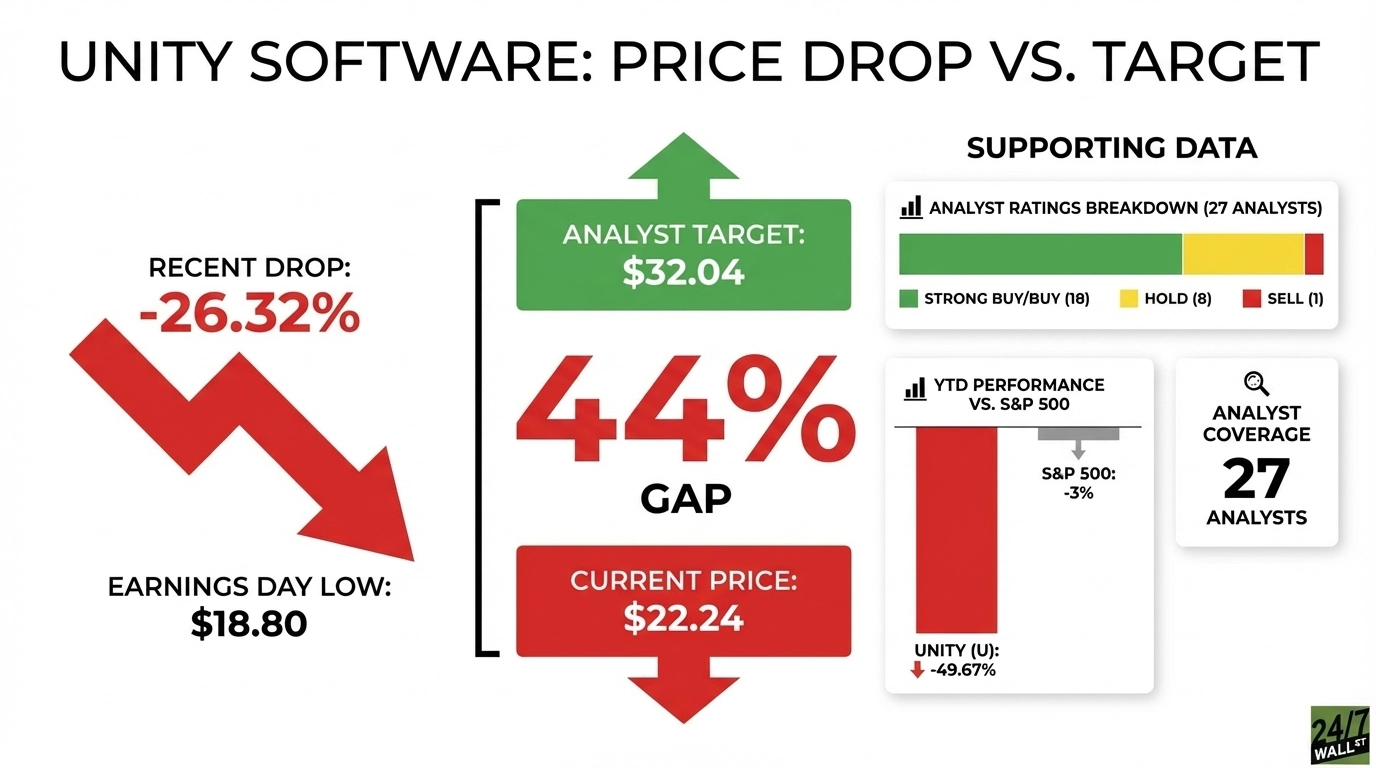

Unity Software (NYSE:U | U Price Prediction) currently trades at $22.24, while Wall Street’s consensus price target sits at $32.04, meaning analysts see roughly 44% upside for the stock today.

A Beat That Sent the Stock Down Nearly 30%

Unity reported Q4 2025 revenue of $503 million, beating the $493 million consensus estimate, and adjusted EPS of $0.24 against a $0.2051 estimate, a 17% beat. The stock dropped around 26.32% on earnings day, with the session low touching $18.80. The culprit was Q1 2026 guidance: revenue of $480 million to $490 million, a sequential step-down that missed market expectations after a strong holiday quarter.

Unity’s preliminary Q1 results released on March 26th point to revenue of $505 million to $508 million and adjusted EBITDA of $130 million to $135 million, both well above prior guidance. The upside is being driven by Unity Vector, which is expected to grow 15% sequentially, along with better-than-expected performance in the Create segment.

The company is also reshaping its ad business. Unity plans to sunset the ironSource Ads Network by the end of April and is exploring a sale of its Supersonic publishing unit. Excluding these businesses, Strategic Grow revenue is expected to increase 48% year over year, roughly double the overall Grow segment’s growth rate, while Strategic Create revenue is expected to grow 14%. Unity’s year-to-date decline stands at roughly 49.67%, while the S&P 500 is down roughly 3% over the same period, which represents nearly 47 percentage points of underperformance.

Why Analysts Are Still Holding Their Targets

The bull case centers on Vector. CEO Matt Bromberg said on the Q4 earnings call that “Vector revenue has grown 53% in the first three quarters since its launch, and we believe we are still very much at the beginning of the trajectory. This January was Vector’s best revenue month ever, larger even than the holiday record set in December, and 72% larger than January. He also projected that “by the end of 2026, we expect the quarterly revenue run rate for Vector to be comfortably more than $1 billion a year.” That is significant for a platform currently representing 56% of Grow Solutions’ revenue.

The next catalyst analysts are watching is the integration of Unity’s runtime engine data into Vector’s ad models, expected in Q2 2026. Bromberg described it as a compounding improvement, noting opt-in rates from developers using the data framework have exceeded 90%. On the Create side, CFO Jarrod Yahes noted that “excluding the impact of non-strategic revenue, our Create business grew an extremely healthy 16% year over year.” Unity 6 adoption is tracking at the fastest rate in company history, and the China business grew nearly 50% in 2025.

A 44% Gap With a Stock That Has Already Cut Its Losses in Half

Of the 27 analysts covering Unity, 18 rate the stock a Buy, 8 rate it a Hold, and 1 rates it a Strong Sell. Wells Fargo trimmed its target from $38 to $29 but maintained an Outperform rating. Wedbush reiterated its Outperform rating with a $30 price target. While analysts have downgraded their target prices, they’re still largely bullish and haven’t abandoned the thesis.

The stock touched a low near $18.36 before recovering, gaining 4.61% over the past month as sentiment stabilizes. Free cash flow for full-year 2025 came in at $403.93 million, up 47.88% year over year, and Unity holds $2.055 billion in cash. The balance sheet is solid.

Might Only Be Worth the Risk If Vector Keeps Compounding

The case for Unity strengthens if Vector’s runtime data integration delivers measurable model improvement in Q2 2026 and the sequential revenue step-down proves seasonal rather than structural. Vector’s 70% year-over-year growth is quite strong. If analysts are right that IronSource’s drag is nearly finished and Vector becomes the dominant revenue engine, the current price looks deeply discounted.

The bear case builds if the earlier guidance cut signals Vector is hitting advertiser budget limits sooner than expected, or if macro pressure and US-China tensions weigh on mobile ad spending. Unity’s beta of 1.998 amplifies market swings. A stock that dropped nearly 50% while the index barely moved highlights real sentiment risk. The market may be pricing in a longer recovery than analysts expect.

The business is improving, the balance sheet is solid, and Vector has real traction. Still, investors should size positions with volatility in mind. The pace of the recovery will depend on both execution and market conditions in the quarters ahead.

Contact [email protected] for any questions or corrections.