The stock market keeps rolling along as if nothing can stop it. The S&P 500 recently hit another all-time high, unemployment remains low at 4.3%, and payroll growth has continued to beat expectations, according to the latest Bureau of Labor Statistics report. President Donald Trump has pointed to both as proof the economy remains on solid footing.

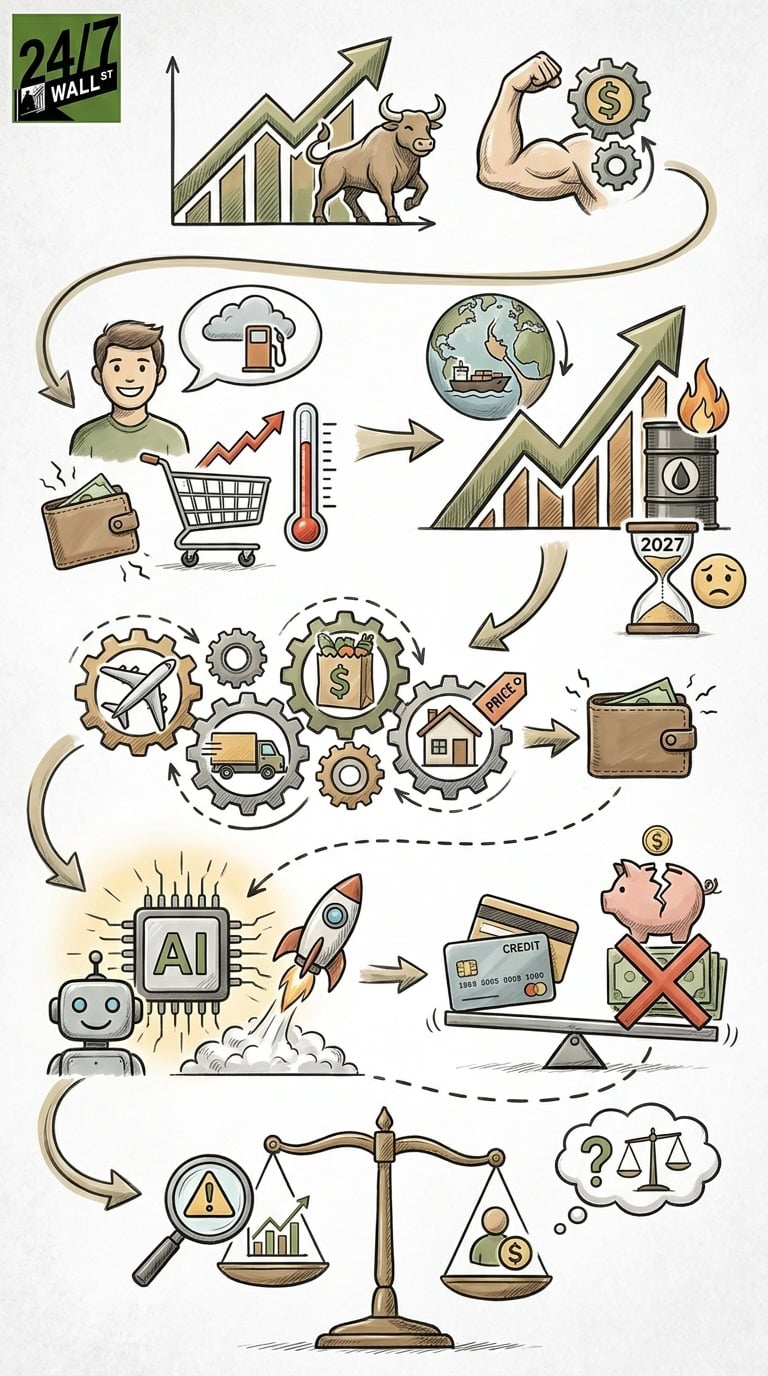

Yet underneath the surface, cracks are widening. The University of Michigan’s consumer sentiment index recently fell to its lowest level in 75 years. Gasoline prices have surged to a national average of $4.52 per gallon, with nine states now ranging between $4.71 and $6.15. Consumers increasingly cite energy costs and tariffs as their top financial concerns.

So the question investors need to ask is simple: what happens if high energy prices are not temporary after all?

Wall Street Still Believes Oil Prices Will Cool Off

Right now, the market appears to be treating the recent spike in oil and gasoline prices as a short-term geopolitical shock. The thinking goes something like this: once tensions surrounding Iran ease and shipping through the Strait of Hormuz normalizes, crude prices should settle back down.

That assumption matters a lot.

The Strait of Hormuz handles roughly 20% of the world’s oil supply, according to the U.S. Energy Information Administration. Any disruption there ripples through global energy markets almost instantly. Oil prices surged after the conflict escalated, yet stocks barely blinked. The Nasdaq continues powering higher on enthusiasm surrounding artificial intelligence, semiconductor demand, and data-center spending.

In other words, investors are betting the energy shock fades before it damages consumer spending or corporate earnings.

Granted, there is some logic behind that optimism. Consumers continued spending through much of the inflation spike in 2022 and 2023 even after gasoline prices climbed above $5 per gallon nationally during the Biden administration. Household balance sheets were stronger then, though, and savings accumulated during the pandemic helped cushion the blow.

Today looks different. Credit card delinquencies have risen, according to the Federal Reserve Bank of New York. Consumer confidence has weakened sharply. Tariffs have pushed up prices on everything from appliances to auto parts. That leaves less room for families to absorb another prolonged jump in fuel and transportation costs.

And then came Saudi Aramco’s warning.

Don’t let the S&P 500 records fool you—underneath the surface, soaring energy costs and 75-year lows in sentiment are creating a dangerous economic divide.

Don’t let the S&P 500 records fool you—underneath the surface, soaring energy costs and 75-year lows in sentiment are creating a dangerous economic divide.

The Market’s Biggest Belief Just Got Challenged

Saudi Aramco CEO Amin Nasser told Bloomberg that even if the Strait of Hormuz fully reopened today, “it will take a few months for the oil market to rebalance.” Even worse, he warned that if disruptions continue for more than several weeks, normalization may not occur until sometime in 2027.

That is a startling statement coming from the head of the world’s largest oil producer. Saudi Aramco produces around 9 million barrels of oil per day and carries a market value larger than Exxon Mobil (NYSE:XOM | XOM Price Prediction). When all is said and done, few executives have a clearer view of global oil supply chains than Nasser.

Look at it this way: If oil stays elevated for another year or more, gasoline prices likely rise further from today’s already painful levels. Diesel prices would climb too, increasing shipping and freight costs across the economy. Airlines would face higher fuel bills. Manufacturers would see transportation expenses expand. Grocery stores would pay more to move food nationwide. Nearly everything consumers buy could get more expensive.

Surprisingly, the risk may not be inflation alone. It is the combination of inflation and slowing growth that could become dangerous for stocks.

AI Euphoria Can Only Carry Markets So Far

Right now, artificial intelligence remains the market’s main engine. Nvidia (NASDAQ:NVDA) alone has added trillions in market value as demand for AI chips continues outpacing supply. Mega-cap technology stocks have masked weakness elsewhere in the market, much like during prior late-stage bull runs.

But consumers still drive roughly 68% of U.S. GDP, according to the Bureau of Economic Analysis. If families begin pulling back spending because gasoline, food, utilities, and tariffs consume more of their paychecks, corporate earnings growth could slow quickly.

Retailers would feel it first. Restaurants and travel companies would likely follow. Automakers, already dealing with tariff-related cost increases, could face softer demand. Eventually, even technology companies may struggle if businesses reduce spending plans.

That does not mean a recession is guaranteed. The labor market still looks resilient, and corporate balance sheets remain healthier than during past downturns. That said, markets priced for perfection rarely respond calmly when profit growth weakens.

Key Takeaway

In short, Saudi Aramco’s warning matters because it challenges the market’s belief that the oil shock will fade quickly. If Nasser is right and energy markets remain strained into 2027, consumers could face gasoline prices exceeding the inflation peaks seen during the Biden years.

Regardless of how you look at it, sustained energy inflation would pressure household budgets at the exact moment consumer sentiment already sits near record lows. The Trump bull market has so far powered higher on AI excitement and strong jobs data. But bull markets eventually need broad economic strength — not just a handful of technology giants carrying the indexes higher.

Smart investors should keep watching oil prices, consumer spending trends, and corporate earnings guidance closely. Because if energy costs stay elevated longer than Wall Street expects, the next big market correction may not come from AI hype fading — it could come from consumers finally running out of room to spend.

Contact [email protected] for any questions or corrections.