For much of 2026, the chip trade has been the only show on Wall Street. The iShares Semiconductor ETF (SOXX) is still up 77% year to date through May 11, Advanced Micro Devices (NASDAQ:AMD | AMD Price Prediction) has more than doubled, and Intel (NASDAQ:INTC) has been the comeback story of the cycle. But today, the bid disappeared. SOXX fell 3.2% intraday, AMD dropped 2.3%, and Intel got hit hardest at down 6.8%. NVIDIA (NASDAQ:NVDA) was the lone holdout, closing up 0.6% to $220.78.

This kind of broad semiconductor flush is exactly the moment Wall Street starts pulling up old charts. I’ve been watching the chip cycle since the 2018 trade-war bottom, and the muscle memory of the last two real selloffs is doing most of the talking in trader chats right now. So let’s actually read the long memory instead of guessing.

The Q4 2018 Drawdown: A Trade-War Air Pocket

The first comparison everyone reaches for is the late-2018 chip wreck. The PHLX Semiconductor Index fell roughly 25% from October to December that year as the Fed tightened, the China trade war escalated, and smartphone demand cratered. NVIDIA caught the worst of it: the stock fell 54% in the fourth quarter of 2018 alone, from $7.17 to $3.31 on a split-adjusted basis. The catalyst was a crypto mining inventory glut layered on top of macro fear, and the bottom came in late December.

Intel, interestingly, barely participated. INTC actually finished Q4 2018 up 1.7% because the data center build-out was still intact and Intel was the default CPU. That dispersion matters: not every chip stock trades the same selloff the same way. When the secular driver under one name stays solid, that name decouples.

What followed the 2018 bottom is the part bulls remember. The SOX more than doubled over the next 18 months as 5G capex ramped and Nvidia’s data center business started showing up in earnings.

The 2022 Bear: An Inventory Reset Met a Capex Pause

The 2022 selloff was uglier and longer. SOX dropped roughly 36% peak to trough. The catalysts: a crypto/gaming inventory glut, a hyperscaler capex pause, and rate shock. Every major chip name took damage.

- NVDA fell 51% in calendar 2022, from $30.06 to $14.60.

- AMD fell 57%, from $150.24 to $64.77.

- Intel fell 48%, from $49.33 to $25.47.

NVDA bottomed in October 2022, then began the historic AI-driven run that delivered a roughly 1,499% five-year return through this past Monday. The lesson from 2022 is similar to 2018: sharp chip selloffs driven by demand-cycle fears have historically marked entry points when the underlying secular driver, in that case AI, remained intact.

Does Today’s Setup Actually Match Either Precedent?

Here’s where I have to be honest. Today’s setup does not cleanly resemble 2018 or 2022. Both prior selloffs were demand resets, with real inventory bloat, real capex pauses, and earnings revisions ahead. The current chip backdrop looks nothing like that.

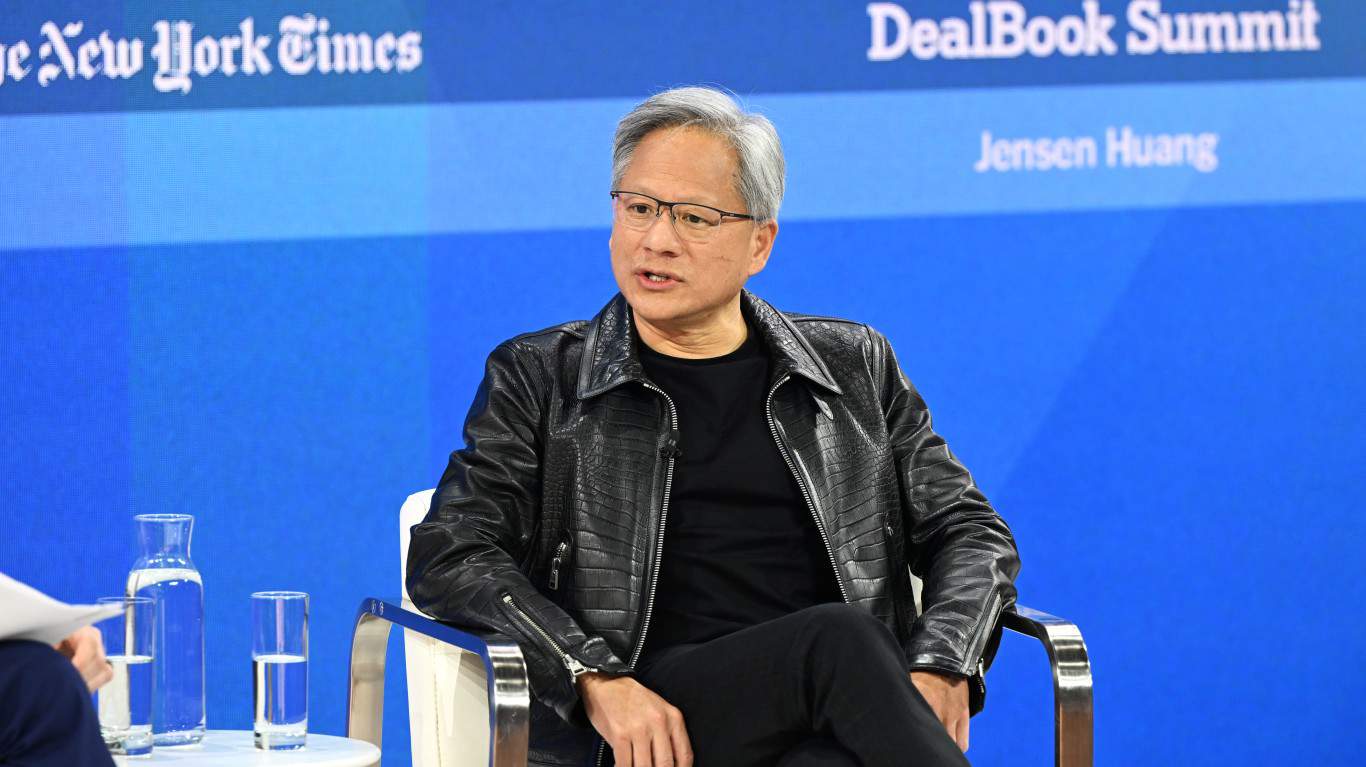

NVIDIA just reported Q4 FY2026 revenue of $68.13 billion, up 73.2% year over year, with data center revenue of $62.31 billion (+75%) and a Q1 FY2027 guide of roughly $78.0 billion. CEO Jensen Huang said “computing demand is growing exponentially, the agentic AI inflection point has arrived.” AMD just delivered $10.25 billion in Q1 FY2026 revenue, up 38%, with data center up 57% and a Q2 guide near $11.2 billion. Lisa Su called out “leading customer forecasts exceeding our initial expectations” on the MI450 series, anchored by a 6-gigawatt deal with Meta. Intel’s Q1 came in at $13.58 billion in revenue and $0.29 non-GAAP EPS, with data center and AI revenue up 22%.

So the fundamentals say we are mid-cycle. The valuation says caution. AMD trades at 173x trailing earnings and 112x free cash flow, rich against any reasonable historical median. Intel’s 251% year-to-date rally and 504% one-year return have priced in a lot of foundry optionality before $2.51 billion in Q4 2025 foundry operating losses have actually narrowed.

What the Long Memory Actually Says

Read 2018 and 2022 together and a pattern emerges. Selloffs that started with valuation fatigue inside an intact demand cycle resolved upward within 6 to 12 months. Selloffs that started with an actual demand break, real inventory glut, real capex pause, took longer and went deeper. The catalyst, not the magnitude, determines the recovery path.

Today’s move looks like the first kind. A 3% SOXX day after a year-to-date ramp that absurd is rotation. I’m watching the next two NVIDIA and AMD earnings reports for any crack in the data center growth rate. As long as those numbers hold, the long memory says this is noise. The day the hyperscaler capex commentary turns, that is when 2022 starts to rhyme.

For now, the chip sector is bleeding. History suggests that is usually when it pays to keep reading the fundamentals, not the headlines.

Contact [email protected] for any questions or corrections.