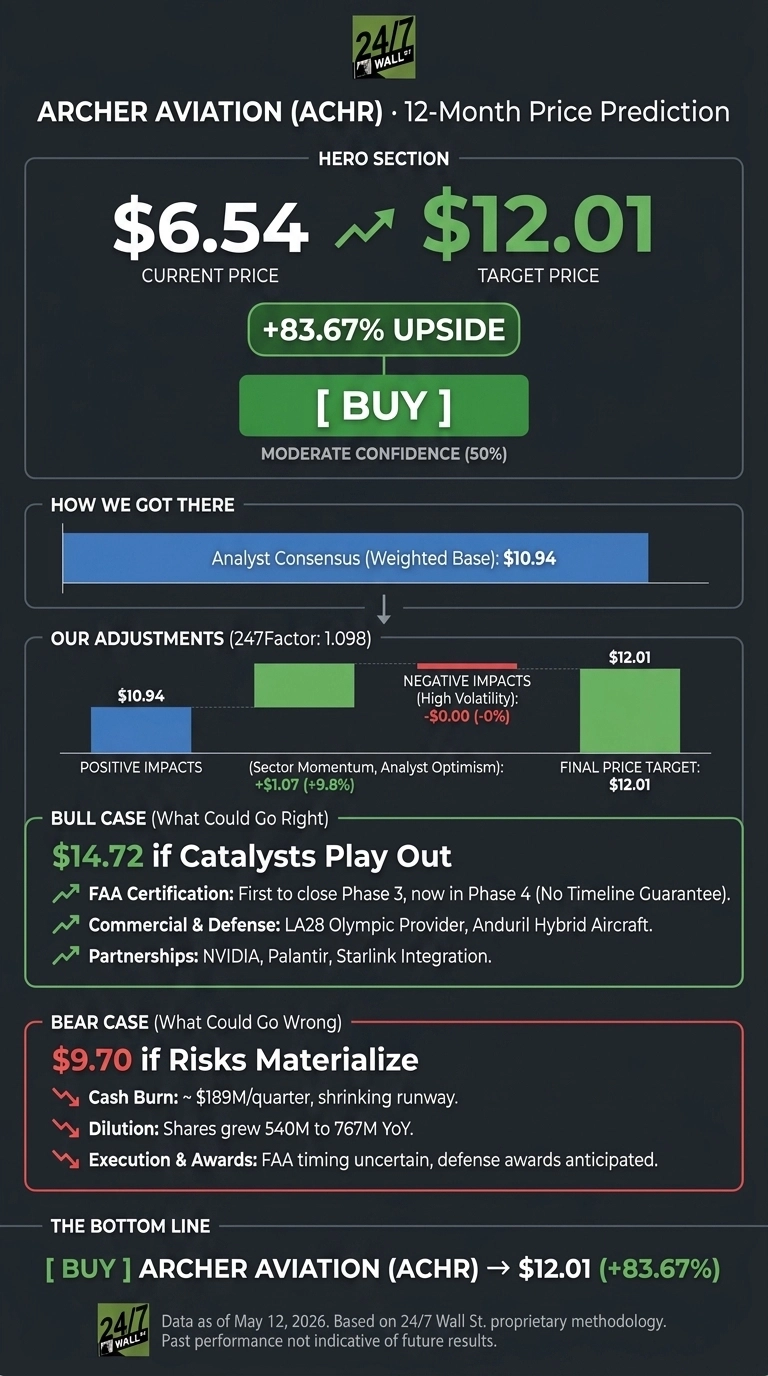

Archer Aviation (NYSE:ACHR | ACHR Price Prediction) delivered Q1 2026 results with operational momentum offset by a beaten-down share price. Our 24/7 Wall St. price target for Archer is $12.01, implying meaningful upside from current levels with moderate confidence.

The 24/7 Wall St. Price Target: $12.01

| Metric | Value |

|---|---|

| Current Price | $6.54 |

| 24/7 Wall St. Price Target | $12.01 |

| Upside | 83.67% |

| Recommendation | BUY |

| Confidence | 50% (moderate) |

This is a buy rating with calibrated expectations. Archer is pre-revenue at scale, and the path to commercialization runs through the FAA. Our target reflects analyst consensus adjusted by proprietary factors.

Quarterly Numbers Tell a Story of Spend and Progress

Archer reported Q1 2026 results on May 11, 2026. EPS came in at -$0.28, revenue was $1.60 million from Hawthorne Airport operations, and net loss widened to $217.70 million. R&D spend surged to $171.70 million as Archer advanced FAA Type Certification and the Anduril hybrid aircraft program. Adjusted EBITDA loss of $172.50 million landed within guided range.

Cash and equivalents stand at $951.10 million, with total liquidity near $1.80 billion. Shares climbed 540 million to 767 million year over year. The stock is down 25.77% over the past year and 13.03% year to date, but rallied 21.11% in the past month heading into the earnings report.

Why Bulls See a Breakout Ahead

The bull case rests on CEO Adam Goldstein’s thesis: “Archer is now a multi-threat company and we expect to begin initial operations of our air taxis in US cities, winning phased government awards, and deploying our AI solutions later this year.” Archer is the first eVTOL company to close Phase 3 of FAA Type Certification and is now in Phase 4.

They are the Official Air Taxi Provider for the LA28 Olympic Games, were selected in three winning eIPP applications spanning eight states, and partner with Anduril on a dual-use hybrid aircraft Goldstein calls “the most sophisticated vertical lift platform ever developed.”

Add partnerships with NVIDIA, Palantir, and Starlink, plus international launch programs across the UAE, Korea, and Japan. Our bull-case scenario projects $14.72 over the next 12 months.

The Risks Worth Watching

Archer burns roughly $189 million per quarter. At current cash levels, runway is finite, and Q2 guidance calls for adjusted EBITDA loss of $170 million to $200 million. Phase 4 compliance testing has no guaranteed timeline, and defense awards remain anticipated rather than booked. Insider activity skews mixed, with concentrated March selling at $5.30 to $6.46 per share.

Bulls argue widening losses reflect deliberate investment in FAA certification and the Anduril platform rather than deteriorating fundamentals. The $1.80 billion raised in 2025 was the price of optionality. Our bear-case 12-month scenario lands at $9.70.

I’d Buy It Here, With Eyes Open

Our price target is $12.01 with a buy recommendation and moderate confidence. The factor tipping the scale is FAA certification trajectory paired with a fortress balance sheet for a pre-revenue name. I’d be a buyer if Phase 4 milestones land on schedule and initial US operations begin in 2026 as guided. I’d stay on the sidelines if certification slips into 2027 or dilution accelerates beyond current pace.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $12.01 |

| 2027 | $16.34 |

| 2028 | $21.45 |

| 2029 | $28.06 |

| 2030 | $34.24 |

These projections assume Archer executes on FAA certification, scales commercial air taxi operations, and converts at least a portion of its defense and AI pipeline into recurring revenue. Significant upside or downside would follow from certification timing and government contract award trajectory.

Contact [email protected] for any questions or corrections.