Marvell Technology (NASDAQ:MRVL | MRVL Price Prediction) has staged one of the most remarkable AI-driven rallies in semiconductors, with shares climbing 179.33% over the past year on the back of custom silicon momentum and a deepening role in hyperscaler AI infrastructure. After a 95.49% year-to-date surge, the question is whether the price has run ahead of the fundamentals.

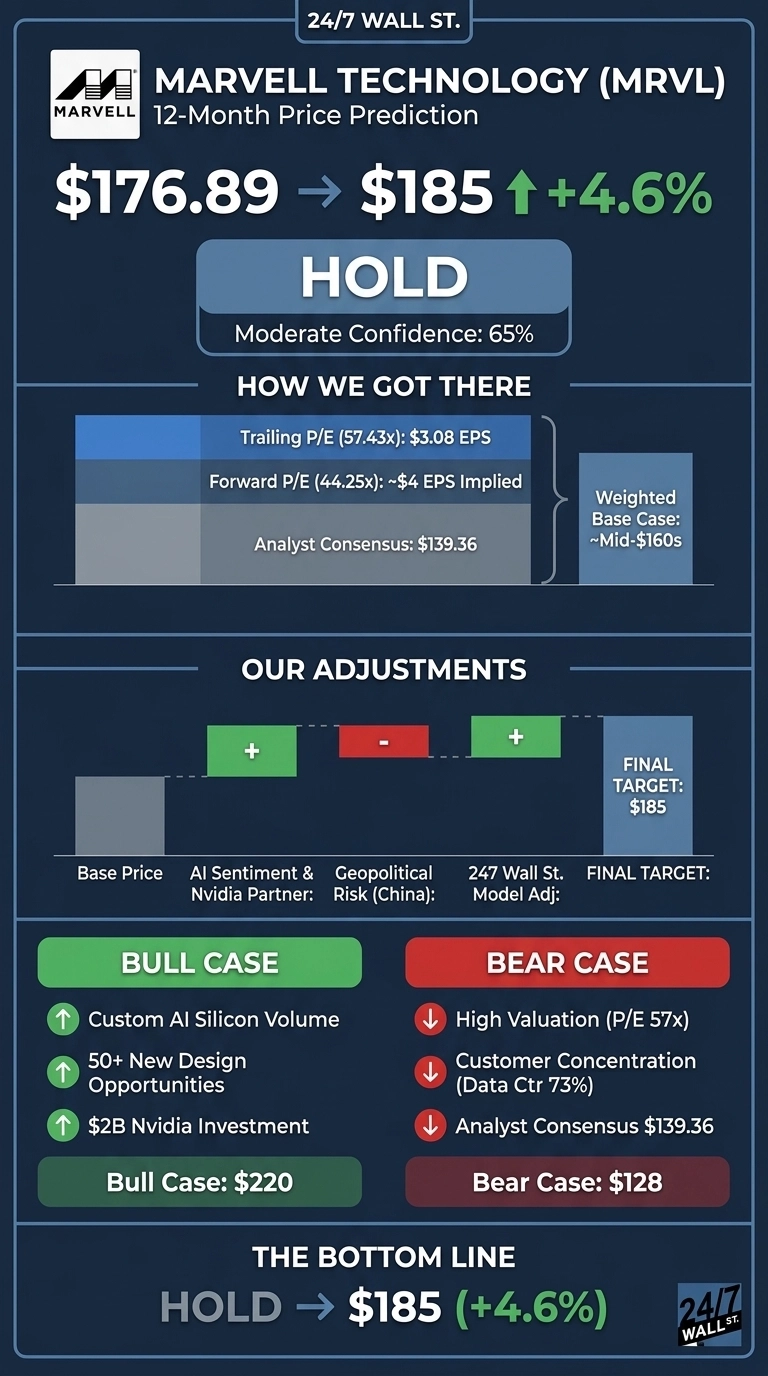

Our 24/7 Wall St. price target for Marvell is $185, implying a modest 4.6% upside from the current price of $176.89. Our recommendation is hold, with moderate confidence at 65%.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $176.89 |

| 24/7 Wall St. Price Target | $185 |

| Upside/Downside | +4.6% |

| Recommendation | HOLD |

| Confidence Level | 65% |

An AI Custom-Silicon Story Trading at Full Valuation

Marvell trades just below its 52-week high of $192.15, well above the 52-week low of $58.45. Shares are up 25.1% in the past month alone.

The most recent quarter, Q3 FY2026, delivered record revenue of $2.07 billion, up 37% YoY, with data center sales of $1.52 billion (73% of total) growing 38% YoY. Non-GAAP EPS came in at $0.76 versus $0.43 a year earlier.

News flow has reinforced the AI narrative. Recent sentiment data cites a $2 billion Nvidia investment and deeper custom AI chip collaboration, alongside design discussions with Alphabet and exposure to Amazon’s $225 billion Trainium backlog. The pending Celestial AI acquisition extends Marvell’s optical interconnect roadmap for AI datacenters.

Why Bulls See a Breakout Ahead

The bull case rests on volume monetization of custom AI silicon. Management cited 50-plus new custom AI design opportunities across 10-plus customers, and full-year FY2026 revenue growth is guided above 40%.

BofA Securities raised its target citing a larger long-term AI networking opportunity, and Trefis modeled a path toward $400 if earnings quadruple and the multiple holds. With 36 Buy or Strong Buy ratings against just six Holds, a $220 bull-case scenario looks reasonable if FY2027 data center growth accelerates.

The Risks Worth Watching

Marvell’s P/E of 57 and price-to-sales of 19x leave little margin for execution slips. The consensus analyst target of $139.36 sits well below the current price, implying meaningful downside if AI sentiment cools. Customer concentration is steep, with data center generating roughly three-quarters of revenue, and hyperscalers building in-house ASICs remains a longer-term threat.

Bulls would counter that the recent insider selling partly reflects mechanical 10b5-1 plan execution after a 165% rally rather than a fundamental view shift. A bear-case scenario takes shares back toward the 50-day moving average near $128.

Marvell Price Prediction 2026-2030

My 24/7 Wall St. price target for Marvell is $185, a hold with 65% confidence. The tipping factor is valuation. The AI thesis is intact, but the stock already reflects most of it. I would be a buyer if the May 27 Q1 FY2027 earnings call shows another guidance raise and custom silicon revenue accelerating. I would stay on the sidelines if the data center mix softens or margins compress.

Looking further ahead, here is where our model projects Marvell could trade in the coming years, assuming current AI infrastructure trajectories and margin expansion hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $185 |

| 2027 | $215 |

| 2028 | $245 |

| 2029 | $275 |

| 2030 | $310 |

These projections assume Marvell continues executing on its custom AI silicon roadmap and reaches the reported $15 billion revenue target by fiscal 2028. Significant upside or downside could result from hyperscaler insourcing trends or China-related trade actions.

Contact [email protected] for any questions or corrections.