Joby Aviation (NYSE:JOBY | JOBY Price Prediction) has been one of the most volatile names in the eVTOL space. After a punishing first half of 2026, the risk/reward calculus has shifted. The stock is down sharply, certification is inching closer, and Dubai operations are reportedly on track.

The 24/7 Wall St. Price Target for Joby Aviation

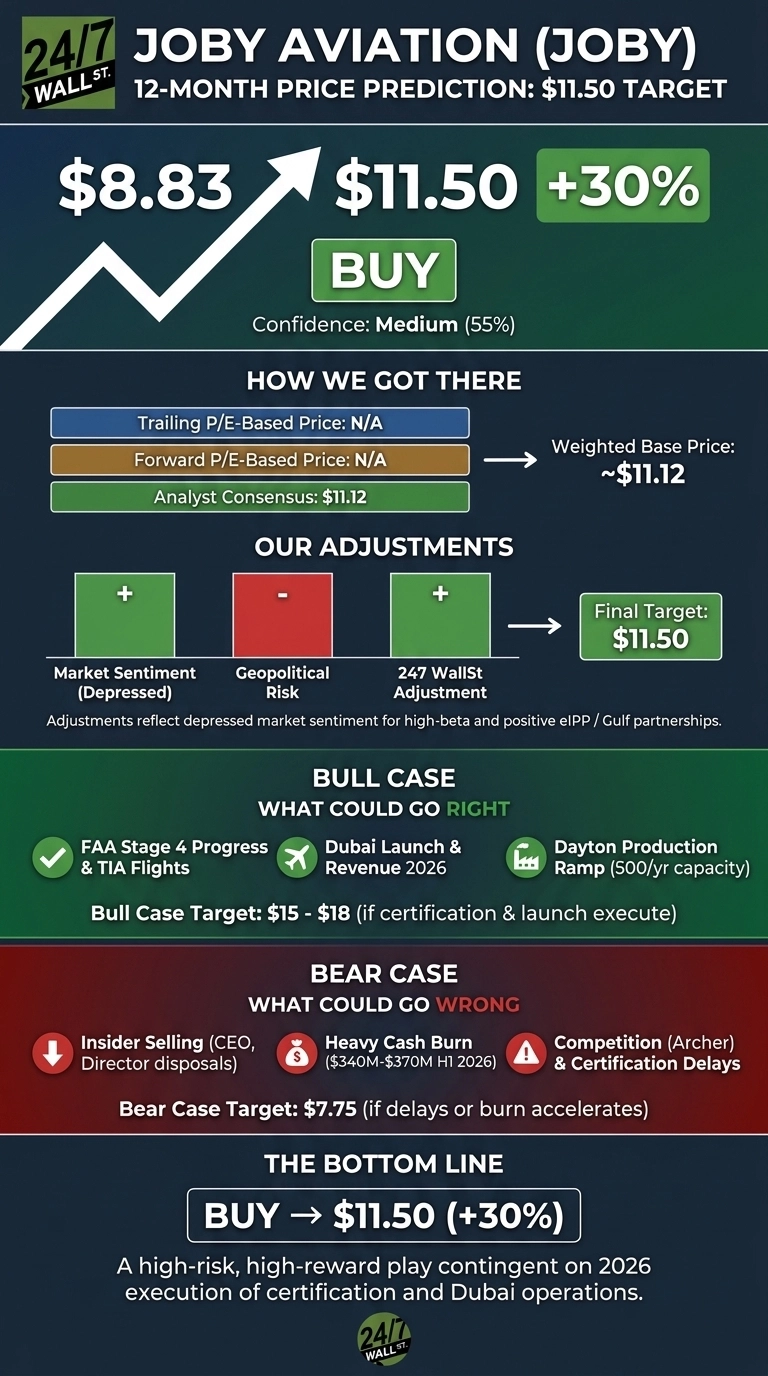

Joby Aviation trades at $8.83, down 33.11% year to date. Our 24/7 Wall St. price target for Joby is $11.50 over the next 12 months, implying roughly 30% upside, modestly above the Wall Street consensus target of $11.12. Recommendation: Hold with constructive bias. Confidence: medium, given the binary nature of FAA certification and cash burn risk.

| Metric | Value |

|---|---|

| Current Price | $8.83 |

| 24/7 Wall St. Price Target | $11.50 |

| Upside | 30% |

| Recommendation | HOLD |

| Confidence Level | 55% |

A Brutal Six Months, but a Real Earnings Beat

Joby has fallen 23.08% over the past month and 11.7% in the past week, pressured partly by Russell rebalance flows. The 52-week range is $7.75 to $20.95, with the 200-day moving average at $12.39.

Q4 2025 results were strong: revenue of $30.84 million exceeded the $16.88 million consensus, and EPS of -$0.14 beat the -$0.20 estimate. A $1.2 billion equity and convertible raise in February pushed cash to $1.41 billion, extending runway materially.

Why Bulls See a Breakout Ahead

The bull case is rich. CEO JoeBen Bevirt called 2026 “a key inflection point”, citing Dubai passenger service this year and the eIPP program. FAA Stage 4 certification advanced 18 points in Q4 alone. Joby logged 9,000+ flight miles in 2025 and has letters of intent worth over $1 billion across Saudi Arabia, Kazakhstan, and Japan.

The 700,000 sq ft Dayton, Ohio facility targets eventual capacity of 500 aircraft per year, supported by Toyota’s $500 million commitment. If FAA Type Certification arrives on time and Dubai launches cleanly, a bull scenario points to $15 to $18, near the 52-week high.

The Risks Worth Watching

The bear case starts with insider activity. CEO Bevirt sold 322,019 shares on June 15 at $10.38, part of a broader pattern of executive disposals. Director Paul Sciarra sold 500,000 shares at roughly $12. Much of this trades through Rule 10b5-1 plans, and Sciarra still holds 56.1 million shares, so framing every sale as conviction loss overstates the case.

H1 2026 cash usage is guided at $340 million to $370 million, gross margin sits at -30.1%, and Archer Aviation is a credible competitor. Bulls counter that the operating loss reflects $161.26 million in Q4 R&D spending ahead of certification. A bear scenario revisits the 52-week low near $7.75.

Hold for Now, but Watch Dubai

My 24/7 Wall St. price target is $11.50 with a hold rating and 55% confidence. I would be a buyer if Joby announces a concrete FAA TIA flight schedule or confirms paying passenger flights in Dubai before year end.

I would stay on the sidelines if cash burn exceeds guidance or certification slips into 2027. The setup is high risk, high reward. The 30% upside requires execution on certification and Dubai.

Assuming certification by 2027, the Dayton ramp toward 4 aircraft per month, and progressive margin expansion as Blade revenue scales:

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $11.50 |

| 2027 | $14.00 |

| 2028 | $17.50 |

| 2029 | $21.00 |

| 2030 | $25.00 |

Significant upside or downside could result from FAA timing, dilution from future raises, or Archer Aviation winning key contracts.

Contact [email protected] for any questions or corrections.