Carnival Corporation (NYSE:CCL | CCL Price Prediction) just delivered its twelfth consecutive quarter of record net yields, yet the stock sold off after Q2 results landed. That dislocation is the setup for our call.

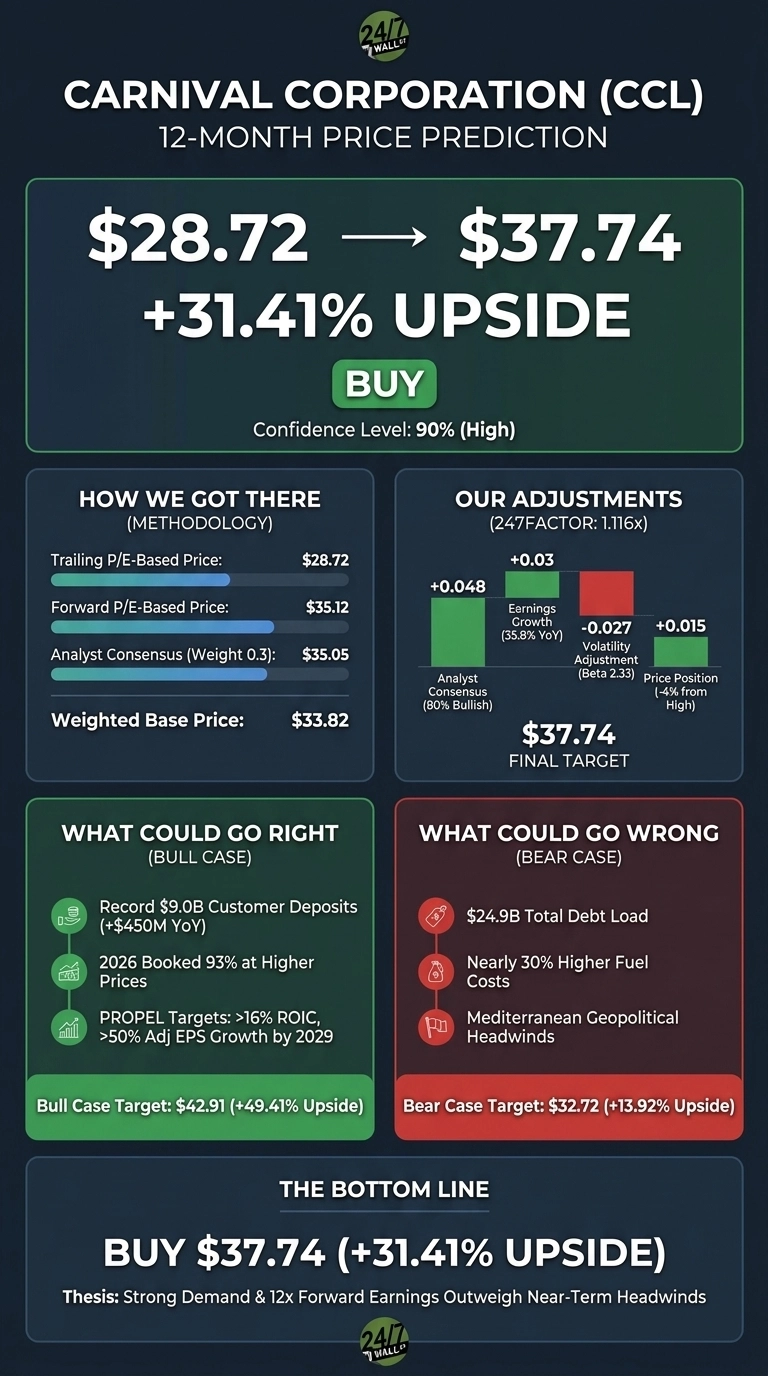

Our 24/7 Wall St. price target for Carnival is $37.74 over the next 12 months, implying 31.41% upside from a current price of $28.72. The recommendation is buy, with confidence at 90%, the high end of our framework.

| Metric | Value |

|---|---|

| Current Price | $28.72 |

| 24/7 Wall St. Price Target | $37.74 |

| Upside | 31.41% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Record Quarter, Punished by a Soft Guide

CCL is up 20.75% over the past year but down 4.95% year to date, and shares fell 4.87% on Q2 results. Carnival posted adjusted EPS of $0.41 against $0.35 a year ago and revenue of $6.663B, beating its own March guidance by $100M. Customer deposits hit a record $9B, and 2026 is 93% booked.

The sell-off traced to a Q3 outlook that came in below estimates on roughly 30% higher fuel prices and a $73M currency headwind. CEO Josh Weinstein told investors that “recent booking trends already suggest that we are beginning to see a reversal of these headwinds.”

Why Bulls See a Breakout Ahead

The bull case rests on demand that refuses to crack. Weinstein flagged that “booking volumes and prices” for 2027 sailings are running ahead of last year. The PROPEL plan targets >16% ROIC, >50% adjusted EPS growth from 2025 by 2029, and roughly $14B in shareholder distributions.

A $2.5B buyback is underway, and Fitch awarded investment grade. Bureau of Economic Analysis data shows recreation spending at a 16-month high of $864.2B. Freedom Broker carries a $35 target on a “rare” mix of record demand and disciplined supply. A bull case run takes shares to $42.91, a 49.41% return.

The Risks Worth Watching

Bears point to $24.9B in total debt, unhedged fuel exposure, and Mediterranean booking softness from Middle East tensions. Truist recently trimmed its price objective, and Q2 gross profit fell 29.81% YoY.

Bulls would counter that GAAP weakness reflects the fuel spike and FX, while adjusted net income still rose 20% and net debt to EBITDA improved to 3.4x. If macro softens, our bear case lands at $32.72, still 13.92% above today.

Carnival Price Prediction 2026 to 2030

Our 24/7 Wall St. price target of $37.74 reflects a buy rating at 90% confidence. The deciding factor is the $9B deposit book paired with 12x forward earnings. The thesis strengthens if fuel prices stabilize and 2027 booking momentum persists. It weakens if the Mediterranean disruption deepens and debt service crowds out buybacks.

Looking further out, here is where our model projects CCL could trade if base case growth holds.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $37.74 |

| 2027 | $44.11 |

| 2028 | $51.57 |

| 2029 | $60.27 |

| 2030 | $70.45 |

These projections assume Carnival continues hitting PROPEL targets. Material upside or downside could come from oil price shocks, recession risk, or accelerated deleveraging.

Contact [email protected] for any questions or corrections.