CoreWeave (NASDAQ:CRWV) has whipsawed investors with triple-digit revenue growth, a $99 billion backlog, and one of the heaviest capex profiles in the cloud sector. After a 14.58% pullback over the past month, the question is whether the AI hyperscaler discount has gone too far.

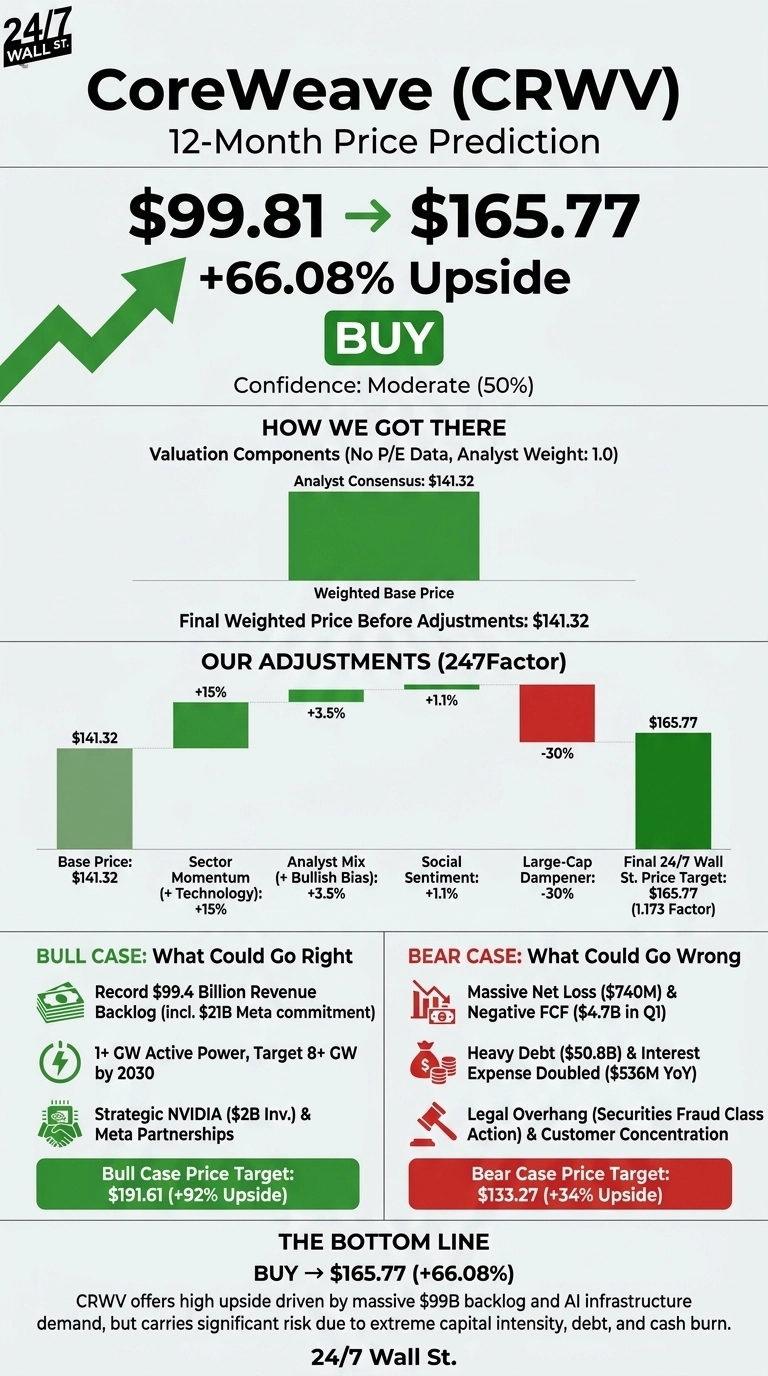

Our 24/7 Wall St. price target for CoreWeave is $165.77, implying 66.08% upside from $99.81. The model output flags a buy signal at moderate confidence given the volatility and balance-sheet risk in the story.

| Metric | Value |

|---|---|

| Current Price | $99.81 |

| 24/7 Wall St. Price Target | $165.77 |

| Upside | 66.08% |

| Recommendation | BUY |

| Confidence | 50% (moderate) |

From $187 High to Backlog at $100 Billion

CRWV trades 24% below its $187 52-week high and well off the $63.80 low. Shares are down 7.37% over the past week, yet still up 39.38% year to date.

The Q1 2026 report on May 7, 2026 was a study in contrasts. Revenue of $2.08 billion beat estimates and grew 111.69% year over year, while EPS of -$1.40 missed the -$1.2042 consensus. Revenue backlog jumped to $99.4 billion, including a fresh $21 billion Meta (NASDAQ:META | META Price Prediction) commitment. CEO Michael Intrator called it “the strongest bookings quarter in CoreWeave’s history.”

The Case for $190+

Bulls anchor on backlog conversion. CoreWeave grew active power past 1 GW in Q1 with contracted power above 3.5 GW and a target of 8 GW by 2030. NVIDIA (NASDAQ:NVDA) closed a $2 billion Class A investment, and an $8.5 billion investment-grade term loan facility shores up funding. Intrator argues CoreWeave “sits between the models and the silicon” as workloads pivot from training to inference.

The bull case maps to our $191.61 upside scenario, a 91.97% 12-month return. Analyst consensus sits at $141.32, with 22 Buy-equivalent ratings.

What Could Go Wrong

Free cash flow ran -$4.71 billion in Q1 against $7.7 billion in capex. Total liabilities of $50.81 billion nearly match the $55.57 billion asset base, and interest expense doubled YoY to $536 million. A securities fraud class action tied to alleged data center construction delays adds legal overhang.

Counterpoint: operating cash flow surged to $2.98 billion, and bulls would argue the negative FCF reflects pre-funded capacity tied to signed contracts rather than speculative build. Still, the bear scenario implies a 12-month price near $133.27 if growth decelerates.

CoreWeave Price Prediction 2026-2030

The 24/7 Wall St. price target of $165.77 reflects a buy at moderate confidence. The key tip is the $99.4 billion backlog, which provides visibility few growth names can match. The thesis strengthens if capex begins translating to operating leverage by late 2026. It weakens if interest expense keeps doubling without margin progress.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $165.77 |

| 2027 | $237.40 |

| 2028 | $299.21 |

| 2029 | $349.60 |

| 2030 | $397.97 |

These projections assume CoreWeave executes on its 8 GW power roadmap and converts backlog on schedule. Significant upside or downside could come from a shift in NVIDIA allocation, hyperscaler insourcing, or refinancing terms on the debt stack.

Contact [email protected] for any questions or corrections.