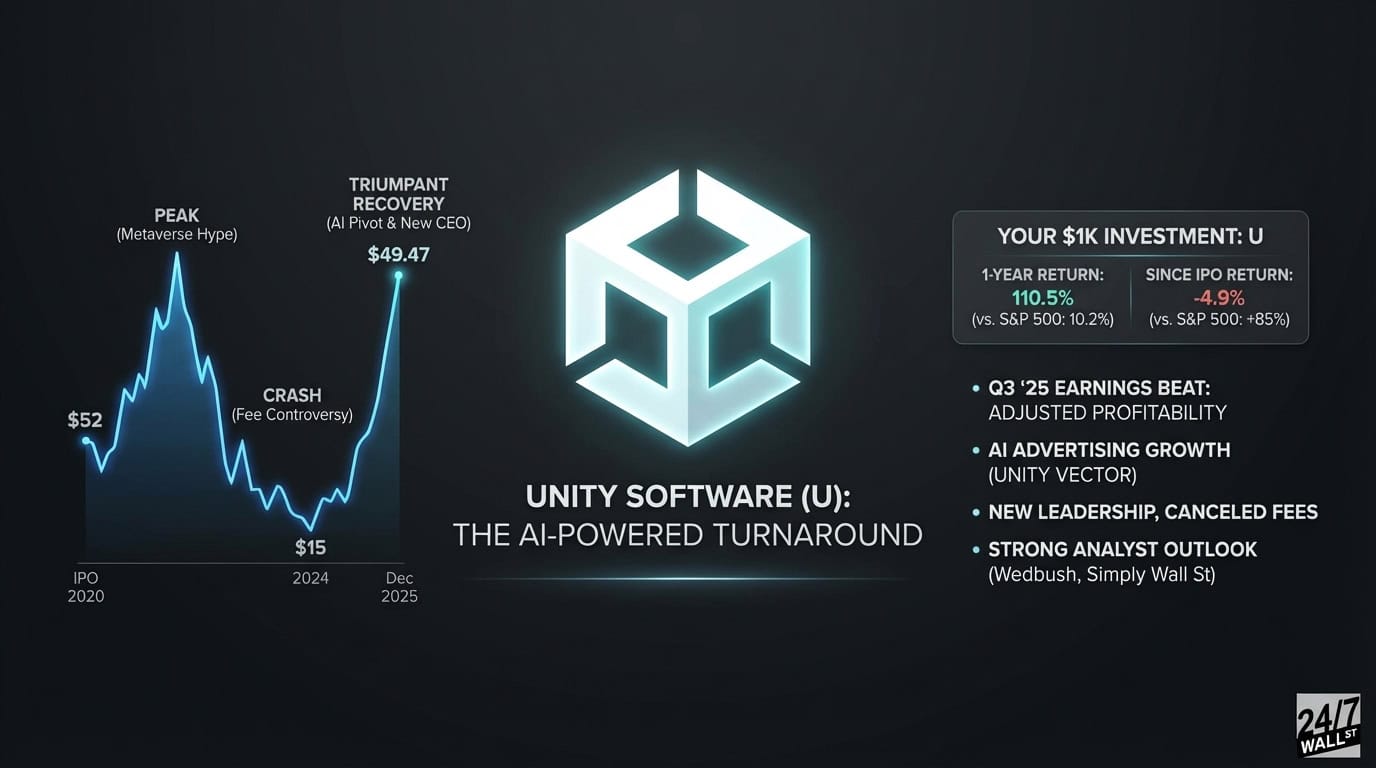

Unity Software (NYSE: U | U Price Prediction) went public in September 2020 at $52 per share during the pandemic gaming boom. The company provides the engine behind thousands of mobile games and interactive 3D experiences. Its business splits into Create Solutions (development tools) and Grow Solutions (advertising and monetization platform).

The stock peaked above $200 in late 2021 during metaverse hype, then crashed over 80% by 2024. Unity burned cash, posted widening losses, and alienated developers with a controversial runtime fee structure threatening to charge per game install. New CEO Matthew Bromberg canceled the unpopular fees in early 2024, raised subscription prices, and pivoted into AI-powered advertising with Unity Vector.

The stock bottomed around $15 in early 2024 and has since tripled.

Your $1,000 Tripled in 18 Months

Here’s what $1,000 invested at different points would be worth today at $49.47 per share:

1-Year Return (December 2024 to December 2025)

- Initial Investment: $1,000

- Current Value: $2,105

- Total Return: 110.5%

- S&P 500 (same period): $1,102 (10.2%)

Since IPO (September 2020 to December 2025)

- Initial Investment: $1,000 at $52 IPO price

- Current Value: $951

- Total Return: -4.9%

- S&P 500 (same period): Approximately $1,850 (85%)

IPO investors remain underwater after five years. But 2024 buyers doubled their money in 12 months, crushing the S&P 500 by 100 percentage points.

Unity’s Q3 2025 earnings on November 5 delivered a massive surprise. The company posted adjusted earnings of $0.20 per share against expectations of a $0.24 loss. Revenue of $471 million beat estimates, and management credited Unity Vector AI for driving 6% growth in the advertising segment. Free cash flow hit $151 million. Analysts expect $0.89 in earnings for fiscal 2025, turning the corner to profitability.

Wedbush added Unity to its Best Ideas List in early December, citing undervaluation in the game engine and mobile ad markets. Simply Wall St estimated fair value at $55.77, suggesting 20% upside at current prices near $49.

Risk and Opportunity Profile

Unity’s profile includes high growth potential through AI-powered advertising, 74% gross margins, and a path to profitability. The company dominates mobile game development, Vector AI is working, and the stock trades at 11.7 times sales with a forward P/E of 105. However, Unity still posted a $127 million GAAP loss in Q3 despite adjusted profits. The stock has a beta above 2, meaning higher volatility than the market. Insider selling has been heavy, with directors unloading millions in shares. Competition from Epic’s Unreal Engine remains fierce, and geopolitical risk exists with significant operations in Israel.

The turnaround appears real, the AI monetization story has legs, and the valuation isn’t insane relative to peers like Roblox (15.6 times sales, still unprofitable). The stock’s high volatility requires careful position sizing.

Contact [email protected] for any questions or corrections.