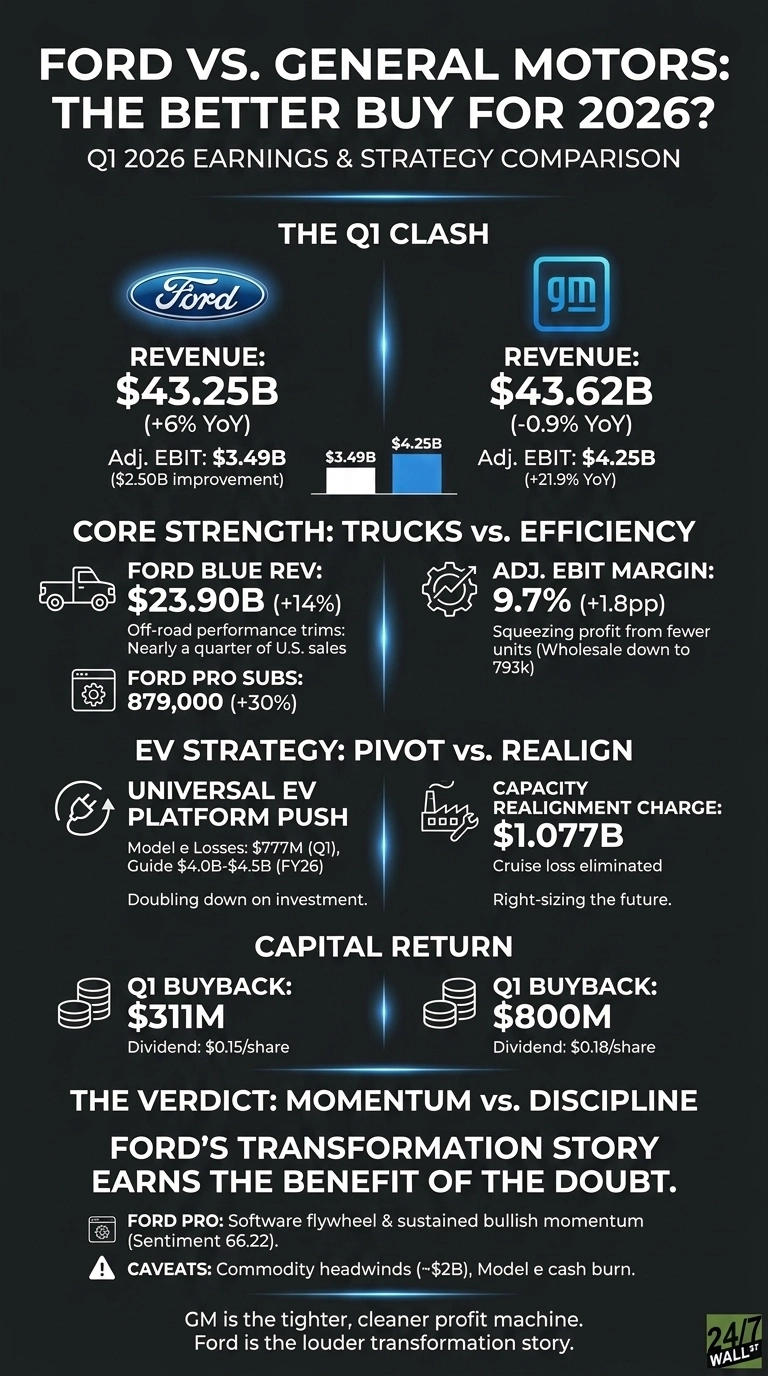

Ford (NYSE:F | F Price Prediction) and General Motors (NYSE:GM) closed Q1 2026 with a sharp contrast. GM topped estimates with a 41.31% EPS beat built on margin discipline. Ford answered with a $2.50 billion swing in adjusted EBIT and a louder transformation story. Both raised guidance. Only one is winning.

Trucks Carry Ford. Cost Discipline Carries GM.

Ford Blue delivered with $23.9 billion in revenue, up 14%, as F-Series, Bronco, Explorer, and Expedition demand stayed hot. Off-road performance trims now account for nearly a quarter of U.S. sales. Ford Pro added another layer: 879,000 paid software subscribers, up 30% year over year, at an 11.4% margin. That is recurring revenue most legacy automakers cannot match.

GM played differently. EBIT-adjusted jumped 21.9% to $4.25 billion, with margins expanding 1.8 percentage points to 9.7%, even as North American wholesale volumes slipped to 793,000 units and U.S. share fell to 16.5%. Mary Barra is squeezing more profit from fewer trucks. China helped, with equity income rising to $165 million from $45 million.

The EV Bet: Pivot vs. Purge

Ford is doubling down with a new Universal EV platform for affordable models, plus $1.5 billion earmarked for Ford Energy. Model e lost $777 million in the quarter, with full-year losses guided to $4 billion to $4.5 billion. That is substantial red ink to defend a platform bet.

GM went the other direction, booking a $1.077 billion EV capacity realignment charge and winding down Cruise, whose loss is now eliminated.

| Lens | Ford | GM |

| Core Bet | Ford+ software, UEV platform | Margin discipline, buybacks |

| EV Posture | Doubling investment | Right-sizing capacity |

| Capital Return | $311M buyback, $0.15 dividend | $800M buyback, $0.18 dividend |

| Key Vulnerability | $2B aluminum-led commodity hit | U.S. share erosion to 16.5% |

Both leaned on the U.S. Supreme Court IEEPA tariff ruling. Ford booked a $1.3 billion one-time benefit; GM trimmed its gross tariff cost range to $2.5 billion to $3.5 billion.

What I’m Watching Into the Back Half

For Ford, the test is whether the Universal EV platform can shrink Model e losses while Ford Pro compounds software subs. Jim Farley framed it bluntly: “We are well-prepared to deliver for our customers and shareholders as we enter one of the most intensive product, software and physical services rollouts in our history.”

Aluminum costs and the $400 million European restructuring drag will tell us if the cost side cooperates. BofA raised the firm’s price target on Ford to $20 from $17 and keeps a Buy rating on the shares.

For GM, the watch item is share. Fleet sales jumped to 20.6% of total from 16.5%, which props volume but pressures retail mix. China is recovering, yet vehicle sales there fell to 349,000 from 443,000.

Why Ford Looks More Compelling Right Now, With Caveats

For investors focused on the cleaner profit machine and steady buyback cadence, GM fits that profile. Barra’s team runs a tighter shop, and the one-year return rewards that discipline.

But Ford looks more compelling heading into 2026. Ford Pro’s software flywheel is the most underappreciated part of either story, and the post-earnings move and bullish composite sentiment of 66.22 tell me momentum is real.

Analyst consensus implies -17.42% downside on Ford, and Model e still burns cash. If aluminum keeps climbing or the UEV ramp slips, the case for GM strengthens. For now, the transformation story has earned the benefit of the doubt.

Contact [email protected] for any questions or corrections.