Joby Aviation (NYSE:JOBY | JOBY Price Prediction) is one of the most polarizing names in the eVTOL space, and the question on every shareholder’s mind right now is whether the stock can double from here.

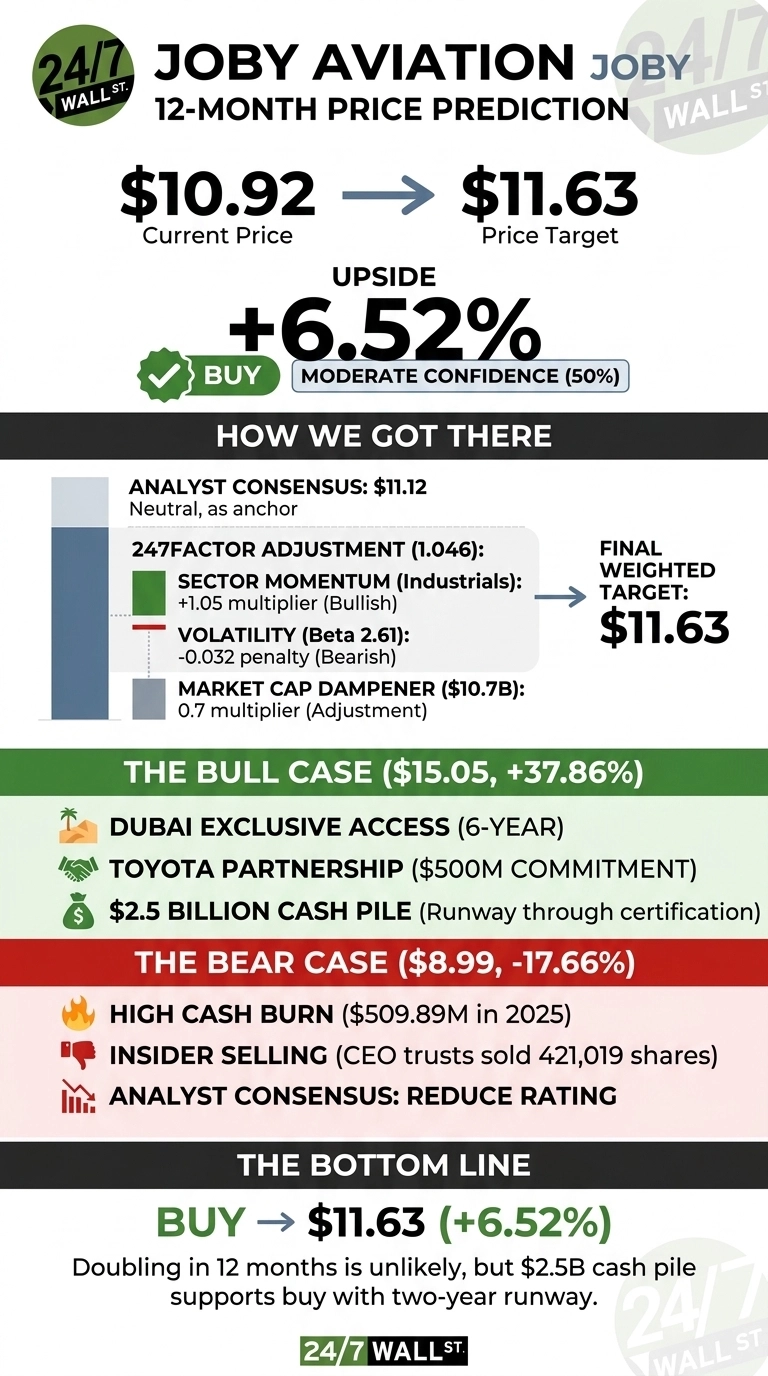

Based on our proprietary model, the answer is no, at least not over the next 12 months. The 24/7 Wall St. price target for Joby is $11.63, implying roughly 6.52% upside from $10.92. Our recommendation is buy with moderate confidence.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $10.92 |

| 24/7 Wall St. Price Target | $11.63 |

| Upside | 6.52% |

| Recommendation | BUY |

| Confidence Level | 50% |

From a Painful Drawdown to a May Rally

Joby has had a volatile year. The stock traded as high as $20.95 in the last 52 weeks before sliding to a low of $6.72. Year to date, shares are down 17.27%, but the past month has brought a sharp rebound of 19.47%, helped by Q1 2026 results that delivered $24.25 million in revenue against an estimate near $19 million to $20.2 million.

The May 2026 capital raise brought in roughly $1.3 billion through a combined equity and convertible notes offering, lifting cash and short-term investments to $2.5 billion. The first eVTOL flights between JFK and Manhattan, completed in under 10 minutes, also reignited the story.

The Case for $15 and Beyond

The bull case is straightforward: 2026 is the inflection year. CEO JoeBen Bevirt has said the focus is shifting “from how and when we’ll go to market, to how many aircraft we can produce and where to deploy them.” Joby holds a 6-year exclusive on Dubai air taxi access, with vertiports planned at DXB Airport, the American University of Dubai, Palm Jumeirah, and Dubai Mall.

Add Toyota’s $500 million commitment, a Kazakhstan LOI valued up to $250 million, and an Abdul Latif Jameel framework worth roughly $1 billion, and the revenue pipeline becomes credible. Our bull case scenario points to $15.05 in a year, a 37.86% gain.

What Could Go Wrong

The bear case is equally specific. Joby burned $509.89 million in operating cash in 2025, and 2026 H1 cash usage is guided to $340 million to $370 million. CEO trusts sold 421,019 shares at a weighted average of $10.38 in mid-May, and the average rating from nine brokerages now reads “Reduce.”

It should be noted, however, that those insider transactions sit under pre-approved 10b5-1 plans rather than discretionary selling, and bulls would argue the cash burn reflects deliberate investment in the Dayton, Ohio facility capable of building up to 500 aircraft per year. Our bear case price target sits at $8.99, a 17.66% drawdown.

Joby Aviation Price Prediction 2026-2030

My final 24/7 Wall St. price target is $11.63 with a buy rating and 50% confidence. The tipping factor is the $2.5 billion cash pile, which buys Joby roughly two years of runway through certification. I would be a buyer here on any pullback to the $9 area if FAA type certification progress continues quarterly.

I would stay on the sidelines if H2 2026 cash burn exceeds guidance or Dubai service entry slips into 2027. Doubling in 12 months is unlikely, but the multi-year setup is real.

Looking further ahead, here is where our model projects Joby could trade in the coming years, assuming current growth trajectories and certification timelines hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $11.63 |

| 2027 | $12.30 |

| 2028 | $13.00 |

| 2029 | $13.70 |

| 2030 | $14.40 |

These projections assume Joby executes on its Dubai launch and ramps Dayton production to four aircraft per month by 2027. Meaningful upside or downside could result from FAA certification timing and the pace of international deployments.

Contact [email protected] for any questions or corrections.