Figma (NYSE:FIG) has had a brutal first nine months as a public company. After pricing its IPO at $33/share on July 31, 2025 and trading as high as $142.92, the design-software leader has collapsed back near its 52-week low. I see that drawdown as a buying opportunity.

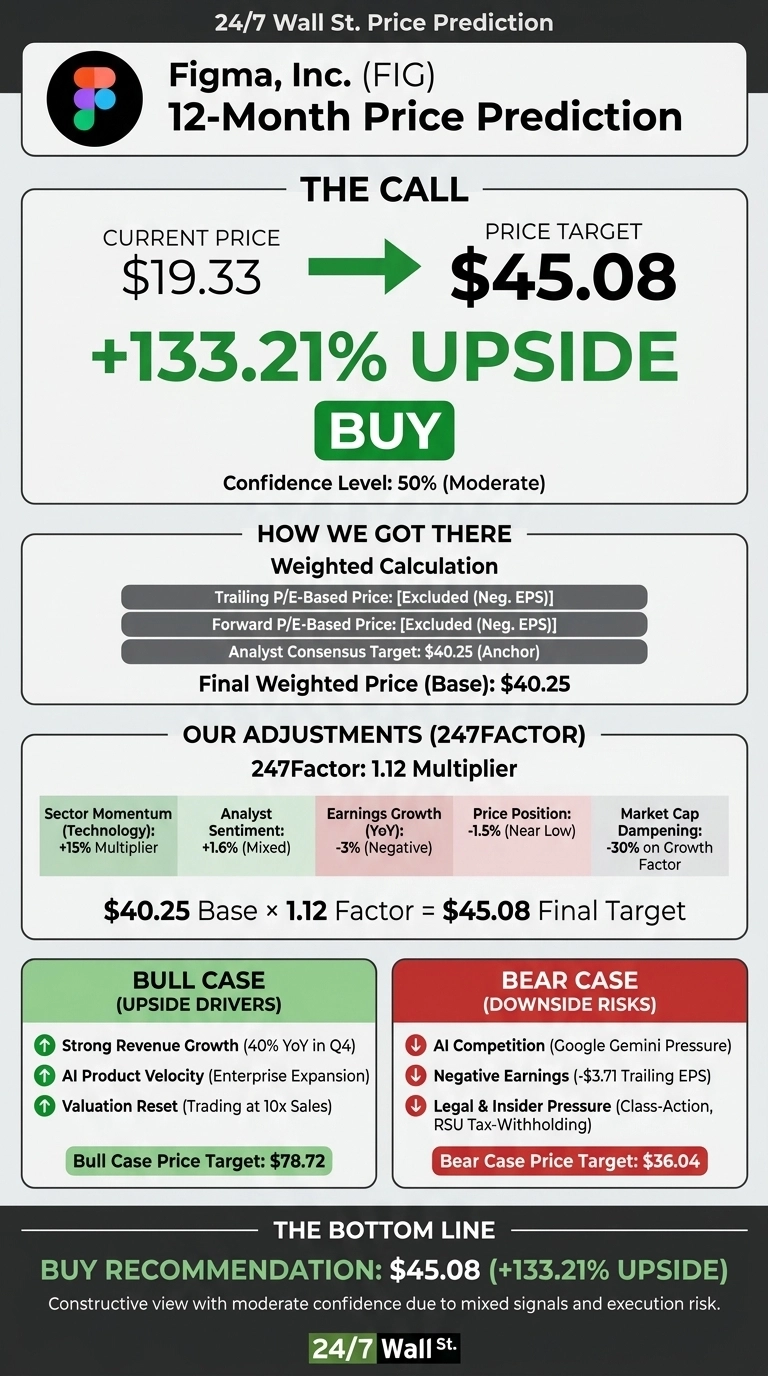

Our 24/7 Wall St. price target for Figma is $45.08, implying 133.21% upside from $19.33. The recommendation is buy, with confidence at a moderate 50%, reflecting genuinely mixed signals between collapsing sentiment and improving fundamentals.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $19.33 |

| 24/7 Wall St. Price Target | $45.08 |

| Upside | 133.21% |

| Recommendation | BUY |

| Confidence Level | 50% |

A Brutal Reset Since the IPO

Figma is down 48.27% year to date and 83.26% over the past year, trading near its $16.60 52-week low.

Two narratives drove the unwind: Google’s free Gemini image-generation tools raised pricing-power fears in February, and a class-action investigation by Lowey Dannenberg followed in March. Yet Q4 revenue grew 40% year over year, full-year 2025 revenue cleared $1.056 billion, and gross margins held at 84.76%. Director Reed Phillips bought $36.5 million of stock in late February, a meaningful contrarian signal.

Why Bulls See a Breakout Ahead

The bull case rests on three pillars. First, growth durability: 40% revenue growth at 84.76% gross margins is a rare combination, and analyst commentary points to profitability in fiscal 2026.

Second, AI as an offensive lever: Figma’s product velocity on enterprise AI features is expanding seat counts internationally.

Third, valuation reset: at 10x sales, FIG trades well below its IPO multiple. Goldman Sachs lifted its target to $54, and Piper Sandler holds an Overweight. Our bull-case scenario points to $78.72 over the next 12 months.

The Risks Worth Watching

The bears are not wrong about the immediate setup. Forward P/E sits at 86, EBITDA is negative $1.27 billion, and RBC Capital trimmed its target to $38 citing AI margin pressure. Insider tax-withholding sales continue almost weekly.

It should be noted, however, that the bulk of recent insider selling is routine RSU tax-withholding, not discretionary, and the GAAP net loss was driven largely by IPO-related stock-based compensation, a non-cash item. Still, if Google’s free tools compress pricing or the class-action overhang widens, our bear-case scenario lands at $36.04.

Our Take on Figma at Current Levels

The 24/7 Wall St. price target of $45.08 with 133.21% upside supports a constructive view, with 50% confidence reflecting real execution risk. The tipping factor is the gap between fundamentals (40% growth, 85% gross margins, a credible AI roadmap) and a stock priced for stagnation. The constructive case strengthens if FIG holds the $16.60 floor and Q1 reaffirms 2026 profitability guidance. The thesis weakens if Google’s Gemini meaningfully erodes seat counts or revenue growth slips below 25%.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $45 |

| 2027 | $70 |

| 2028 | $110 |

| 2029 | $150 |

| 2030 | $190 |

These projections assume Figma sustains 25%+ revenue growth, expands AI monetization, and reaches GAAP profitability on schedule. Significant upside could come from enterprise displacement of Adobe; meaningful downside could come from sustained pricing compression tied to free generative-AI design tools.

Contact [email protected] for any questions or corrections.