POET Technologies (NASDAQ:POET) has gone from obscure micro-cap to one of the loudest tickers on WallStreetBets in a matter of weeks. The stock surged 114.72% in the past week alone after announcing a $500 million AI infrastructure deal with Lumilens. After that explosive run, our proprietary model suggests the upside is now stretched.

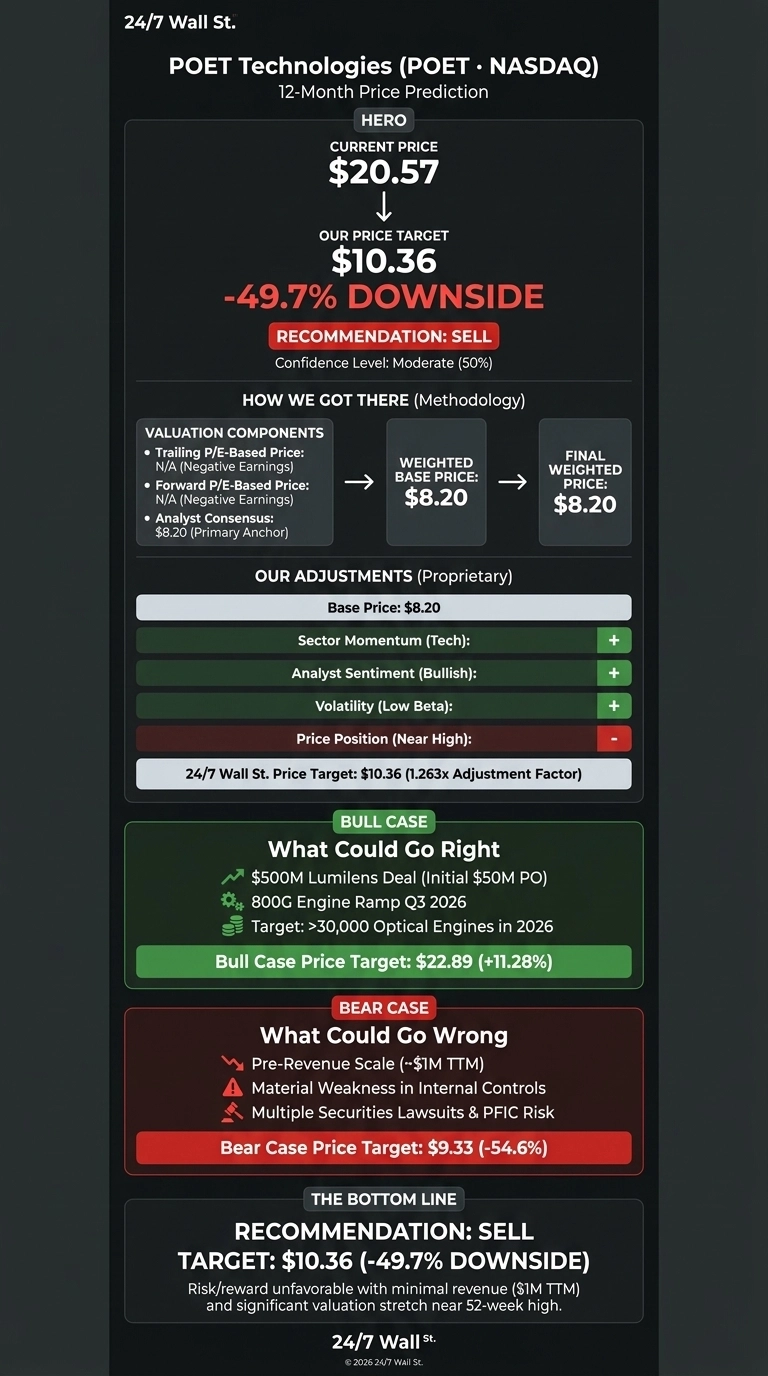

Our 24/7 Wall St. price target for POET is $10.36 over the next 12 months, implying meaningful downside from the current $20.57 quote. The recommendation is sell with moderate confidence.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $20.57 |

| 24/7 Wall St. Price Target | $10.36 |

| Upside/Downside | -49.7% |

| Recommendation | SELL |

| Confidence Level | 50% |

Why We Could Be Wrong on POET

POET is one of the most divisive names in AI photonics, and real value could come from execution on the $500 million Lumilens partnership or the planned ramp of 800G optical engines in Q3 2026. If Malaysia volume manufacturing scales cleanly, the price target could prove far too conservative. Treat our price target as one datapoint. The full bull case appears below.

How a $500M Deal Lit the Fuse

POET is up 206.56% over the past month and 224.96% year to date, with a 43.15% single-day move on May 14 after the Lumilens announcement. The deal carries an initial $50 million purchase order and engineering samples targeted for late 2026.

Q4 2025 revenue came in at $341,202, missing the $700,180 estimate, with full-year FY2025 revenue of just $1,074,865. The stock also weathered a 47.35% single-day plunge on April 23 after Marvell (NASDAQ:MRVL | MRVL Price Prediction) canceled all Celestial AI purchase orders, followed by multiple securities class action lawsuits with a June 29 lead plaintiff deadline.

The Case for $22+

Bulls point to the 800G transceiver market projected to reach $9.8B by 2032 at 22.8% CAGR and the AI GPU server opportunity. CEO Suresh Venkatesan secured $225 million in Q4 2025 plus $150 million in January 2026, leaving roughly $430 million in cash. Management expects to ship more than 30,000 optical engines in 2026. Our model’s bull scenario points to $22.89, an 11.28% return.

What Could Go Wrong

POET trades at a price-to-sales ratio of 2,922 with a TTM EPS of -$0.68 and operating margin of -41.74%. The accumulated deficit sits near $291 million, and management disclosed a material weakness in internal controls.

Bulls fairly counter that the Q4 net loss of $42.67M was largely driven by a $30.69M non-cash derivative warrant liability adjustment that should disappear after USD repricing. Still, the bear scenario lands at $9.33.

The Risk Isn’t Worth the Reward Here

Our 24/7 Wall St. price target is $10.36 with a sell recommendation and 50% confidence. The tipping factor is the gap between a roughly $3.14 billion market cap and roughly $1 million in trailing revenue.

The setup would look more attractive if Lumilens production orders convert into recognized revenue in 2027 and the securities litigation resolves cleanly. The risk/reward looks unfavorable while POET trades near the $20.81 52-week high with lawsuits pending.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $10.36 |

| 2027 | $9.10 |

| 2028 | $7.85 |

| 2029 | $6.70 |

| 2030 | $5.83 |

These projections assume POET continues to scale Malaysia manufacturing without securing a transformational hyperscaler design win. Significant upside could come from successful Lumilens execution or a competitor acquiring POET for its photonic interposer technology.

Contact [email protected] for any questions or corrections.