Marvell Technology (NASDAQ:MRVL | MRVL Price Prediction) is the name on every chip trader’s lips after a 305.44% one-year rip that turned custom AI silicon into the most crowded trade in semiconductors. But here’s what you should actually be watching.

The Marvell trade is mathematically exhausted

Last Friday’s leverage shakeout told you everything. Marvell dropped 16.74% in a single session on June 5, and by June 7, Reddit’s wallstreetbets crowd had pivoted from “23k MRVL YOLO” posts to a high-engagement thread celebrating a 100k+ gain shorting Marvell. Sentiment scores collapsed from 88 to 8 in under a week. That is the signature of a positioning unwind.

The fundamentals don’t justify catching it. Marvell trades at a trailing P/E of 91 and a forward P/E of 65, with a price-to-sales ratio of 26. Q1 FY2027 revenue of $2.418 billion beat consensus by a razor-thin 0.41%, and GAAP net income cratered to $34.5 million, down 80.61% year over year. Stock-based comp ballooned to $207.6 million, the company took a $331.8 million contingent consideration charge, and management issued $2 billion in Series A Convertible Preferred Stock on March 31. 76% of revenue comes from data center customers who are actively building their own in-house silicon to replace Marvell.

This is a single-customer-relationship business priced like a monopoly.

The redirect: the foundry looks more attractive than the designer

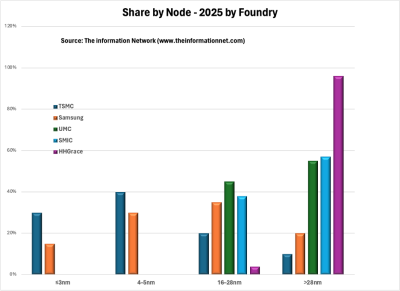

Taiwan Semiconductor Manufacturing (NYSE:TSM) actually fabricates the advanced-node chips Marvell designs. It sold off 6.69% on June 5, and that is the opportunity. Three reasons it stands out.

One: the math is the opposite of Marvell’s. TSMC’s Q2 2026 wafer manufacturing revenue hit $968.1 billion NT, up from roughly $714 billion NT a year earlier. Net income grew 43.82% on 21.45% revenue growth, the signature of operating leverage. Profit margin sits at 46.5%, operating margin at 58.1%, and return on equity at 36.2%. The forward P/E is 27, less than half of Marvell’s.

Two: the moat is physical. No competitor can match TSMC’s advanced-node capacity. Analysts project roughly 28% compound annual EPS growth over the next several years, and the company has 19 covering analysts with a $467.84 consensus target. If hyperscalers insource their custom silicon, they still need TSMC to print the wafers.

Three: the “Taiwan risk” discount is closing. The U.S. investment tax credit on TSMC Arizona was raised from 25% to 35% effective January 1, 2026, and the company is collecting government subsidies from the United States, Germany, Japan, and China for overseas fabs. Geographic diversification is no longer a slideshow promise.

Retail enthusiasm on TSM already peaked and cooled, with Reddit sentiment scores falling from 80-83 in late May to 58-64 by June 4. That is exactly the quiet window value buyers want.

What to watch next

The June 5 pullback offers a notably cheaper entry on TSM while the Marvell positioning continues to unwind.

Contact [email protected] for any questions or corrections.