Jefferies analyst Joseph Gallo raised his price target on Palo Alto Networks (NASDAQ:PANW | PANW Price Prediction) to $265 from $215, reiterating a Buy rating following CyberArk’s IMPACT26 Conference. The central thesis: frontier AI is compressing attack timelines, forcing enterprises to accelerate spending on automated, identity-based detection and response.

The price target raise lands as Palo Alto Networks shares trade near $237, with the stock up roughly 47% over the past month. For prudent investors, the call reinforces a platform consolidation story that’s been building all year.

| Ticker | Company | Firm | Action | Old Rating | New Rating | Old Target | New Target |

|---|---|---|---|---|---|---|---|

| PANW | Palo Alto Networks | Jefferies | Price Target Raise | Buy | Buy | $215 | $265 |

The Analyst’s Case

Gallo’s takeaway from CyberArk’s conference is direct: AI tooling lets attackers identify vulnerabilities and execute campaigns faster, and that dynamic is “likely a spend accelerant” for cybersecurity budgets. Defenders increasingly need automated response capabilities that operate at machine speed.

A second pillar is identity. Agent growth and over-permissioning are driving a shift toward modern privileged access management (PAM), although Jefferies cautions, “[W]e think this will take time.” That nuance matters: enterprise security architecture transitions play out across multiple quarters.

Company Snapshot

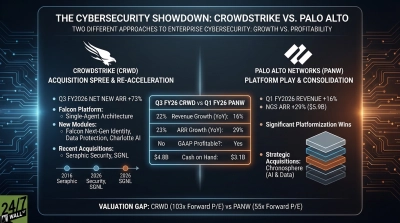

Palo Alto Networks carries a market capitalization of $191.31 billion and runs a cybersecurity platform spanning network, cloud, and security operations, with brands including Unit 42, Cortex, and Cortex XSIAM. In its most recent quarter, the company reported Q2 FY2026 revenue of $2.59 billion, up 15% year over year, with Next-Generation Security ARR of $6.3 billion, up 33%.

Pending acquisitions of CyberArk (identity security) and Chronosphere ($3.35 billion, observability) deepen the platform footprint. Palo Alto Networks’ Q3 FY2026 guidance calls for revenue of $2.941 billion to $2.945 billion, or 28% to 29% growth, reflecting the CyberArk contribution.

Why the Move Matters Now

PANW stock trades at a trailing P/E ratio of 163x and a forward P/E ratio of 52x, a premium even within cybersecurity. The bullish read is that AI-driven attacks pull demand forward, and platformization concentrates spending with vendors like Palo Alto Networks that can deliver integrated detection, response, and identity controls. Next-Generation Security Annual Recurring Revenue (ARR) of $6.30 billion last quarter underscores the platform’s momentum.

The competitive backdrop is intense. CrowdStrike (NASDAQ:CRWD) also received a price target hike today to $621, and CRWD shares are up by about 45% over the past month on the same consolidation theme. CrowdStrike closed FY26 with ending ARR of $5.25 billion, up 24%.

What It Means for Your Portfolio

For long-term investors, the Jefferies analyst upgrade in target reinforces a credible thesis: AI is reshaping both offense and defense in cybersecurity, and platform vendors stand to capture an outsized share of incremental budget. Palo Alto Networks stock has run hard into this print, which raises the bar on execution.

The bear case is straightforward. Palo Alto Networks’ valuation leaves limited margin for error, peers like CrowdStrike are competing for the same consolidation dollars, and the PAM transition Gallo highlights could take longer than bulls expect. A measured PANW stock position size may be prudent for investors building exposure to the AI security cycle.

Contact [email protected] for any questions or corrections.