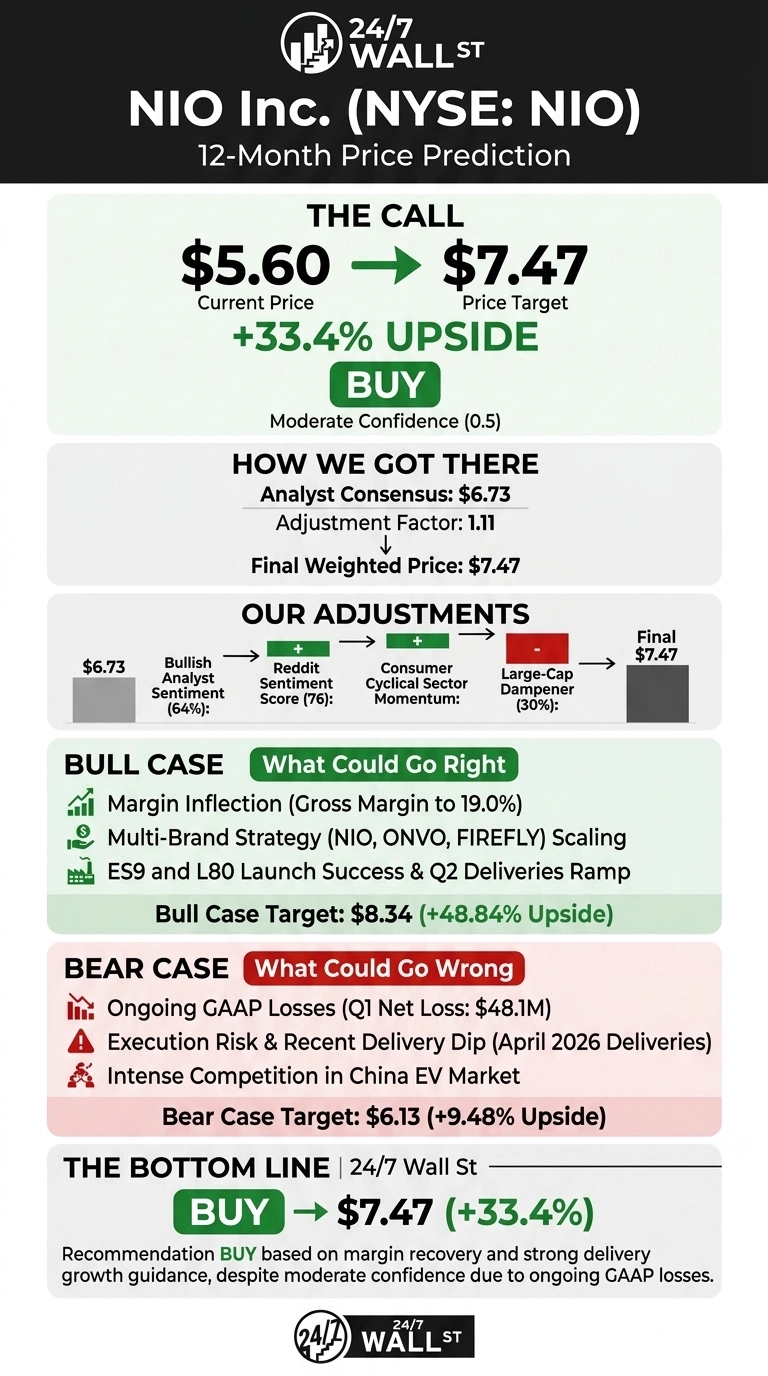

Our NIO (NYSE:NIO | NIO Price Prediction) call comes after a turbulent month for the Chinese smart EV maker, with shares down 10.4% over the past week and trading at $5.60.

The 24/7 Wall St. price target for NIO is $7.47, implying 33.4% upside over the next 12 months. Our recommendation is buy, with moderate confidence reflecting NIO’s improving fundamentals offset by ongoing GAAP losses.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $5.60 |

| 24/7 Wall St. Price Target | $7.47 |

| Upside | 33.4% |

| Recommendation | BUY |

| Confidence Level | 50% |

A Volatile Run Into a Major Product Cycle

NIO has had a wild ride. Shares are up 42.13% over the past year and 9.8% year to date, yet the stock is down 12.91% over the past month and sits 16% below its 52-week high of $8.02.

Q1 FY26 results, reported May 21, 2026, showed revenue of $3.70 billion, EPS of -$0.03, and deliveries of 83,465 units, up 98.3% year over year. Vehicle margin hit 18.8%, the fourth consecutive sequential improvement.

Management guided Q2 deliveries to 110,000 to 115,000 vehicles with revenue of $4.75 billion to $4.99 billion, supported by the NIO ES9 SUV (deliveries beginning May 27, 2026) and the ONVO L80.

Why Bulls See a Breakout Ahead

The bull case rests on a real margin inflection. Gross margin expanded to 19% from 7.6% YoY, R&D fell 40.7% YoY, and SG&A dropped 20.5% YoY. NIO already printed its first GAAP profit in Q4 2025 at $0.04 EPS, with quarterly net income of $40.4 million.

The All-New ES8 ranked first in China’s large SUV segment for five consecutive months, and the multi-brand strategy is scaling. If Q2 deliveries land at the high end and ES9 ramps quickly, the bull-case scenario points to $8.34, or 48.84% upside.

What Could Go Wrong

NIO still operates at a GAAP loss, posting a $48.1 million net loss in Q1 and a $2.14 billion full-year 2025 loss. Prior filings carried going concern language, and current liabilities exceeded current assets at year-end. April 2026 deliveries of 29,356 vehicles trailed the Q1 monthly pace, raising execution risk.

Bulls counter that Q1 generated $66.8 million in non-GAAP adjusted operating profit and that elevated spending reflects the ES9 and L80 ramp. The bear-case scenario still finishes higher at $6.13, or 9.48% upside, supported by the $3.34 52-week low floor.

The Bottom Line on NIO

My verdict matches the model: Buy, with a 24/7 Wall St. price target of $7.47 and 50% confidence. The deciding factor is the margin trajectory paired with triple-digit delivery growth guidance.

The bullish setup strengthens if Q2 deliveries confirm the 110,000-plus ramp and the ES9 launch holds pricing. The thesis weakens if vehicle margin slips below 17% or if cash burn re-accelerates ahead of another raise.

NIO Price Prediction 2026-2030

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $7.47 |

| 2027 | $8.53 |

| 2028 | $9.74 |

| 2029 | $11.12 |

| 2030 | $12.69 |

These projections assume NIO sustains its margin expansion and that the ES9, ONVO, and FIREFLY brands hold share against an intensely competitive China EV market. Significant upside or downside could come from further pricing wars, regulatory shifts on Chinese ADRs, or a faster-than-expected swing to durable GAAP profitability.

Contact [email protected] for any questions or corrections.