Costco (NASDAQ:COST | COST Price Prediction) just delivered another quarter that proves why this membership machine keeps compounding. Fiscal Q3 2026 revenue hit $70.53 billion, up 11.6% year over year, with comparable sales climbing 9.8% and e-commerce traffic surging 37%.

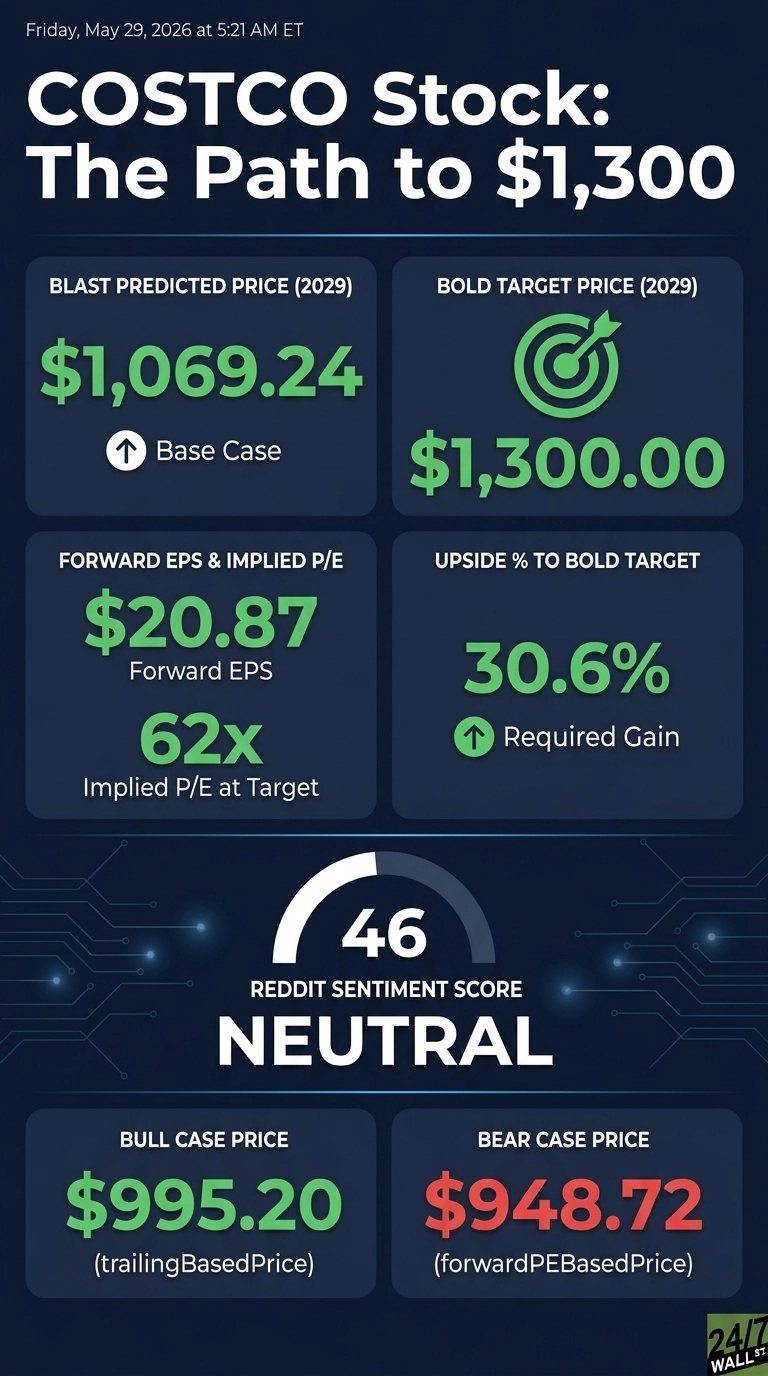

Shares trade at $995.20, up 15.73% year to date. The question I want to answer: can this stock reach $1,300 by 2029, or is the warehouse story already priced in?

Why Costco Shares Are Stuck Just Below the All-Time High

Despite the strong fundamentals, the stock has been frustrating lately. Shares are down 5.26% over the past week and basically flat over the last month at 0.27%. The one-year return is actually negative 1.22%.

The issue is the multiple. With a trailing P/E of 52, investors are paying a premium that leaves little room for error. The most recent earnings beat was just 0.17%, and the market shrugged. Add a University of Michigan consumer sentiment reading of 49.8, deep in recessionary territory, and you can see why a low-beta defensive name (beta 0.908) is treading water.

Wall Street Sees 8% Upside. I Think That’s Too Cautious

Wall Street’s consensus price target sits at $1,076.97, with 3 Strong Buys, 19 Buys, 12 Holds, and 2 Sells. Our model’s base case lands at $1,069.24, implying 7.44% upside with 90% confidence. The optimistic 1-year scenario stretches to $1,152.91, the bear case to $975.72.

Here is my pushback. With 45.5% YoY earnings growth and 61% of analysts bullish, the consensus underestimates how durable membership economics become once Costco crosses 940 warehouses. Analysts are anchoring to a one-year window. I am looking three years out.

The Path to $1,300 Per Share by 2029

Reaching $1,300 from today’s price of $995.20 would require a gain of 30.6%. With forward EPS of $20.87, a price of $1,300 implies a forward P/E of 62x. Our base case of $1,069.24 already implies 50x, meaning the bold target requires roughly 12x of additional multiple expansion (or, more realistically, the same multiple applied to materially higher 2029 earnings).

The case rests on three pillars. First, the 1.073 adjustment factor in our model is driven by 45.5% YoY earnings growth and 61% bullish analyst consensus.

Second, membership fee income grew 10.7% in Q3 with a worldwide renewal rate of 89.7%, locking in high-margin recurring revenue.

Third, Goldman Sachs flagged Costco specifically for capturing “a significant share of sales growth, benefiting from strong value offerings, operational leverage, and effective supplier negotiations” in retail. The main risk: a tariff-driven margin compression that breaks the Kirkland price-cut flywheel.

Current Valuation in Context

Costco’s current forward P/E sits at roughly 48x. That is rich, no question. But the stock has returned 690.43% over the past 10 years and 177.6% over five, so paying up for quality has worked. Shares sit just 2% below the 52-week high of $1,096.50, with the 52-week low at $841.69.

Premium multiple, premium business. The bull case requires Costco to keep compounding EPS at double-digit rates so 2029 earnings grow into the multiple rather than the multiple having to expand further.

Is $1,300 Realistic? My Verdict

Reaching $1,300 by 2029 requires a 30.6% gain from here, equivalent to about 9% annualized over three years. That is achievable but not easy.

Three things need to go right: membership renewal must hold above 89%, warehouse expansion to 940 locations must convert to comp-sales leverage, and e-commerce momentum (Q3’s 21.5% digital comp) must keep margins climbing.

A sustained consumer recession that pressures executive memberships would derail the thesis fastest. Returns at this level shouldn’t be expected every year, but we’ve outlined the blueprint for how Costco could reach $1,300 in 2029.

Contact [email protected] for any questions or corrections.