Our price target for Alphabet (NASDAQ:GOOG | GOOG Price Prediction) is $352.02, representing 11.5% upside from the current price of $315.72. The 24/7 Wall St. model signals buy, with a 90% confidence level. The fundamental story is compelling: accelerating Cloud growth, a dominant AI platform, and reasonable valuation for a company of this quality.

| Metric | Value |

|---|---|

| Current Price | $315.72 |

| 24/7 Wall St. Price Target | $352.02 |

| Upside | +11.5% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Year of Remarkable Recovery

Alphabet has staged one of the most impressive recoveries among mega-cap technology stocks over the past twelve months. Shares are up 103.9% over the past year, rising from $154.84 in April 2025 to $315.72 today. Year-to-date, the stock is up 0.68%, with a 7.22% gain over the past week suggesting renewed buying interest.

The catalyst was strong earnings beats. In Q4 2025, Alphabet reported EPS of $2.82 against a $2.63 estimate, a 7.22% beat, on revenue of $113.83B versus $111.35B expected. Full-year 2025 revenue crossed $400B for the first time, reaching $402.84B, with net income surging 32.01% year-over-year to $132.17B.

The Bull Case

The bull case centers on Google Cloud and AI infrastructure monetization. Cloud revenue grew 48% year-over-year in the quarter to $17.66B, with operating income more than doubling. The Cloud backlog stood at $155B as of Q3 2025, providing strong revenue visibility. CEO Sundar Pichai noted that “Google Cloud ended 2025 at an annual run rate of over $70 billion.”

AI adoption metrics reinforce growth. The Gemini App reached 750 million monthly active users, processing over 10 billion tokens per minute. YouTube’s annual revenue surpassed $60 billion across ads and subscriptions, and paid subscriptions across consumer services topped 325 million.

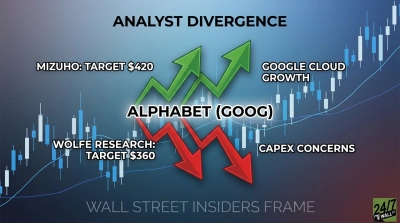

The analyst consensus target of $359.53 implies further upside, and our bull case projects $381.99 by April 2027 if Cloud acceleration continues and AI monetization ramps.

What Could Go Wrong

The most significant risk is CapEx escalation. Alphabet guided for $175B to $185B in capital expenditures in 2026, compared to $91.45B spent in 2025. Free cash flow grew just 0.69% year-over-year to $73.27B, even as operating cash flow rose 31.46%.

If AI infrastructure spending fails to generate commensurate returns, the stock could re-rate lower. Our bear case scenario puts the stock at $286.34 by April 2027.

Antitrust exposure remains a headwind. A $3.5B European Commission competition fine hit in Q3 2025, and regulatory scrutiny over Search dominance remains elevated. Other Bets operating losses widened to $3.6B in Q4, a drag that compounds as CapEx scales.

Bulls argue the massive CapEx commitment reflects management confidence in demand, and the Cloud backlog of $155B provides a clear path to ROI.

The Verdict

The 24/7 Wall St. price target of $352.02 reflects a business genuinely accelerating. Revenue growth went from 12% in Q1 2025 to 18% in Q4 2025, Cloud compounds at nearly 50% annually, and AI platform metrics are extraordinary. At 29x trailing earnings, valuation is reasonable for a company generating $164.71B in annual operating cash flow.

Cloud acceleration and 2026 CapEx translation into margin expansion by mid-year represent the key variables to watch. Antitrust rulings restricting Search monetization or sharp free cash flow deterioration represent the primary downside risks. The risk/reward, based on current data, favors the bull case.

Alphabet Price Projection 2026-2030

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $352.02 |

| 2027 | $381.99 |

| 2028 | $410.00 |

| 2029 | $440.00 |

| 2030 | $463.41 |

These projections assume continued Cloud growth and AI monetization. Significant upside could result from Waymo scaling commercially or breakthrough AI products. Primary downside risk remains regulatory action against Search or prolonged CapEx compression of free cash flow.

Contact [email protected] for any questions or corrections.