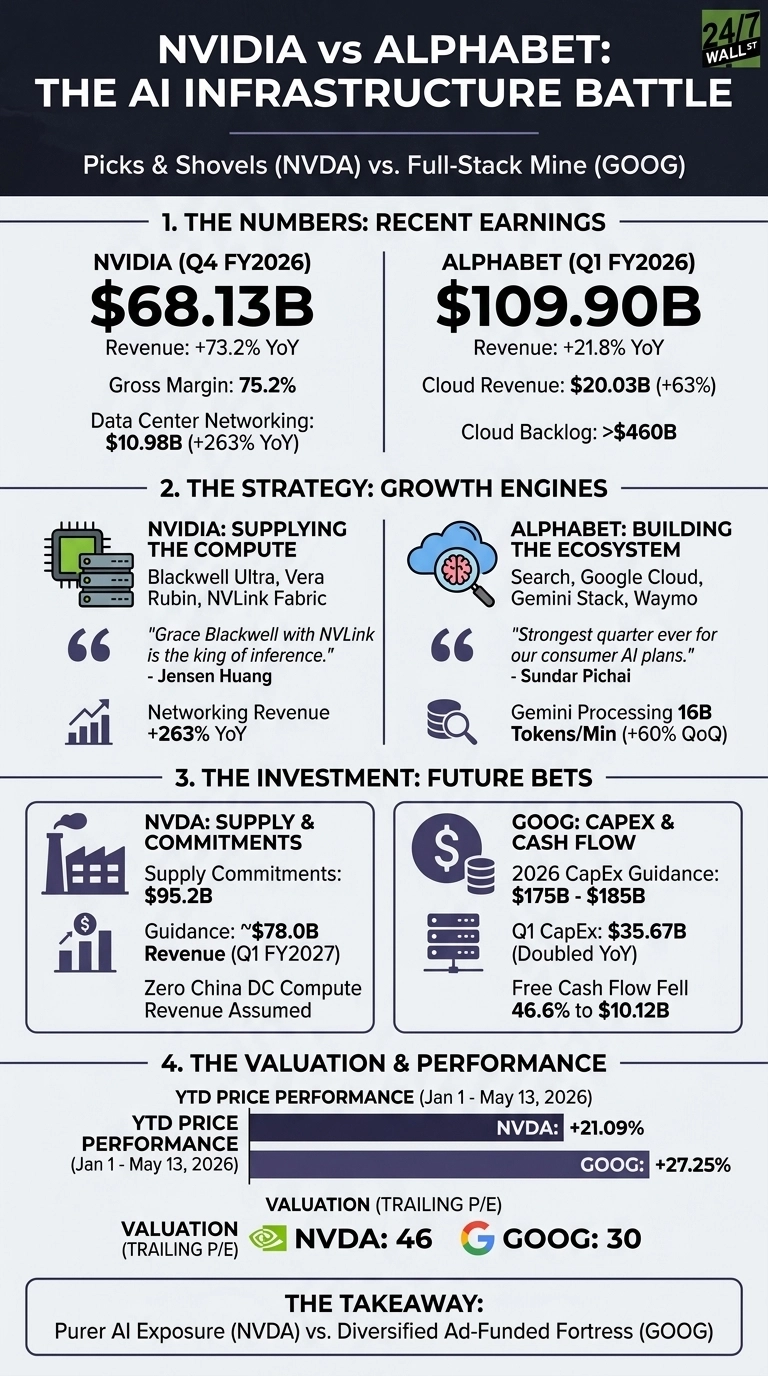

NVIDIA (NASDAQ: NVDA | NVDA Price Prediction) closed its fiscal year on Feb. 25, 2026 with $68.13 billion in Q4 revenue, up 73.2% YoY. Alphabet (NASDAQ: GOOG) followed in late April with $109.90 billion in Q1 revenue and a $460 billion Cloud backlog. Both earnings reports frame the same AI build-out from opposite ends: NVIDIA sells the shovels, Alphabet is digging the mine.

Blackwell Sells Out. Gemini Scales Up.

NVIDIA’s Data Center segment hit $62.31 billion, but the wilder number is networking at $10.98 billion, up 263% YoY, reflecting NVLink fabric demand for GB200 and GB300 racks. Jensen Huang told investors “Grace Blackwell with NVLink is the king of inference today”, and the partner roster (Meta, Anthropic, CoreWeave, AWS, Oracle) supports that claim.

Alphabet’s growth engine is more distributed. Google Cloud grew 63% to $20.03 billion, Search lifted 19% to $60.4 billion, and Gemini now processes 16 billion tokens per minute via direct API, up 60% QoQ. Sundar Pichai called it “our strongest quarter ever for our consumer AI plans”.

| Business Driver | NVIDIA | Alphabet |

| Main Growth Engine | Data Center GPUs and NVLink | Search, Cloud, Gemini stack |

| Q4/Q1 Revenue Growth | 73.2% | 21.8% |

| Gross Margin | 75.2% | 59.7% |

One Sells the Picks. The Other Builds the Mine.

NVIDIA is doubling down on a single product cadence: Blackwell Ultra now, Vera Rubin next, with Huang promising “an order-of-magnitude lower cost per token”. Supply commitments sit at $95.2 billion, and Q1 FY2027 guidance of $78.0 billion explicitly assumes zero China Data Center compute revenue. That is a confident bet, with a real geopolitical asterisk.

Alphabet is funding the other side of the equation. Management already guided 2026 CapEx to $175 to $185 billion, and Q1 spend alone hit $35.67 billion, more than double YoY. The cost: free cash flow fell 46.63% to $10.12 billion. Waymo’s 500,000+ fully autonomous rides per week hints at where some of that cash is going.

The Next Test Is Whether Demand Keeps Compounding

I will be watching whether Alphabet’s $460 billion Cloud backlog actually converts into margin expansion as TPUs and Gemini take share. For NVIDIA, the binding constraint is supply: TSMC capacity, networking ramps, and whether enterprise agent adoption stays on the trajectory Huang described as “skyrocketing”. NVDA’s 21.09% YTD gain trails Alphabet’s 27.25%, hinting investors already priced some of NVDA’s beat.

Why I Lean Toward Alphabet Right Now

If I had to put new money to work today, Alphabet looks more interesting to me. A 30 trailing P/E and a forward multiple near 28 for a business compounding Search, Cloud, and Gemini at 20%+ feels like the easier story to underwrite.

NVIDIA still has the cleaner growth profile, and a 46 P/E with 75% gross margins can absolutely be justified. My hesitation is concentration risk: one product cycle, one foundry, and a China policy ceiling I cannot model.

For a growth-first investor, NVDA is the purer AI exposure. For someone who wants AI growth wrapped inside an ad-funded fortress, GOOG fits better. I would only change my view on NVIDIA if China rules loosen or networking growth slows materially, neither of which the current quarter signals.

Contact [email protected] for any questions or corrections.