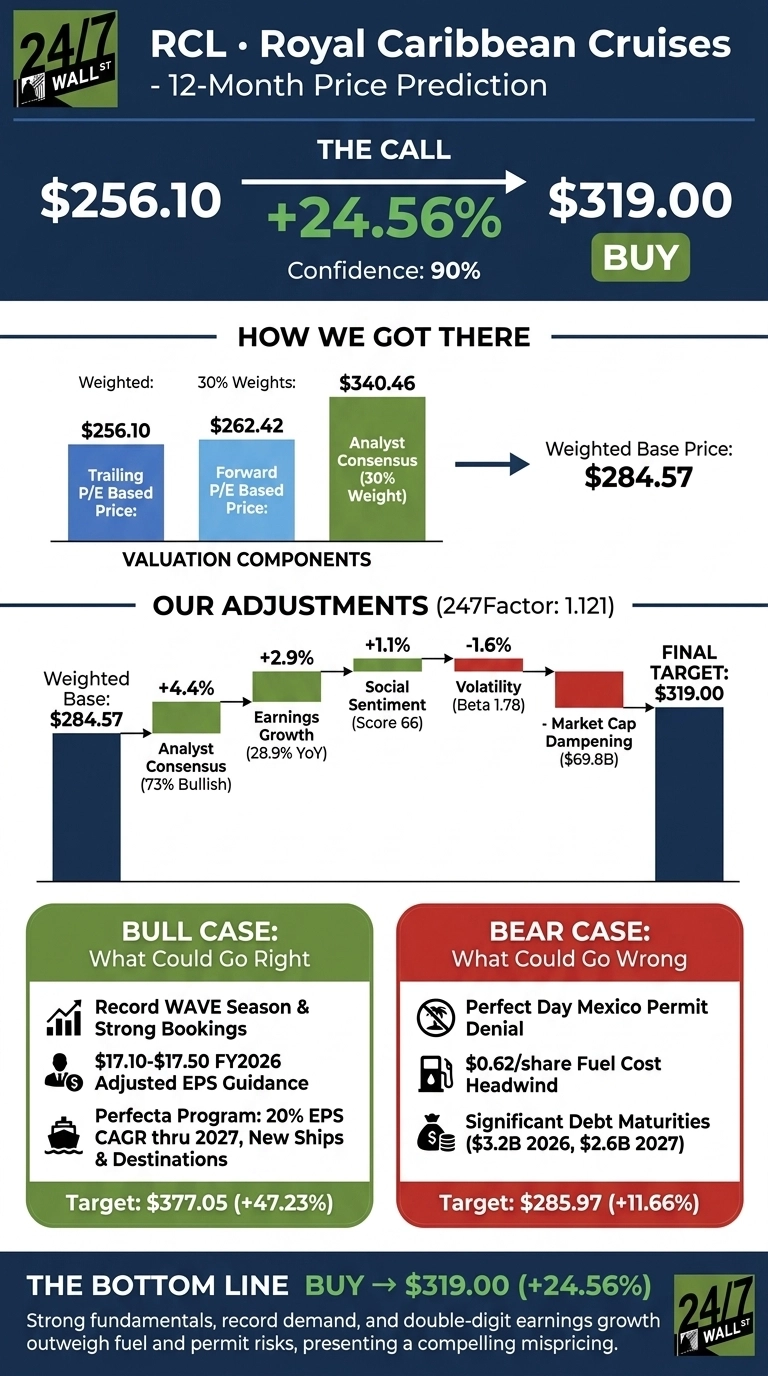

Our Royal Caribbean Cruises (NYSE:RCL | RCL Price Prediction) call sits firmly in the bull camp. Our 24/7 Wall St. price target for Royal Caribbean is $319, pointing to 24.56% upside from the recent close of $256.10. The model carries a 90% confidence score. The recommendation is buy.

| Metric | Value |

|---|---|

| Current Price | $256.10 |

| 24/7 Wall St. Price Target | $319.00 |

| Upside | 24.56% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Choppy Stock Hiding a Strong Operating Story

RCL has frustrated shareholders despite excellent fundamentals. The stock is down 7.69% year to date and 3.59% over the past month, hitting a 52-week low of $232.48 on May 20. The stock sits 6% below its 52-week high of $362.21. The five-year return is 216.4%.

Q1 2026, reported April 30, delivered adjusted EPS of $3.60 against $3.20 consensus, a 12.59% beat and fourth straight quarter topping estimates. Revenue grew 11.33% YoY to $4.452 billion, narrowly missing expectations.

Net income jumped 28.9% to $941 million, and adjusted EBITDA margin expanded 310 bps to 38.2%. The recent selloff tracked headlines around Mexico’s intent to deny the Perfect Day Mexico environmental permit and elevated fuel costs, while operating performance held firm.

The Case for $377+

Bulls have a clean story. CEO Jason Liberty told investors Q1 reflected a “record WAVE season” and guided FY2026 adjusted EPS to $17.10 to $17.50, implying double-digit earnings growth. The Perfecta Program targets 20% adjusted EPS CAGR through 2027, with management hitting the high-teens ROIC milestone early.

Growth drivers include Legend of the Seas delivery, Royal Beach Club Santorini launch, Icon VI and VII orders, Celebrity River Cruises entering service in 2027, and the new Royal ONE credit card. Royal Caribbean repurchased 2.9 million shares for $836 million in Q1 alone, with $1 billion remaining. The Street’s $340.46 consensus and our bull case scenario of $377.05 reflect that compounding setup.

The Risks Worth Watching

Mexico’s intent to deny the Perfect Day Mexico permit dings a key destination growth pillar, though Royal Caribbean is re-engaging with stakeholders. Fuel is a $0.62 per share headwind versus prior guidance, partly offset by 59% hedging.

Scheduled debt maturities of $3.2 billion in 2026 and $2.6 billion in 2027 arrive into an elevated rate backdrop. Geopolitical risk pressured Mediterranean bookings in March and April. The GF Value fair value sits at $244.48, suggesting modest overvaluation today. Q1 fundamentals show demand is intact: load factor was 109%, gross cruise costs per APCD fell 1%, and operating income grew 22.96%. Our bear scenario lands at $285.97, still above today’s price.

Royal Caribbean Price Prediction 2026-2030

The 24/7 Wall St. price target is $319, BUY, confidence 90%. An EPS run rate of $17.10 to $17.50 against a stock paying 15x forward earnings is a mispricing.

I’d be a buyer here if the broader consumer remains resilient and WAVE booking momentum carries into Q3. I’d stay on the sidelines if fuel spikes meaningfully and the Perfect Day Mexico denial cascades into broader destination strategy delays. The setup leans bullish.

Looking further out, here is where the model projects RCL could trade, assuming current growth trajectories and Perfecta Program execution hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $319 |

| 2027 | $370 |

| 2028 | $410 |

| 2029 | $450 |

| 2030 | $490 |

These projections assume Royal Caribbean executes capacity growth of 4% to 7% annually through 2029 and delivers on Perfecta targets. Significant upside or downside could come from fuel price swings, geopolitical shocks, or a broader consumer pullback.

Contact [email protected] for any questions or corrections.