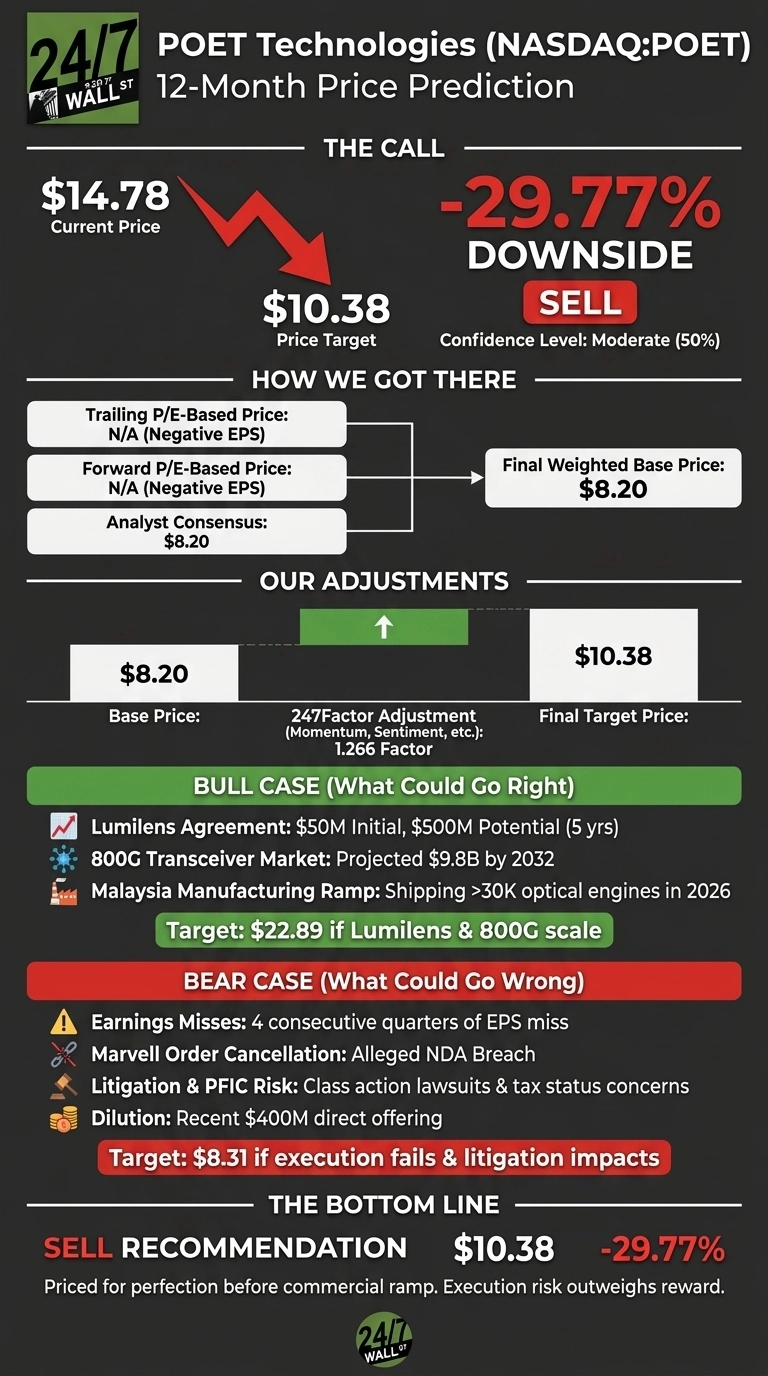

POET Technologies (NASDAQ:POET) has been one of the wildest small-cap AI infrastructure stories of 2026, with shares riding a 133.49% year-to-date rally on a marquee Lumilens supply agreement. After running this name through our proprietary model, the rally has gotten ahead of the fundamentals. Earlier this month, we’d a buy call for the stock with a target of $10.51. Now that the stock has hit $14, our latest call changes.

Our 24/7 Wall St. price target for POET is $10.38, implying -29.77% downside from the current $14.78 quote. The recommendation is sell, with moderate confidence of roughly 50%.

| Metric | Value |

|---|---|

| Current Price | $14.78 |

| 24/7 Wall St. Price Target | $10.38 |

| Upside/Downside | -29.77% |

| Recommendation | SELL |

| Confidence Level | 50% |

Why We Could Be Wrong

POET is divisive, and real upside could come from the $500 million five-year Lumilens commercial ramp or successful 800G shipments from Malaysia in Q3 2026. Consider our price target one datapoint among many.

The Rally, The Lawsuit, and a Whiplash Stock

POET is up 72.06% over the past month and 216.49% over the past year, cooling 28.15% since May 14.

The rally was triggered by a joint development deal with Lumilens carrying an initial $50 million purchase order and a paired $400 million direct offering from a single institutional investor. Q1 2026 revenue of $503,389 topped expectations, but EPS came in at -$0.08, missing expectations and pushing the net loss to $12.34 million. Overhanging the story are securities class action lawsuits tied to PFIC tax status and an alleged NDA breach that cost POET its Marvell/Celestial AI orders.

The Case for $22+

Bulls have a credible story. The 800G transceiver market is projected at $9.8 billion by 2032 with a 22.8% CAGR, and POET’s Optical Interposer slots directly into co-packaged optics demand.

Management guided to shipping more than 30,000 optical engines in 2026, with $430 million in cash to fund the Malaysia ramp. CEO Suresh Venkatesan called Lumilens “an important commercial milestone” that could become “a substantial long-term supplier relationship supporting frontier AI infrastructure.” The bull case scenario lands at $22.89, a 54.88% return.

What Could Go Wrong

The bear case is specific. POET has missed EPS in four consecutive quarters, the most recent Q1 reaction was a -22.36% single-day drop, and a Night Market Research short report on May 16 questioned past partnerships.

Multiple law firms are organizing class actions over alleged misrepresentation of PFIC tax status with a lead plaintiff deadline of June 29, 2026. Seeking Alpha rated shares Sell on May 5, citing heavy dilution and loss of the Marvell relationship.

The widened Q1 loss reflects a smaller non-cash warrant gain of $1.60 million vs $15.38 million a year ago rather than operational deterioration. The bear case projects $8.31, a -43.77% outcome.

POET Price Prediction 2026-2030

The 24/7 Wall St. price target of $10.38 reflects a stock that has priced in a commercial ramp not yet shipped. The thesis improves if POET delivers material Lumilens revenue and 800G volume from Malaysia in the second half of 2026. The setup weakens if litigation drags on or 800G timing slips into 2027.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $10.38 |

| 2027 | $9.50 |

| 2028 | $8.75 |

| 2029 | $8.30 |

| 2030 | $7.91 |

These projections assume POET executes on its Malaysia ramp without further reputational shocks. Significant upside could come from converting the Lumilens framework into recurring revenue, while litigation outcomes or further dilution would skew the trajectory lower.

Contact [email protected] for any questions or corrections.