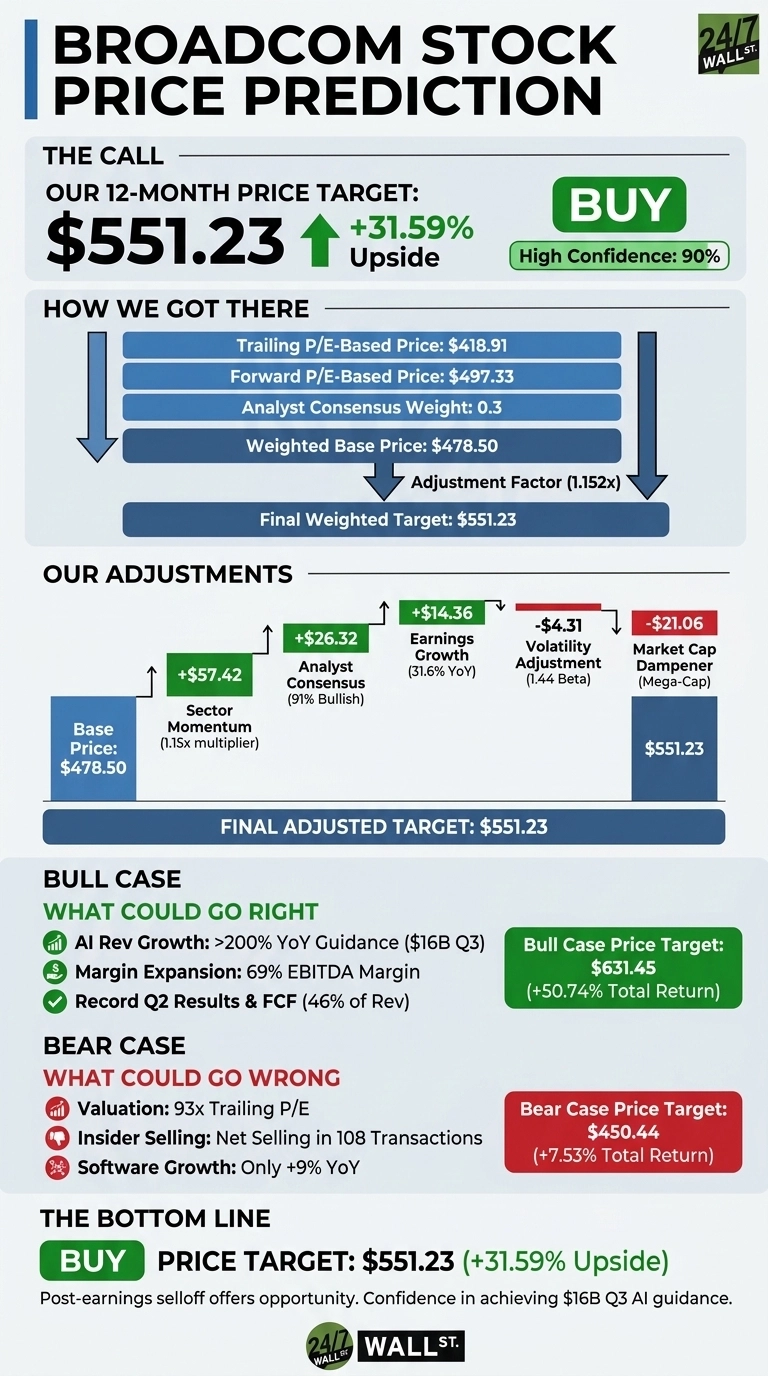

Our 24/7 Wall St. price target for Broadcom (NASDAQ:AVGO | AVGO Price Prediction) is $551.23, implying roughly 31.59% upside from the recent $418.91 close. After Broadcom’s brutal post-earnings selloff, I think the risk/reward has tilted firmly back toward buyers. Our model rates AVGO a buy, with confidence rated High (90%).

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $418.91 |

| 24/7 Wall St. Price Target | $551.23 |

| Upside | 31.59% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Record Quarter the Market Hated

Broadcom is having a strange week. Shares fell 12.59% on June 4, sliding from $495 at the filing to $418.91, even though Q2 FY2026 was a record quarter.

Revenue of $22.19 billion grew 47.9% YoY, EPS of $2.44 beat the $2.40 estimate (the 8th straight beat), and AI semiconductor revenue jumped 143% YoY to $10.8 billion. Reddit’s wallstreetbets crowd has gone from a sentiment score of 74 (bullish) to 13 (very bearish) in 36 hours. Even after the drop, AVGO is up 21.28% YTD and 61.74% over one year.

Why Bulls See a Breakout Ahead

The bull case rests on AI. Q3 FY2026 guidance calls for revenue of $29.4 billion and AI semiconductor revenue of $16 billion, up over 200% YoY. CEO Hock Tan said “Broadcom achieved record revenue, operating profit and free cash flow in Q2 driven by accelerating growth in AI semiconductor revenue and strong operating leverage.”

Free cash flow hit 46% of revenue, EBITDA margin reached 69%, and management is highlighting a longer-term AI revenue opportunity. Analyst consensus sits at $486.85 with 43 buy ratings versus 4 holds and no sells. Our bull case scenario puts Broadcom at $631.45 over 12 months, a 50.74% total return.

The Risks Worth Watching

The bear case starts with valuation. AVGO trades at a 93x trailing P/E and 43x forward P/E, leaving little room for guidance hiccups. Q2 software revenue grew only 9%, which Reddit users called out as “disappointing software revenue”. Insider activity shows net selling across 108 transactions, and customer concentration in hyperscale buyers remains a real risk if AI capex slows.

Bulls would counter that the software softness reflects the ongoing VMware subscription transition rather than demand erosion, and that insider selling at mega-caps is largely programmatic. Still, our bear case pegs 12-month downside at $450.44, a still-positive 7.53% return.

Broadcom Price Prediction 2026-2030

The 24/7 Wall St. price target of $551.23 reflects my view that the post-earnings selloff overshot. Broadcom just reported a 47.9% revenue growth quarter and guided to 84% growth ahead, yet trades below where it sat a week ago.

The case for owning here rests on confidence that Q3’s $16 billion AI guide is achievable. The case for waiting rests on the view that the 93x trailing multiple has to compress before AI tailwinds can lift it further. Our model output: Buy, with high confidence.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $478 |

| 2027 | $551 |

| 2030 | $917 |

These projections assume Broadcom continues executing on its custom-AI-accelerator roadmap and that hyperscale capex holds. Significant upside or downside could result from the pace of AI infrastructure spending and the success of the VMware subscription transition.

Contact [email protected] for any questions or corrections.