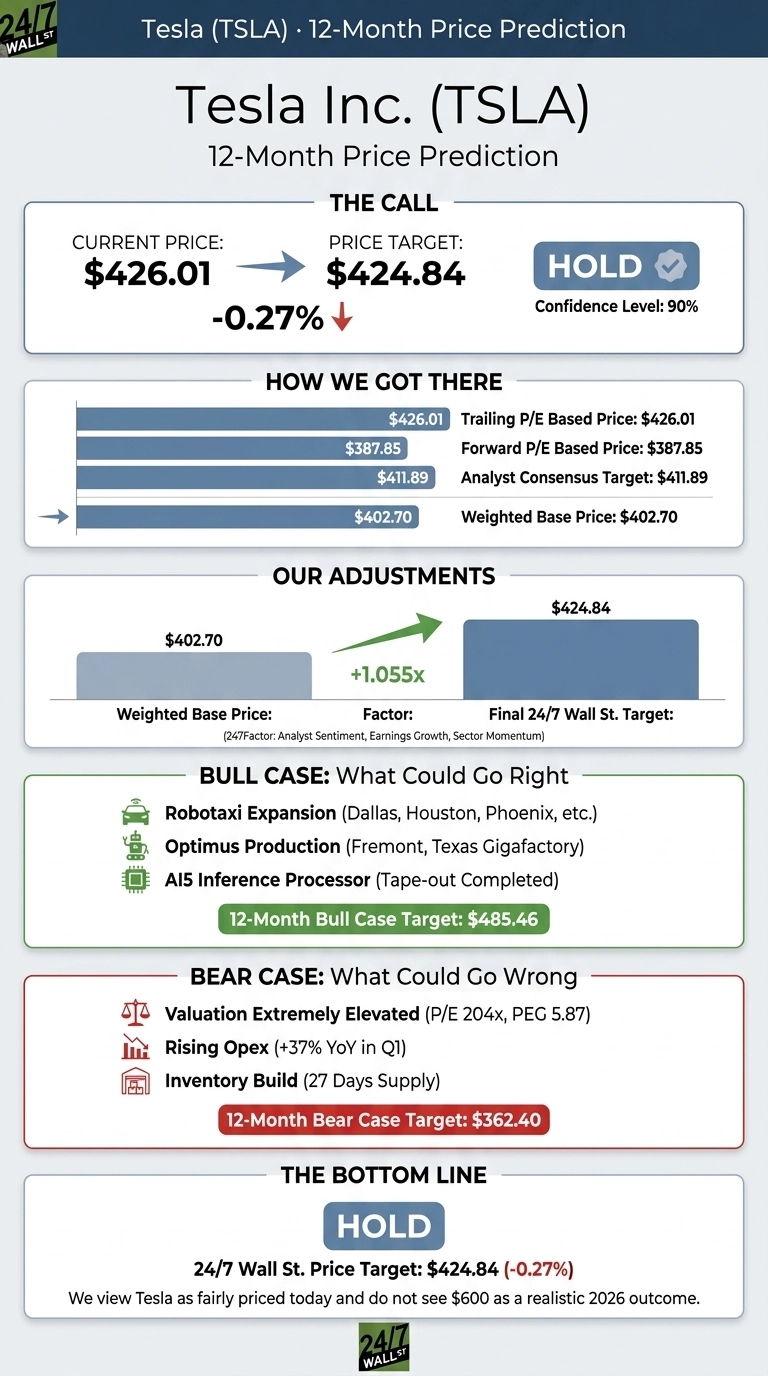

The question in this article’s title cuts to the heart of the Tesla (NASDAQ:TSLA | TSLA Price Prediction) debate. With shares having clawed back to $426.01 and momentum building off April lows, bulls are whispering about a run to $600. Our proprietary model has a different view.

Tesla sits roughly 17% below its 52-week high of $498.83, and reaching $600 in 2026 requires steep gains. Our 24/7 Wall St. price target for Tesla is $424.84, implying -0.27% from current levels. Our recommendation is hold with a 90% confidence reading. We view Tesla as fairly priced today and do not see $600 as a realistic 2026 outcome.

| Metric | Value |

|---|---|

| Current Price | $426.01 |

| 24/7 Wall St. Price Target | $424.84 |

| Upside/Downside | -0.27% |

| Recommendation | HOLD |

| Confidence Level | 90% |

Why We Could Be Wrong

Our price target sits a hair below where Tesla trades today, and Tesla is arguably the most divisive stock in the market. Real upside could come from faster-than-expected Robotaxi expansion across Dallas, Houston, Phoenix, Miami, and Las Vegas, or from Optimus production lines exceeding 1 million robots per year capacity at Fremont. Consider our target one datapoint among many.

From April Lows Back to $426

Tesla has rallied 9.94% over the past month off the April bottom near $391.95, though shares remain down 5.27% year to date. Q1 2026 results reset the narrative: revenue of $22.39 billion rose 15.78% YoY, non-GAAP EPS of $0.41 beat consensus of $0.3592, and automotive gross margin expanded to 21.1% from 16.2%. Active FSD subscriptions climbed 51% YoY to 1.28 million, and Services revenue jumped 42%. The post-earnings recovery has been real, but shares still trade at 421x trailing earnings.

The Case for $500+

Bulls have plenty to work with. Cybercab, Tesla Semi, and Megapack 3 are slated for volume production in 2026. Optimus lines at Fremont and Gigafactory Texas target 1 million and 10 million robots per year capacity, respectively.

The AI5 inference processor completed tape-out in April, and unsupervised Robotaxi rides are now live in Dallas and Houston. Our bull case scenario points to $485.46 over the next 12 months, with a peak of $492.28 in April 2027. That still falls short of $600 in 2026, but extending the bull trajectory five years gets us to $620.90 by 2031.

The Risks Worth Watching

The bear thesis centers on valuation. Tesla trades at a forward P/E of 204 and a PEG ratio of 5.87. FY2025 revenue declined 2.93% YoY, with full-year deliveries off 9%. Operating expenses grew 37% YoY in Q1 on AI R&D and CEO award stock-based comp. Energy revenue dropped 12%, and inventory expanded to 27 days from 22.

Polymarket assigns just 11% probability to a California Robotaxi launch by June 30 and 13.5% to an Optimus release by year-end. Our bear case lands at $362.40, a 14.93% drawdown. Bulls would argue elevated opex reflects investment in AI compute and the semiconductor fab partnership with SpaceX, both of which could become high-margin businesses later this decade.

Hold, Do Not Chase $600

Our 24/7 Wall St. price target of $424.84 says Tesla is fairly priced today. The answer to the title question is no. We would be buyers if Robotaxi monetization data shows real revenue per mile by Q3 or if Optimus hits volume production this year. We would stay sidelined if FSD adoption flattens or regulatory credit revenue keeps eroding. Rating: HOLD.

Here is where the model projects Tesla could trade, assuming current trajectories hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $424 |

| 2027 | $436 |

| 2028 | $450 |

| 2029 | $464 |

| 2030 | $478 |

These projections assume Tesla continues executing on FSD, Robotaxi, and Optimus without a major margin reset. Significant upside or downside could result from an Optimus production breakthrough, an xAI-style merger, or sustained decline in vehicle deliveries.

Contact [email protected] for any questions or corrections.