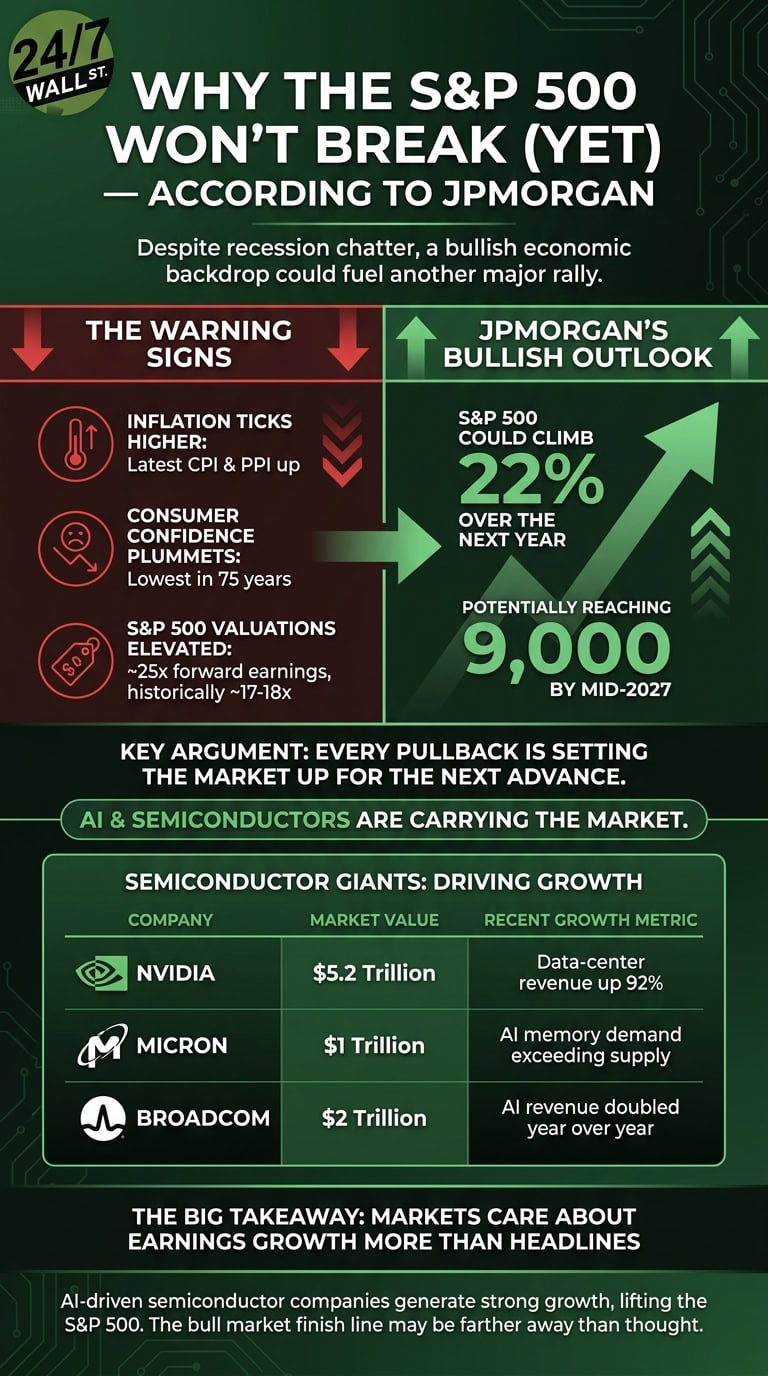

Everywhere investors look, the warning signs seem to be multiplying. Inflation ticked higher again in the latest Consumer Price Index report from the Bureau of Labor Statistics. Producer prices are climbing, too, raising concerns companies may eventually pass those costs onto consumers. The University of Michigan’s consumer confidence index recently hit its lowest reading in 75 years. Meanwhile, the S&P 500 trades near historically elevated valuations after a massive run higher after last year’s April’s crash.

So why does the stock market keep refusing to break?

That question is becoming harder for bears to answer. Despite nonstop recession chatter and growing concerns that President Donald Trump’s bull market is running out of steam, not everyone thinks a crash is around the corner. In fact, according to a recent outlook from JPMorgan Private Bank, the S&P 500 could climb another 22% over the next year — potentially reaching 9,000 by mid-2027. That would mark another historic leg higher for the index.

JPMorgan Says Pullbacks Are Fuel, Not Failure

The core argument JPMorgan is making runs directly against the current mood on Wall Street. The bank acknowledges risks are building. Higher inflation, slowing consumer activity, and stretched valuations are all real concerns. Granted, the S&P 500 currently trades around 25 times forward earnings — well above its historical average closer to 17 or 18 times, according to FactSet data.

Yet JPMorgan argues that every pullback is setting the market up for the next advance. That matters because investors have repeatedly expected this rally to collapse under the weight of higher interest rates, slowing growth, or geopolitical stress. Instead, each dip has become another buying opportunity.

Importantly, JPMorgan does not call its 22% upside target the “base case” scenario. Rather, it describes the move as “entirely plausible” under a bullish economic and earnings backdrop. In other words, the firm is not predicting perfection — it is saying the conditions exist for another major rally if earnings growth keeps outpacing expectations.

Surprisingly, much of that optimism comes down to one sector.

Semiconductors Are Carrying the Market Again

According to JPMorgan, technology — particularly semiconductors tied to artificial intelligence infrastructure — remains the engine powering the broader market higher.

Micron Technology (NASDAQ:MU | MU Price Prediction) has become the latest example. Its stock surged nearly 20% yesterday after investors digested fresh evidence that AI-driven memory demand is still outrunning supply, causing an analyst to hike his price target from $535 to $1,625 per share.

The move pushed Micron above a $1 trillion valuation for the first time, making it the market’s newest trillion-dollar company. The milestone matters for more than bragging rights.

The S&P 500 is weighted by market capitalization, meaning larger companies exert greater influence over the index’s direction. With Micron now ranking as the 11th-largest company in the index, its performance increasingly impacts the broader market itself.

And Micron is hardly alone.

Nvidia (NASDAQ:NVDA) is at a staggering $5.2 trillion valuation as demand for AI accelerators, GPUs, and data-center hardware continues to expand. According to Nvidia’s latest earnings release, data-center revenue rose 92% year over year, showing AI infrastructure spending remains in full sprint mode.

Here’s what the numbers tell us:

| Company | Market Value | Core AI Exposure | Recent Growth Metric |

| Micron | $1 trillion | High-bandwidth memory | AI memory demand exceeding supply |

| Nvidia | $5.2 trillion | AI GPUs/data centers | Data-center revenue up 92% |

| Broadcom (NASDAQ:AVGO) | $2 trillion | AI networking/custom chips | AI revenue doubled year over year |

Regardless of how you look at it, the companies driving the S&P higher are still generating massive revenue growth tied directly to AI spending.

Valuations Look Expensive — But Earnings Keep Climbing

That said, skeptics are not wrong to worry about valuations. The market is expensive by almost every traditional metric. Consumer spending is softening. Manufacturing activity remains uneven. Treasury yields remain elevated compared to the easy-money era that fueled earlier rallies.

But bull markets rarely die simply because valuations look high. Historically, they end when earnings collapse or liquidity dries up. Right now, neither has fully happened. In fact, the opposite may be occurring inside AI-linked sectors where demand continues outpacing available supply.

Memory chips are a perfect example. AI data centers require enormous amounts of high-bandwidth memory, and supply constraints have allowed companies like Micron to command stronger pricing power. That creates expanding margins and rising earnings estimates — two things the market rewards aggressively.

Ultimately, JPMorgan’s bullish outlook comes down to one simple thesis: the AI investment cycle may still be in its early innings.

Key Takeaway

The economic cracks forming beneath the surface are real. Inflation is sticky. Consumer confidence is weak. Valuations are elevated. Smart investors should not ignore those risks. But markets care about earnings growth more than headlines.

Right now, AI-driven semiconductor companies continue generating the strongest growth anywhere in the market, and because they now dominate the S&P 500 by weight, their momentum can keep lifting the broader index higher. Coupled with Nvidia’s renewed strength and Micron’s sudden rise into the trillion-dollar club, JPMorgan’s argument for another major leg higher no longer sounds far-fetched.

The Trump bull market may eventually end. Every bull market does. JPMorgan’s point is that the finish line may still be much farther away than many investors think.

Contact [email protected] for any questions or corrections.