BTIG analyst Gray Powell raised the firm’s price target on CrowdStrike (NASDAQ:CRWD | CRWD Price Prediction) to $621 from $499, maintaining a Buy rating ahead of the company’s Q1 FY27 results. The price target raise lands as channel checks signal that CrowdStrike’s platform consolidation pitch is winning more enterprise security wallets.

For prudent investors, this analyst upgrade reinforces a structural thesis already reflected in CrowdStrike stock, which trades near $577. The pre-earnings timing of BTIG’s call suggests rising conviction in the platform consolidation narrative.

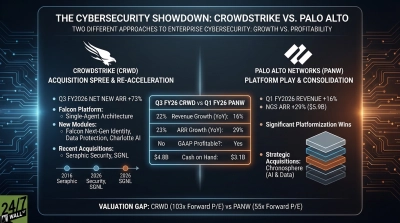

The move arrives the same day Jefferies hiked its target on platform rival Palo Alto Networks (NASDAQ:PANW), underscoring that Wall Street sees cybersecurity consolidation as a multi-winner trade. Both firms are racing to capture enterprise security spend through unified platforms.

| Ticker | Company | Firm | Action | Old Rating | New Rating | Old Target | New Target |

|---|---|---|---|---|---|---|---|

| CRWD | CrowdStrike | BTIG | Price target raised | Buy | Buy | $499 | $621 |

The Analyst’s Case

Powell’s $122 CrowdStrike target hike rests on proprietary checks with industry contacts indicating that the company’s platform consolidation story is increasingly resonating with buyers. Feedback on Identity, Cloud Security, vulnerability management, and newer AI Security products was encouraging.

That product breadth matters. Each new module on the Falcon platform creates attach revenue beyond core endpoint, and CrowdStrike reported 50% of customers on 6+ modules, 34% on 7+, 24% on 8+ at the end of Q4 FY26.

Company Snapshot

CrowdStrike carries a market cap of roughly $145.8 billion and closed FY26 with $4,812 million in revenue, up 22% year over year (YoY). Ending ARR hit $5.25 billion, with Falcon Flex ARR of $1.69 billion, up 120%+ YoY.

CEO George Kurtz framed the strategy bluntly in Q3 FY26, stating that the “single platform strategy coupled with the Falcon Flex subscription model unlocks consolidation, positioning CrowdStrike as the operating system of cybersecurity.” That positioning underpins BTIG’s bullish channel-check thesis.

Why the Move Matters Now

The valuation is rich. CrowdStrike trades at a forward P/E ratio of 109x and a price-to-sales ratio of 30x, well above Palo Alto Networks’ forward P/E ratio of 52x. BTIG’s new target sits comfortably above the consensus analyst target of $493.19.

BTIG’s pre-earnings timing signals conviction. CrowdStrike has guided for Q1 FY27 revenue of $1,360 to $1,364 million and full-year revenue of $5,867.6 to $5,927.6 million.

What It Means for Your Portfolio

The CrowdStrike bull case rests on continued platform consolidation, AI-security attach, and Falcon Flex compounding. The Falcon Flex book has scaled fast, and management is targeting a long-term goal of $10 billion in ending ARR.

The bear case is equally clear. CrowdStrike booked a GAAP operating loss of $293.3 million for FY26, still carries $117.7 million in incident-related costs tied to the July 19, 2024 Falcon sensor event, and faces an aggressive Palo Alto Networks pursuing the same platformization playbook.

For prudent investors, CrowdStrike stock warrants careful position sizing. Investors may want to research how the upcoming Q1 report validates or pressures BTIG’s channel-check thesis before adding exposure at current multiples.

Contact [email protected] for any questions or corrections.