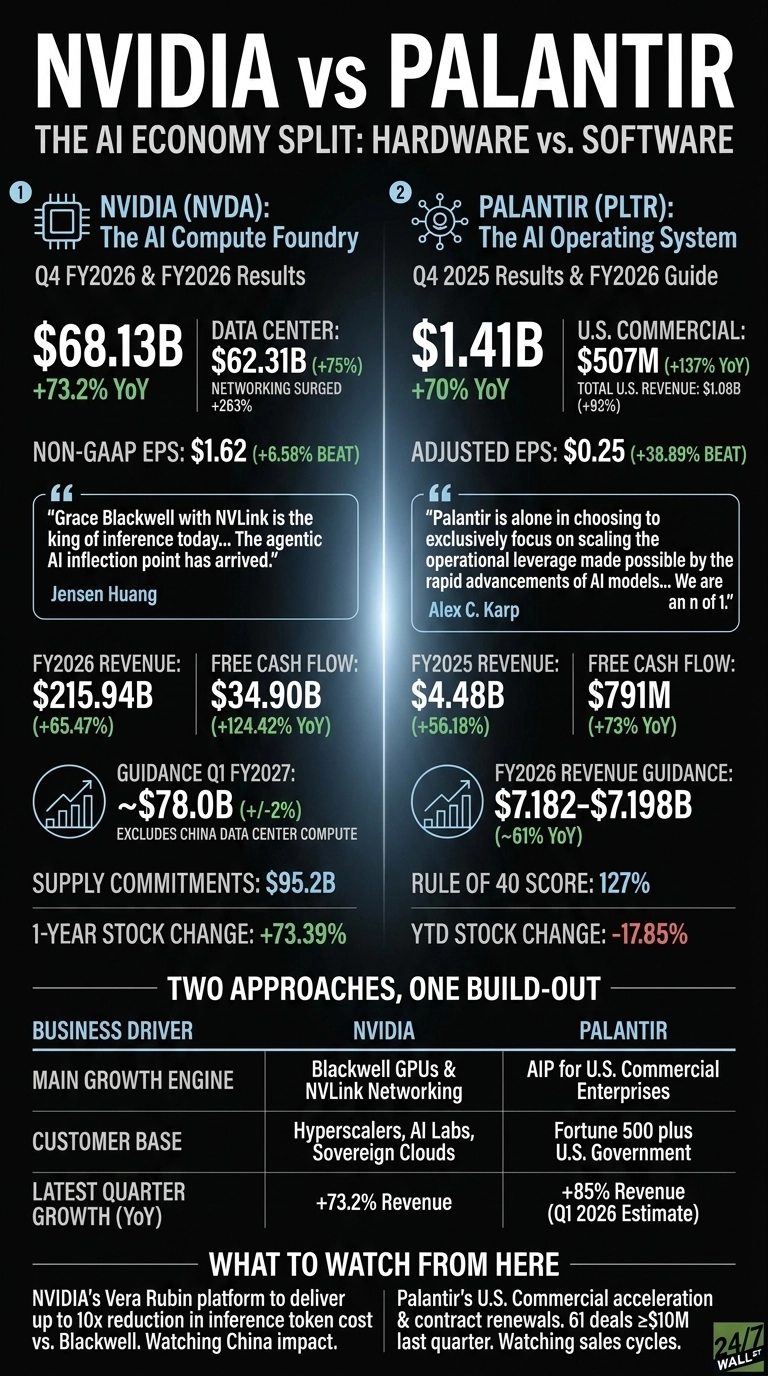

NVIDIA (NASDAQ: NVDA | NVDA Price Prediction) and Palantir (NASDAQ: PLTR) just delivered the cleanest hardware-versus-software split in the AI economy. NVIDIA closed FY2026 with $215.94B in revenue and another Data Center blowout.

Palantir followed up with Q1 2026 revenue of $1.633B, up 85% year over year, the fastest growth it has ever reported as a public company. Two reports, one AI build-out, very different exposures.

Blackwell Floods the Data Center. AIP Floods the C-Suite.

NVIDIA’s Data Center segment generated $62.31B in Q4 FY2026, up 75%, with networking surging 263% as NVLink fabrics shipped inside GB200 and GB300 racks. Non-GAAP EPS came in at $1.62, beating the $1.52 consensus. Jensen Huang told investors “Grace Blackwell with NVLink is the king of inference today”, and the guide reflected it: $78.0B for Q1 FY2027, even with China Data Center compute revenue stripped out.

| Business Driver | NVIDIA | Palantir |

| Main Growth Engine | Blackwell GPUs and NVLink networking | AIP for U.S. commercial enterprises |

| Customer Base | Hyperscalers, AI labs, sovereign clouds | Fortune 500 plus U.S. government |

| Latest Quarter Growth | 73.2% revenue YoY | 85% revenue YoY |

Palantir is selling the layer above the silicon. U.S. Commercial revenue hit $595M, up 133% year over year, and adjusted EPS landed at 33 cents, beating the 28 cent estimate. Alex Karp framed it bluntly, calling Palantir “an n of 1” focused on what he calls commodity cognition. Customer count keeps climbing, and management raised the FY2026 revenue guide to $7.66B, roughly 71% growth.

One Builds the Factory. The Other Runs the Floor.

The strategic split is sharper than the headline beats suggest. NVIDIA is committing capital like a utility: $95.2 billion of supply commitments and multiyear deals with Meta, OpenAI, Anthropic, and CoreWeave. Vera Rubin is already teed up to deliver up to a 10x reduction in inference token cost versus Blackwell. Margins still expanded, with non-GAAP gross margin reaching 75.2%.

Palantir is taking the opposite shape: capital-light, software-pure, and unusually profitable for a hyper-grower. Karp pointed to a Rule of 40 of 145%, a number historically reserved for chip companies. Adjusted free cash flow of $925M at a 57% margin shows AIP deployments are landing without expensive customization tails. Stock-based comp remains high, and valuation reflects the optimism.

China Risk for One. Sales Cycle for the Other.

I will be watching whether NVIDIA’s Q1 FY2027 actually clears the $78B bar without any China Data Center contribution. Networking is the tell. If the 263% NVLink growth holds even partially, the Blackwell-to-Rubin transition is intact.

Rosenblatt analyst John McPeake raised the firm’s price target to $225 from $200 and keeps a Buy rating on the shares. Palantir’s deal mix is also worth watching. 61 deals of $10M or more last quarter says enterprises are signing real contracts, but termination-for-convenience clauses make every renewal cycle a fresh negotiation.

What To Watch From Here

NVIDIA’s setup rests on backlog, margin profile, and the Vera Rubin roadmap, with shares already up 73.39% over the past year. Palantir’s case rests on growth at scale: 85% reacceleration at multi-billion-dollar revenue is rare, and shares have pulled back 17.85% year to date. If commodity cognition disappoints, the multiple compresses fast. The two stocks offer distinct exposures to the same AI build-out: hardware scale at NVIDIA, software leverage at Palantir.

Contact [email protected] for any questions or corrections.