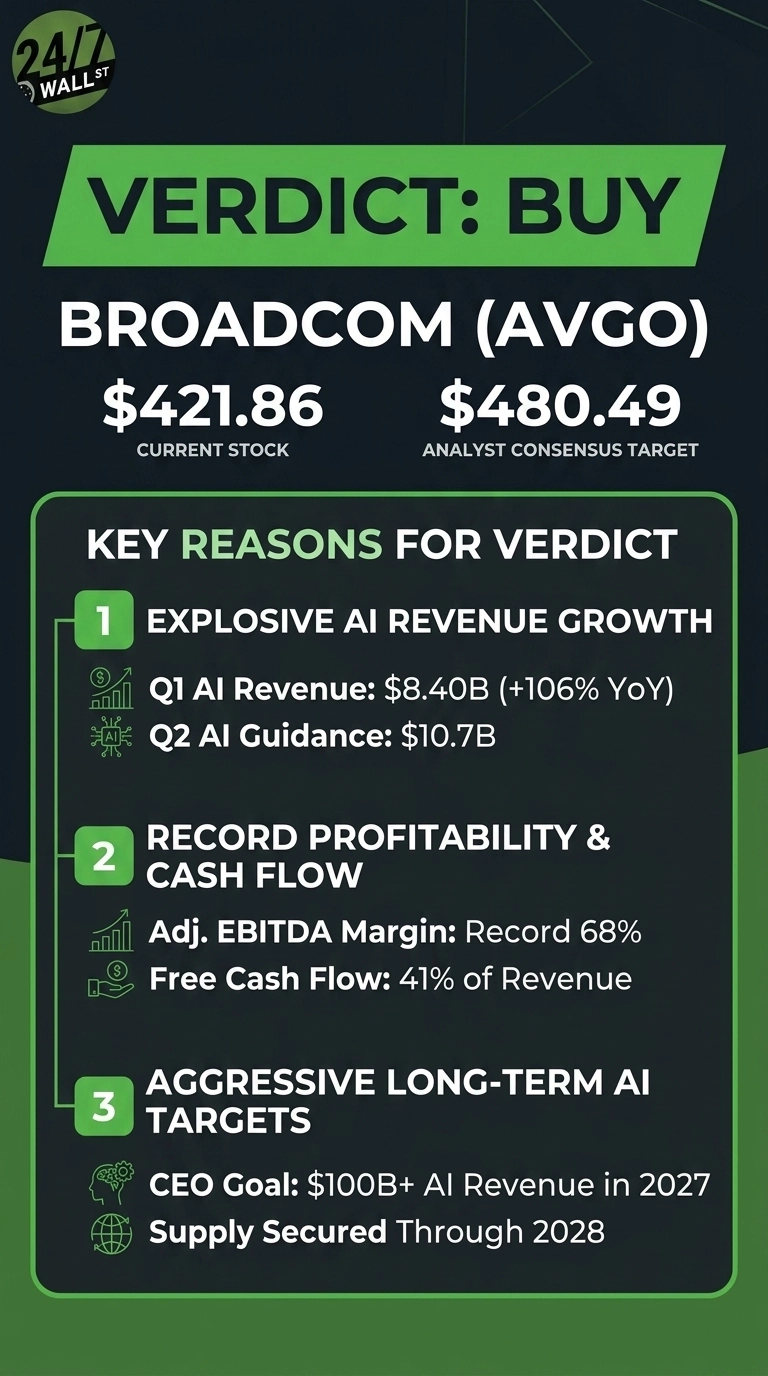

At $421.86, Broadcom (NASDAQ:AVGO | AVGO Price Prediction) is testing resistance. With shares pressing against a 52-week high of $442.36 and earnings days away, the question of whether to chase, fade, or wait deserves a direct answer.

Broadcom designs custom AI accelerators, networking silicon, and infrastructure software for the world’s largest hyperscalers, with VMware anchoring its software arm.

The stock has roughly doubled off its 52-week low after a string of AI-driven beats, and the market cap now sits near $1.99 trillion. CEO Hock Tan has reframed the company around custom XPUs for frontier AI labs, and guidance keeps moving up.

Why The Setup Into Earnings Looks Loaded

AI semiconductor revenue hit $8.40 billion in Q1 FY2026, up 106% year over year, and management guided Q2 AI revenue to $10.7 billion. Total Q2 revenue is guided to roughly $22 billion, up 47% year over year. Polymarket traders assign a 94.4% probability that Broadcom beats next week.

Q1 adjusted EBITDA margin hit a record 68%, free cash flow ran at 41% of revenue, and the company authorized a $10 billion buyback through December 31, 2026. Tan reiterated visibility to “in excess of $100 billion” in AI chip revenue in 2027, with capacity locked in through 2028.

Why The Price Already Reflects A Lot Of Good News

The bear case begins with valuation. Shares trade at 82 trailing earnings and 37 forward earnings, with an EV/EBITDA near 54. That leaves no room for a soft quarter, a hyperscaler capex pause, or slippage in the OpenAI, Anthropic, Google, or Meta XPU roadmaps that Tan has staked the thesis on.

Director Henry Samueli disposed of more than one million shares in late March, and CEO Hock Tan sold 22,000 shares on April 8. The CFO, both segment presidents, and the chief legal officer also unloaded stock in the $317 to $370 range. Customer concentration remains acute, with six strategic XPU customers driving the AI narrative.

Why Waiting For The June Report Has Appeal

The hold case rests on timing. Q2 results land on June 3, 2026, and guidance on AI networking mix or 2027 gigawatt deployment could reset the multiple in either direction. Reddit sentiment has cooled from very bullish in mid-May to merely bullish into the report, hinting at exhaustion near the highs.

What The Numbers Say

Shares trade at $421.86 against a consensus analyst target of $480.49, implying roughly 14% upside. The breakdown across 46 analysts skews heavily constructive:

- Strong Buy: 7

- Buy: 36

- Hold: 3

- Sell: 0

Broadcom is up 22.14% year to date and 80.46% over the past year, against the S&P 500’s 10.05% YTD and 26.95% one-year gains. The 200-day moving average sits at $349.84.

The Verdict: The AI Compounding Story In Focus

At $421.86, Broadcom sits at a pivotal level heading into earnings.

The path to appreciation runs through the June 3 earnings report and the 2027 AI roadmap. A Q2 beat on the $10.7 billion AI guide, paired with upward revision toward Tan’s $100 billion 2027 framing, gives this multiple oxygen. Custom accelerator revenue grew 140% year over year in Q1, and OpenAI’s first-generation XPU deploys at over 1 gigawatt in 2027.

The risk/reward at this price is defensible because supply is locked through 2028, gross margins are not diluting as AI scales, and the buyback absorbs share creep.

The thesis breaks if a major hyperscaler accelerates customer-owned tooling enough to displace Broadcom’s XPU pipeline, or if Q2 networking mix disappoints. Watch the AI networking percentage of total AI revenue, which Tan expects to climb to 40% in Q2.

When the dominant customer in custom silicon prints 100% AI growth and guides higher, paying a premium has historically been rewarded by the market.

Contact [email protected] for any questions or corrections.