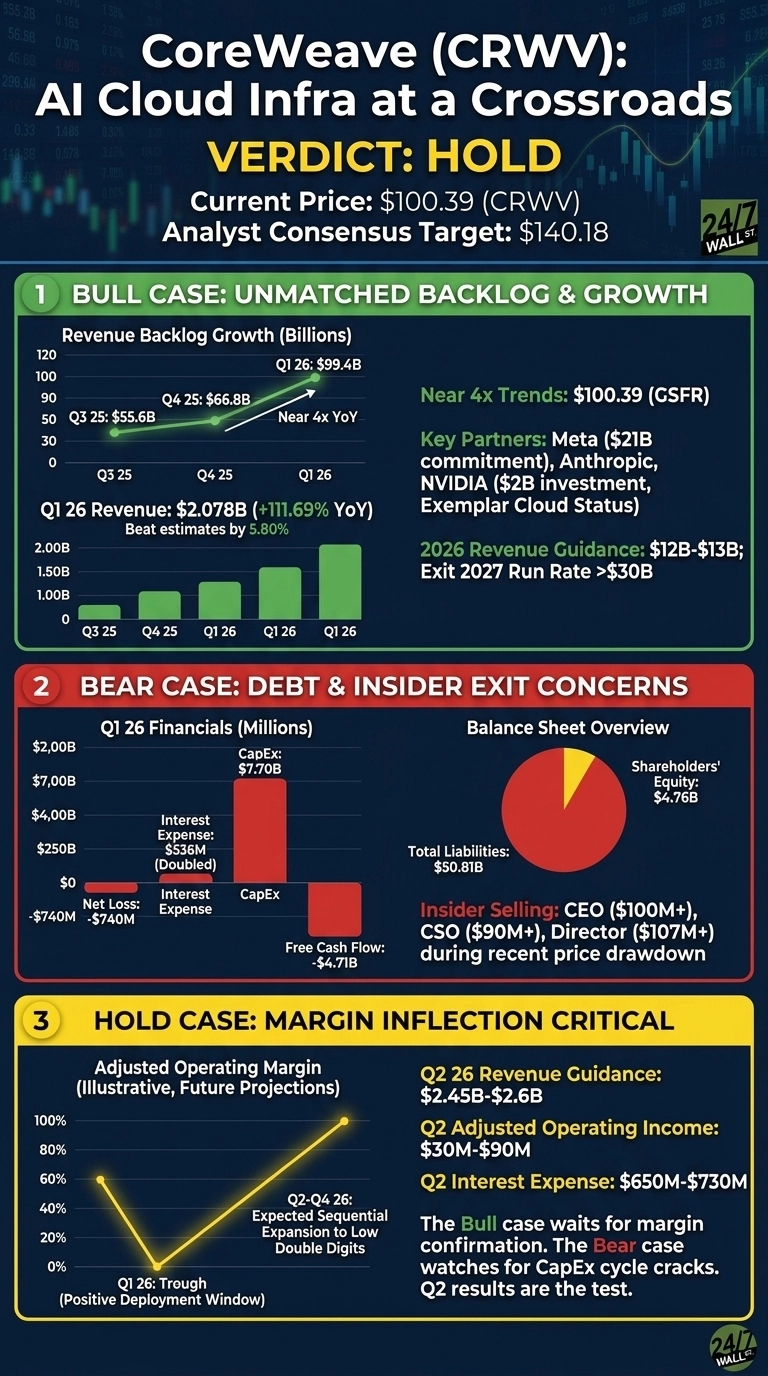

At $100.39, CoreWeave (NASDAQ:CRWV) is a hold. The stock has shed 27.24% in a month while investors debate a core question: can the company convert a $99.4 billion backlog into cash before the debt math turns ugly.

CoreWeave operates a specialized GPU cloud for AI training and inference, positioned between hyperscalers like Microsoft and Meta and NVIDIA silicon.

Its $2.078 billion Q1 revenue, up 111.69% year over year, beat estimates by 5.80%, yet the stock has slid from $136.80 at the filing to triple digits as investors weigh the capital intensity behind that growth.

The Backlog Tells a Generational Story

Revenue backlog reached $99.4 billion, near 4x year over year, after Q1 bookings of more than $40 billion including a $21 billion Meta commitment and a multi-year Anthropic deal. CEO Mike Intrator says “the world’s four preeminent AI model developers now rely on CoreWeave Cloud as do nine of the ten AI leaders outside of China.”

Management reaffirmed $12 billion to $13 billion of 2026 revenue and raised the low end of exit-2026 annualized run rate to $18 billion to $19 billion, with a path to more than $30 billion exiting 2027. NVIDIA’s $2 billion equity check and Exemplar Cloud status validate the moat. With shares 25.66% off year-ago levels, the entry looks cheap against a five-year contracted revenue profile.

The Debt and Insider Exit Are Real

Q1 net loss widened to $740 million from $315 million, interest expense doubled to $536 million, and total liabilities sit at $50.81 billion against $4.76 billion of equity. Free cash flow ran negative $4.71 billion as CapEx ballooned to $7.7 billion in a single quarter.

Insiders have been selling. CEO Intrator sold roughly $100 million across May and June, CSO Brian Venturo offloaded near $90 million, and Director Jack Cogen disposed of about $107 million. That is a striking signal during a 27.24% drawdown, and Morningstar warns the stock trades “just above its fair value estimate.”

Margin Inflection Is the Whole Ballgame

CFO Nitin Agrawal told analysts “Q1 was the trough of our margin story” with sequential expansion expected as deployments cross the three-month fit-out window. Adjusted operating margin should return to low double digits by Q4. That is the bull case in waiting and the bear’s trap door if Q2 or Q3 disappoints.

Q2 guidance of $2.45 billion to $2.6 billion in revenue with adjusted operating income of just $30 million to $90 million against $650 million to $730 million of interest expense leaves no room for slippage. The next two earnings reports will reveal whether contribution margins normalize as promised.

What the Street Says

CoreWeave trades at $100.39 against an analyst consensus target of $140.18, implying 39.64% upside. Coverage is wide: 3 Strong Buy, 19 Buy, 11 Hold, 1 Sell, and 1 Strong Sell.

Year to date, CRWV is up 40.19% versus the S&P 500’s 8.16%, yet shares trade below the $105.98 50-day moving average and at 8.8x sales with a $54.77 billion market cap and negative trailing EPS of -$2.72.

Why Waiting Beats Acting Here

At $100, CoreWeave’s risk/reward looks balanced.

The Buy case requires faith that margin expansion arrives on schedule. The Sell case requires belief that the AI capex cycle cracks before backlog converts. Both hinge on data still ahead.

Q2 results, due in roughly two months, will deliver the first real test of “sequential expansion through the balance of the year.” A clean beat with operating income at the high end of $30 million to $90 million, plus evidence that contribution margins normalize toward mid-20s, flips this to a Buy with conviction.

A miss, especially one driven by deployment delays referenced in the pending securities fraud action, opens a path back toward the $63.80 52-week low as the market reprices the gap between $50.81 billion of liabilities and a still-unprofitable P&L. The cost of waiting is roughly 39.64% of theoretical upside; the cost of acting early is owning a leveraged AI build-out through a guidance reset.

With a backlog this large, debt this heavy, and insiders this active on the sell side, let the next earnings report settle the argument.

Contact [email protected] for any questions or corrections.