Everyone is piling into NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) after another blowout quarter that pushed revenue to $81.61 billion and the market cap past $5.14 trillion, and the AI hype machine keeps printing headlines about agentic compute and unstoppable hyperscaler spend.

The underlying setup deserves a closer look.

The Crowded Trade Nobody Wants to Talk About

NVIDIA is the most concentrated bet on the planet. At a trailing P/E of 33 and a price-to-book of 27, you are paying peak-cycle prices for a chip business whose largest customers are openly building competing silicon. Roughly 50% of Data Center revenue flows from a handful of hyperscalers (Meta, Microsoft, Google, Amazon), China compute is excluded from forward guidance entirely, and supply commitments have ballooned to $119.0 billion. CEO Jensen Huang frames the AI buildout as “the largest infrastructure expansion in human history,” the kind of peak-cycle rhetoric that should make a retirement investor flinch. Shares are down 4.86% over the past week. Multiple compression has already started whispering.

Layer in the macro. With $39 trillion in U.S. debt and incoming Fed Chair Kevin Warsh signaling an end to the reflexive “Fed Put” and a re-evaluation of traditional inflation targeting, the cheap-money tailwind that inflated mega-cap tech multiples is about to flip. A divided FOMC tolerating higher capital costs is a wrecking ball for any stock priced for perfection.

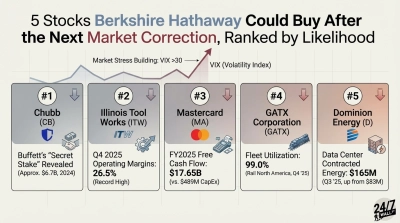

The Monopoly Hiding in Plain Sight

That brings us to Berkshire Hathaway (NYSE:BRK-B). Three reasons it warrants a closer look.

1. Valuation with an actual margin of safety. BRK-B trades at a P/E of 10 and a price-to-book of 0.94, below stated book value. You are buying a diversified collection of operating businesses (GEICO, BNSF, Berkshire Hathaway Energy, plus a sizable Apple stake) at a discount to balance-sheet math. Free cash flow yield sits at 3.73% and earnings yield at 9.98%. These are the kind of metrics long-duration, income-oriented portfolios tend to favor.

2. A fortress balance sheet that benefits from a hawkish Fed. Debt-to-equity is 0.19, interest coverage runs 11.62x, and net debt-to-EBITDA is 1.20. Berkshire’s mountain of Treasury bills throws off billions in pure interest income when the Fed stays restrictive. Higher capital costs punish NVIDIA’s customers; they pay Berkshire. A beta of 0.622 indicates materially lower sensitivity to broad market drawdowns.

3. Toll-booth economics that ignore the AI cycle. Insurance float, freight rail monopoly economics at BNSF, regulated utility cash flow, and inelastic pricing power across essential infrastructure generate durable earnings whether hyperscaler capex slows or not. Vice Chairman Greg Abel personally accumulated 25 Class A shares across $725,000 to $733,000 on March 4, 2026, and Warren Buffett netted roughly 18,854 Class B shares on May 18, 2026. Insiders are quietly accumulating while the crowd chases GPUs.

The Setup

Berkshire is off 5.74% over the past year and 4.52% year to date. That underperformance is the opportunity. While capital crowds into the most expensive name in the index, a conglomerate with monopoly-like cash engines is being marked down to book value.

The setup is straightforward: capital is crowding into the most expensive name in the index while a conglomerate with monopoly-like cash engines trades near book value. Investors weighing concentration risk against valuation discipline have a clear contrast to study.

Contact [email protected] for any questions or corrections.