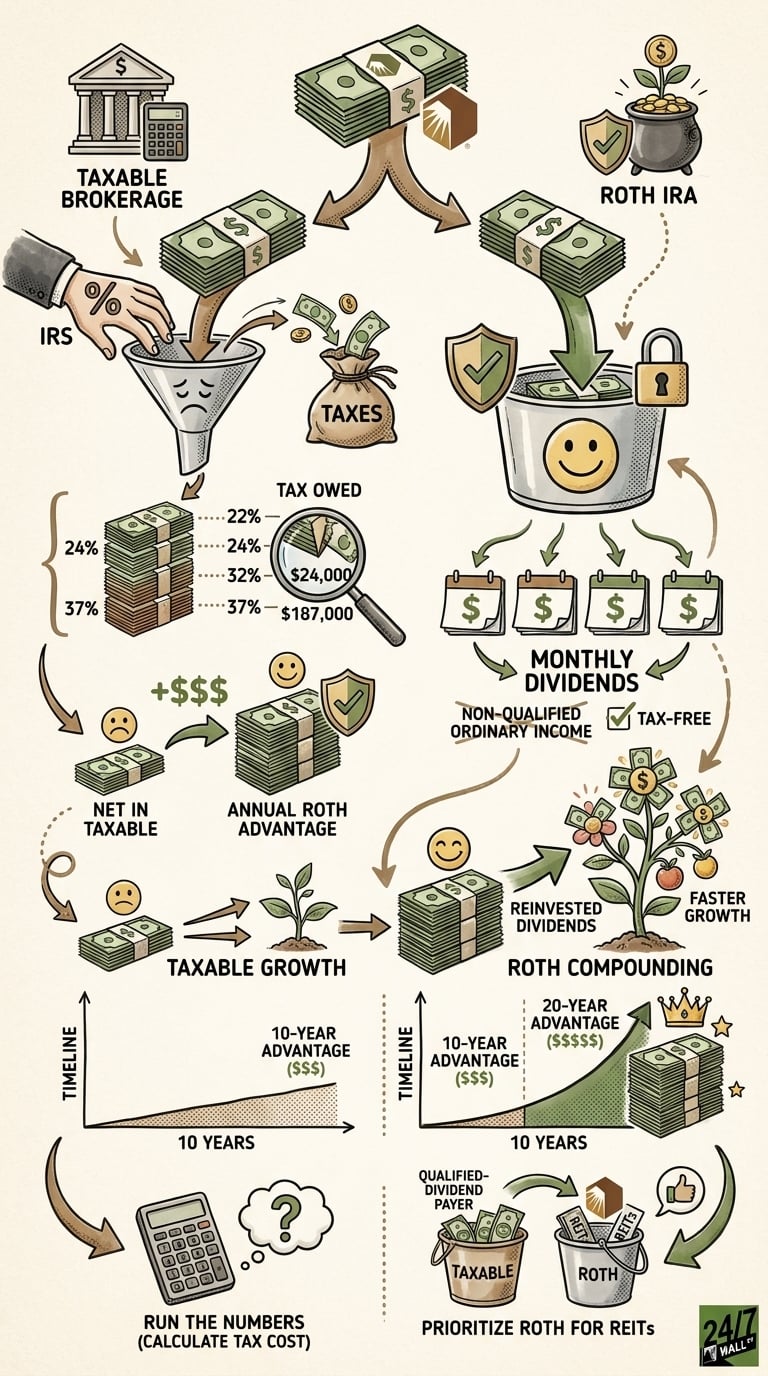

At the 24% federal bracket, a $250,000 position in Realty Income (NYSE: O | O Price Prediction) throws off roughly $13,150 a year at the current 5.3% yield. Held in a taxable brokerage, about $3,156 of that goes straight to the IRS every year. Held in a Roth, zero does. That is the entire premise of this article.

Why Realty Income Is a Textbook Roth Holding

Real estate investment trust (REIT) distributions are non-qualified ordinary income. They are taxed at your marginal bracket, full stop, with no access to the 15% or 20% qualified-dividend rate. Realty Income has now declared 671 consecutive monthly dividends and posted its 114th consecutive quarterly increase, with a monthly payout of $0.2705 and an annualized rate of $3.246. That is a high-frequency, fully taxable income stream. The Roth wrapper is the difference between keeping all of it and giving a chunk back every April.

The Tax Delta: Roth Versus Taxable at the 24% Bracket

Using the current yield of 5.3% and the 24% bracket (single filers with income over $105,700, married filing jointly over $211,400 for 2026):

| Position Size | Gross Annual Dividend | Net in Taxable (24%) | Net in Roth | Annual Roth Advantage |

|---|---|---|---|---|

| $50,000 | $2,630 | $1,999 | $2,630 | $631 |

| $100,000 | $5,260 | $3,998 | $5,260 | $1,262 |

| $250,000 | $13,150 | $9,994 | $13,150 | $3,156 |

On the $250K tier, that represents a $31,560 cumulative 10-year advantage before any compounding, based solely on account placement.

The Bracket Multiplier

The same $100,000 Realty Income position, generating $5,260 in gross dividends, produces dramatically different after-tax outcomes depending on bracket.

| Bracket | Tax Owed (Taxable) | Net in Taxable | Roth Advantage |

|---|---|---|---|

| 22% | $1,157 | $4,103 | $1,157 |

| 24% | $1,262 | $3,998 | $1,262 |

| 32% | $1,683 | $3,577 | $1,683 |

| 37% | $1,946 | $3,314 | $1,946 |

A 37% bracket investor loses nearly twice as much per year on the same shares as a 22% bracket investor. The higher the bracket, the more urgent the Roth placement.

The Insight Most Readers Miss

The Roth advantage compounds: that delta reinvested into more Realty Income shares generates more monthly dividends, all tax-free. On a $250,000 position at the 24% bracket, the $3,156 annual delta reinvested monthly at the current 5.27% yield approaches roughly $41,000 over 10 years and north of $110,000 over 20 years before any share-price appreciation. That is the permanent, realized cost of holding Realty Income outside a Roth. Monthly compounding matters here. Realty Income pays 12 times per year versus four for most blue-chip dividend payers, so reinvested distributions begin earning their own dividends a quarter sooner.

What to Do

- If Realty Income or any other REIT sits in your taxable account, calculate the annual tax cost at your marginal bracket before your next filing. With Q1 2026 AFFO of $1.13 per share and full-year guidance of $4.41 to $4.44, the income stream is durable enough to justify running the numbers.

- Run the Roth conversion math on Realty Income shares held in a traditional IRA. Compare the one-time conversion tax against the lifetime stream of $0.2705 monthly distributions sheltered permanently.

- For investors still contributing, the math favors placing Realty Income inside the Roth bucket while qualified-dividend payers can sit in the taxable account, where the 15% to 20% rate already applies.