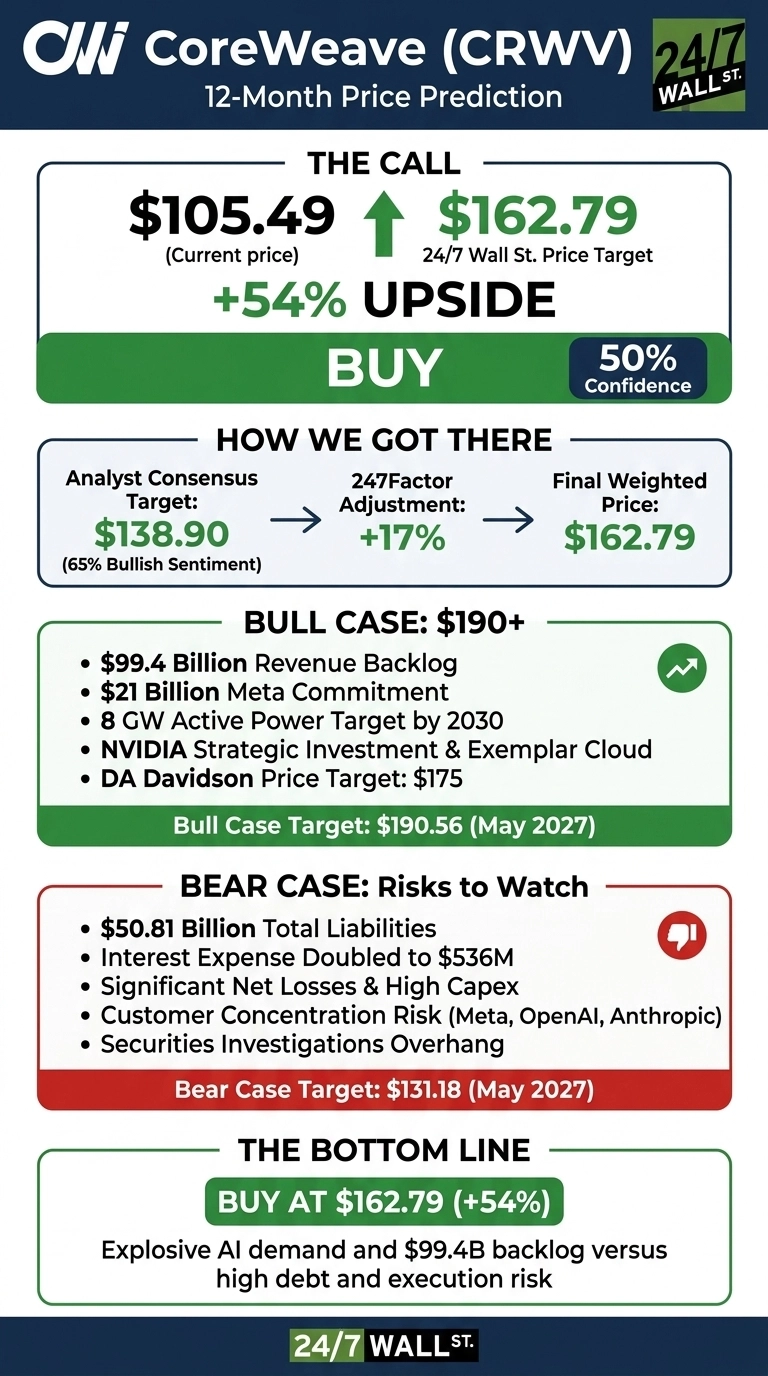

Our CoreWeave (NASDAQ:CRWV) call is built on the collision between explosive AI infrastructure demand and a balance sheet straining under capex. The 24/7 Wall St. price target points to $162.79 over the next 12 months, implying meaningful upside from $105.49.

Our recommendation is buy with a moderate 50% confidence level, reflecting the wide outcome range between hypergrowth execution and debt-funded margin pressure.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $105.49 |

| 24/7 Wall St. Price Target | $162.79 |

| Upside | 54.32% |

| Recommendation | BUY |

| Confidence Level | 50% |

A Whiplash Year for CoreWeave Shareholders

CoreWeave has been one of the wildest stock stories of 2026. Shares are up 47.31% year to date, yet down 13.91% over the past month after touching a 52-week high of $187. The stock sits 26% below that peak and well above the $63.80 52-week low.

The Q1 2026 report on May 7 framed the debate. Revenue surged to $2.08 billion, up 111.7% YoY and beating estimates by 5.80%, while EPS came in at -$1.40, missing expectations. The standout figure: revenue backlog of $99.4 billion, including a $21 billion Meta commitment signed in March.

The Case for $190+

Bulls have plenty to work with. The $99.4 billion backlog provides visibility years out, and over 75% of 2027 capacity is already sold. CEO Michael Intrator told investors, “This was the strongest bookings quarter in CoreWeave’s history… We surpassed 1 GW of active power and believe we are well on our way to more than 8 GW by 2030.”

NVIDIA closed a $2 billion Class A investment and named CoreWeave its Exemplar Cloud for inference on GB200 NVL72. DA Davidson carries a $175 price target, and our bull case scenario points to $190.56 over the next year if inference demand accelerates and capex translates cleanly to revenue.

What Could Go Wrong

The bear case starts with the balance sheet. Total liabilities hit $50.81 billion, interest expense doubled YoY to $536 million, and Q1 capex of $7.70 billion drove free cash flow to -$4.71 billion. Bulls counter that operating cash flow swung to a positive $2.98 billion, and the heavy spend is contracted revenue conversion rather than speculative buildout.

Customer concentration remains real, with Meta, OpenAI, and Anthropic anchoring the backlog. Securities investigations tied to prior data center capacity disclosures add overhang. Our bear case lands at $131.18, still above today’s price but a far cry from the bull path.

CoreWeave Price Prediction 2026-2030

The 24/7 Wall St. price target of $162.79 reflects a buy with 50% confidence. The tipping factor is the backlog. A $99.4 billion contracted pipeline against a $57.55 billion market cap is hard to ignore.

The bull thesis holds if power capacity additions stay on schedule and gross margins remain steady through the inference transition. The thesis weakens if interest expense outpaces revenue conversion or customer concentration risk materializes.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $162 |

| 2027 | $205 |

| 2028 | $250 |

| 2029 | $298 |

| 2030 | $346 |

These projections assume CoreWeave executes on its 8 GW by 2030 power target and continues converting backlog to revenue at current pace. Significant upside or downside could result from a faster inference transition, deeper NVIDIA integration, or a credit-market shock that disrupts the capex-funded growth model.

Contact [email protected] for any questions or corrections.