If you’ve been parking cash in Treasury bills, you know the routine: log into TreasuryDirect, place an auction bid, wait for settlement, then repeat the process every four, eight, or 13 weeks as each bill matures. It works, but it’s friction-heavy — and for investors who want competitive short-duration yield without managing a ladder, there’s a simpler path trading on the open market every day.

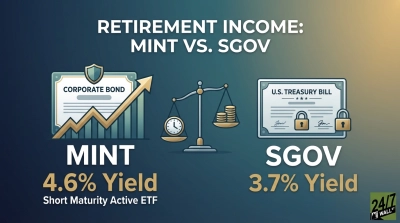

PIMCO Enhanced Short Maturity Active ETF (NASDAQ:MINT) returned roughly 5% over the past year edges roughly 4% 1-year T-Bill yield without auction or rollover hassle. Monthly payouts ran from $0.33 to $0.40 per share, with price near $100. The tradeoff is credit exposure through corporate holdings. MINT suits cash investors seeking intraday liquidity and continuous income over Treasury ladders.

Why MINT Isn’t Just Another Bond Fund

MINT is one of the largest actively managed ultra-short duration ETFs on the market, run by PIMCO — the firm that effectively invented active fixed income management. Unlike a passive T-bill ETF that simply rolls the shortest end of the Treasury curve, MINT’s portfolio managers pick across investment-grade corporate paper, asset-backed securities, commercial paper, and government debt with weighted average maturities typically under one year. The goal is to capture a yield premium over pure Treasuries while keeping interest-rate risk minimal.

That active approach matters in a flattening or inverted curve environment. When short Treasury yields drift lower as the Fed signals cuts, MINT’s managers can lean into corporate credit spreads or floating-rate notes to keep distributions elevated. It’s the kind of flexibility a static T-bill ladder simply can’t replicate.

The Liquidity Advantage Over T-Bills

Here’s the part T-bill investors often underestimate: liquidity. A Treasury bill is liquid in theory, but if you need cash mid-cycle, you’re either waiting for maturity or selling on the secondary market with potential price concessions. MINT trades on Nasdaq throughout the session at tight bid-ask spreads, meaning you can move in or out with a single click and have settled cash in two business days.

That intraday execution also means no auction calendars to track, no reinvestment timing decisions, and no idle cash sitting between maturity and the next bill purchase. For investors managing six-figure cash reserves or corporate treasury accounts, eliminating that drag alone can justify the modest expense ratio.

Monthly Income, Not Quarterly Lump Sums

MINT distributes income monthly, which appeals to retirees and cash-flow-focused investors who’d rather see a steady drip than wait for a T-bill to mature in one chunk. Distributions reflect the underlying coupon income from the portfolio, so they move with prevailing short rates — rising when the front end repriced higher, easing when the Fed pivots dovish.

The fund’s net asset value stays remarkably stable, typically hovering in a narrow band around its target price. Price volatility is minimal compared with intermediate or long-duration bond funds, making MINT closer in behavior to a money-market fund than a traditional bond ETF — but with the yield advantage of going slightly out the credit curve.

The Credit Risk Tradeoff

Nothing in markets is free, and MINT’s yield pickup comes from taking on credit risk that Treasury bills don’t carry. The portfolio holds investment-grade corporate bonds and structured paper, which means in a severe credit-market shock — think March 2020 — the NAV can dip briefly as spreads widen. MINT did experience a short, sharp drawdown during that episode before recovering within weeks as the Fed backstopped short-term credit markets.

For most investors, that’s an acceptable tradeoff. Investment-grade short paper from blue-chip issuers carries minimal default risk over a sub-one-year horizon, and PIMCO’s credit research team has decades of experience navigating these markets. Still, MINT is not a Treasury substitute for the most conservative portion of an emergency fund — it’s a step up the risk-return ladder, not a parallel choice.

Who Should Consider MINT

MINT fits investors who want a competitive yield on cash without the operational overhead of running a T-bill ladder, who value intraday liquidity, and who are comfortable with marginal credit exposure in exchange for higher distributions. It works well inside taxable brokerage accounts, IRAs, and as a parking spot for funds awaiting deployment into equities or longer-duration bonds.

Investors who need state-tax exemption on interest income (a Treasury-only feature) or who want zero credit risk should stick with T-bills or a pure government money-market fund. For everyone else, MINT offers a cleaner, more flexible path to the same outcome: earning meaningful income on cash without locking it up or working a calendar.

Contact [email protected] for any questions or corrections.