Broadcom (NASDAQ:AVGO | AVGO Price Prediction) posted record revenue of $22.19 billion on June 3, 2026, beat consensus on the top and bottom line, raised guidance, and lost roughly a fifth of its market value over the following week. The stock went from $495 at the filing to $385.73 one day later. The broader chip complex dropped alongside it. AVGO sits at $395 as of this writing, still down 4% while SPY is down 0.3% over the same window.

What JPMorgan is actually saying

Late on last week, JPMorgan reiterated its Overweight rating with a $580 price target and told clients to be “aggressive buyers” of Broadcom at current levels.

The thesis rests on two arguments the bank thinks the market is mispricing. First, that Broadcom’s dominance in advanced packaging is being underestimated. Second, that the AI chip development program with Google is on track despite recent supply chain noise. Shares jumped over 4% on the call, and the most recent session added 4.7%.

The numbers that triggered the selloff are the same numbers supporting the bull case

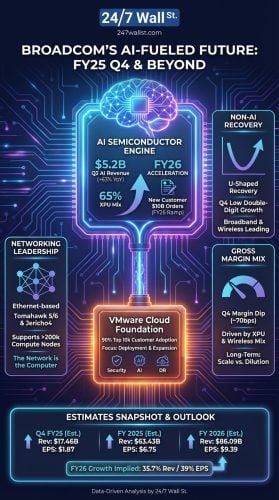

AI semiconductor revenue grew 143% year-over-year to $10.80 billion, beating Broadcom’s own guidance. CEO Hock Tan guided Q3 AI revenue to $16 billion, up over 200%, and disclosed that Q2 alone produced over $30 billion in AI bookings. For full-year 2026 the company expects $56 billion in AI semiconductor revenue, up approximately 180% from fiscal 2025, prior target of more than $100 billion in 2027.

Tan described the demand environment as “demand for XPUs and networking is simply insatiable.” and named the customers funding it. Anthropic gets access to more than 1 gigawatt of TPU-based compute in 2026 and another 5 gigawatts starting in 2027. OpenAI is contractually committed to deploy 1.3 gigawatts in 2027, on the way to a previously announced 10-gigawatt agreement by 2029. Meta committed to 3 gigawatts of MTIA XPUs through 2028. Two unnamed core customers have already placed $6 billion in purchase orders.

So why did the stock collapse?

Three reasons explain it. Valuation, customer concentration, and a Nasdaq-wide chip rout. AVGO trades at 65 times trailing earnings and 33 times forward earnings, with a market capitalization of $1.87 trillion. The six-customer concentration is real, and Tan acknowledged that within Google specifically, “we fully expect that there will be some diversity of sources for them.”

On June 16, the Philadelphia Semiconductor ETF fell 5.9% on FOMC day, with Intel down 8.4% and AMD down 7.3%. AVGO went with them. The supporting filing detail is in the company’s Q2 FY2026 8-K.

The contrarian read on retail panic

Reddit’s r/wallstreetbets briefly turned into a confessional. One post titled “wealthsimple exercised AVGO puts after hours. i’m down 1.2 million. is it over” drew 5,229 upvotes. Within 48 hours, a counter-narrative emerged on r/stocks: “Broadcom’s drop looks way overdone to me” picked up 204 upvotes and 130 comments.

Polymarket’s resolved record on AVGO earnings predictions is 100% correct across 6 markets, though the same crowd assigns essentially zero probability to AVGO becoming the second or third largest company by June 30.

What to weigh against the JPMorgan call

Wall Street consensus sits at $522.06 with 37 buy ratings and 7 strong buys against 4 holds and zero sells. Insiders have been net sellers across 35 recent transactions. CFO Kirsten Spears flagged a structural margin headwind, noting that “our ASICs, TPUs, and some of the wireless business have lower margins” and that consolidated gross margin will compress as AI scales. Q3 gross margin is guided down to roughly 74%.

The JPMorgan trade bets the market mistook a mix-shift margin story and a sector tantrum for something fundamentally broken. Backlog visibility now extends into 2028, and gigawatt demand from Anthropic and OpenAI is, in Tan’s words, “far ahead of what we expected six months ago.” If that holds, $411 looks like a gift. If hyperscaler capex blinks, the multiple has a long way to fall.

Contact [email protected] for any questions or corrections.