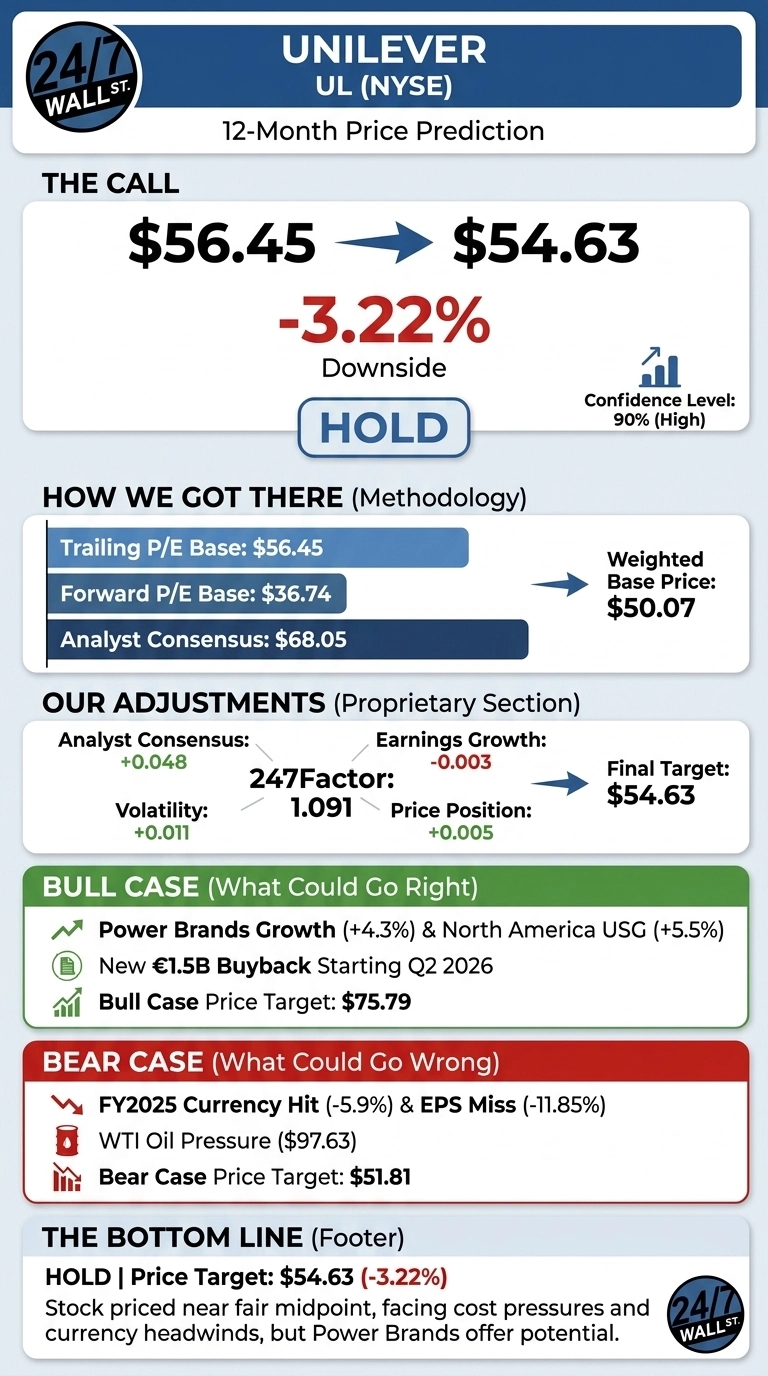

Our Unilever (NYSE:UL | UL Price Prediction) call lands on the cautious side of fair value. After a brutal stretch that has erased 18.4% over the past year and 12.19% year to date, the stock is oversold, but our proprietary model sees a small step backward over the next 12 months.

The 24/7 Wall St. Price Target for Unilever

Our 24/7 Wall St. price target for Unilever is $54.63, modestly below the current $56.45 quote. The implied move is -3.22%, and we rate UL a hold with high (90%) confidence. With a forward P/E of 16 and a defensive beta of 0.452, this stock is priced near its fair midpoint.

| Metric | Value |

|---|---|

| Current Price | $56.45 |

| 24/7 Wall St. Price Target | $54.63 |

| Upside/Downside | -3.22% |

| Recommendation | HOLD |

| Confidence Level | 90% |

Why We Could Be Wrong

Our $54.63 target sits just under current levels. UL is deeply oversold, and real upside could come from a margin beat tied to the new €1.5 billion buyback starting Q2 2026 or faster traction from premium acquisitions like Dr. Squatch and Liquid I.V. Our bull case below outlines why UL could outperform.

A Brutal Slide From February Highs

UL peaked near $73.96 in mid-February 2026 before unwinding to the mid-$50s. The weekly RSI sits at 37.95, with the stock spending 8 of the last 12 weeks in oversold territory.

FY2025 underlying operating margin came in at 20% (+60bps), but reported EPS of $2.59 missed the $2.9383 consensus by 11.85%. WTI crude sits at $97.63, in the 85th percentile of its 12-month range, pressuring input costs heading into 2026 guidance set at the bottom end of the 4% to 6% underlying sales growth band.

How We Calculated $54.63

The 24/7 Wall St. Price Target blends trailing P/E, forward P/E, and analyst consensus, then applies our 247Factor adjustment for sector momentum, growth, volatility, and sentiment. The trailing P/E approach implied $56.45, while forward P/E pointed to $36.74 on a $2.35 forward EPS estimate. The blended pre-adjustment price landed at $50.07.

We applied a 247Factor of 1.091, lifted by an 80% bullish analyst consensus and low beta, but dampened by negative earnings growth of -3.4% YoY and a 30% large-cap dampener, producing our $54.63 target.

The Case for $75 and Higher

Bulls argue UL is mispriced after the Ice Cream demerger left a cleaner, higher-margin business. Power Brands now contribute 78% of turnover and grew 4.3%. North America posted 5.5% USG with 5.4% volume in Q3, and Indonesia returned to 12.7% growth.

The Wall Street consensus target is $68.05 with 1 Strong Buy, 3 Buy, 1 Hold. Our bull-case scenario projects UL at $75.79 by June 2027 if premium beauty acquisitions accelerate and oil retreats below $80.

The Risks Worth Watching

The bear case starts with currency. FY2025 reported turnover took a 5.9% currency hit, Latin America remains weak, and China demand is soft.

EPS missed by nearly 12%, which bulls counter reflects one-time costs from the Ice Cream separation and stranded overhead that should normalize through 2026. Our bear scenario sees UL at $51.81 by mid-2027 if volume growth slips below the company’s 2% floor and WTI stays above $100.

Hold for Now, With a Buyer’s Eye

I rate Unilever a hold with high confidence. The $54.63 target says the easy money has been made on the way down, but premium recovery requires execution proof. The setup turns more constructive on a confirmed Q1 2026 revenue beat versus the $12.45 billion consensus paired with stable volume.

The thesis weakens if oil holds above $100 and the buyback fails to support the share count. The 4.04% dividend yield pays you to wait.

Unilever Price Prediction 2026-2030

Here is where our model projects UL could trade, assuming current growth trajectories and margin recovery hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $55.06 |

| 2027 | $55.02 |

| 2028 | $55.20 |

| 2029 | $56.23 |

| 2030 | $58.56 |

These projections assume Unilever executes on its Power Brand strategy and US/India focus. Significant upside or downside could result from oil normalization, accelerated premium beauty M&A, or a sharper-than-expected slowdown in emerging market demand.

Contact [email protected] for any questions or corrections.