Tesla (NASDAQ:TSLA | TSLA Price Prediction) sits in an awkward place. Q1 2026 showed automotive gross margin rebounding to 21.1% from 16.2% a year earlier, FSD subscriptions hit 1.28 million (+51% YoY), and free cash flow more than doubled to $1.444 billion.

Yet shares closed at $418.45, down 6.95% YTD. Can Tesla reach $500 this cycle?

What’s Holding Tesla Back

The stock is stuck because investors cannot decide which Tesla they own. Shares are off 5.35% in the last week alone, even after rallying 7.47% over the past month. With a beta of 1.79, every macro wobble gets amplified.

The bigger overhang is strategic. Prediction markets peg a SpaceX-Tesla merger by year-end at just 42.5% probability, and the dominant view is that a combined entity would lose money on day one. Add in 43 recent insider transactions tilted toward selling, energy revenue down 12% YoY, and inventory rising to 27 days of supply, and buyers are hesitating.

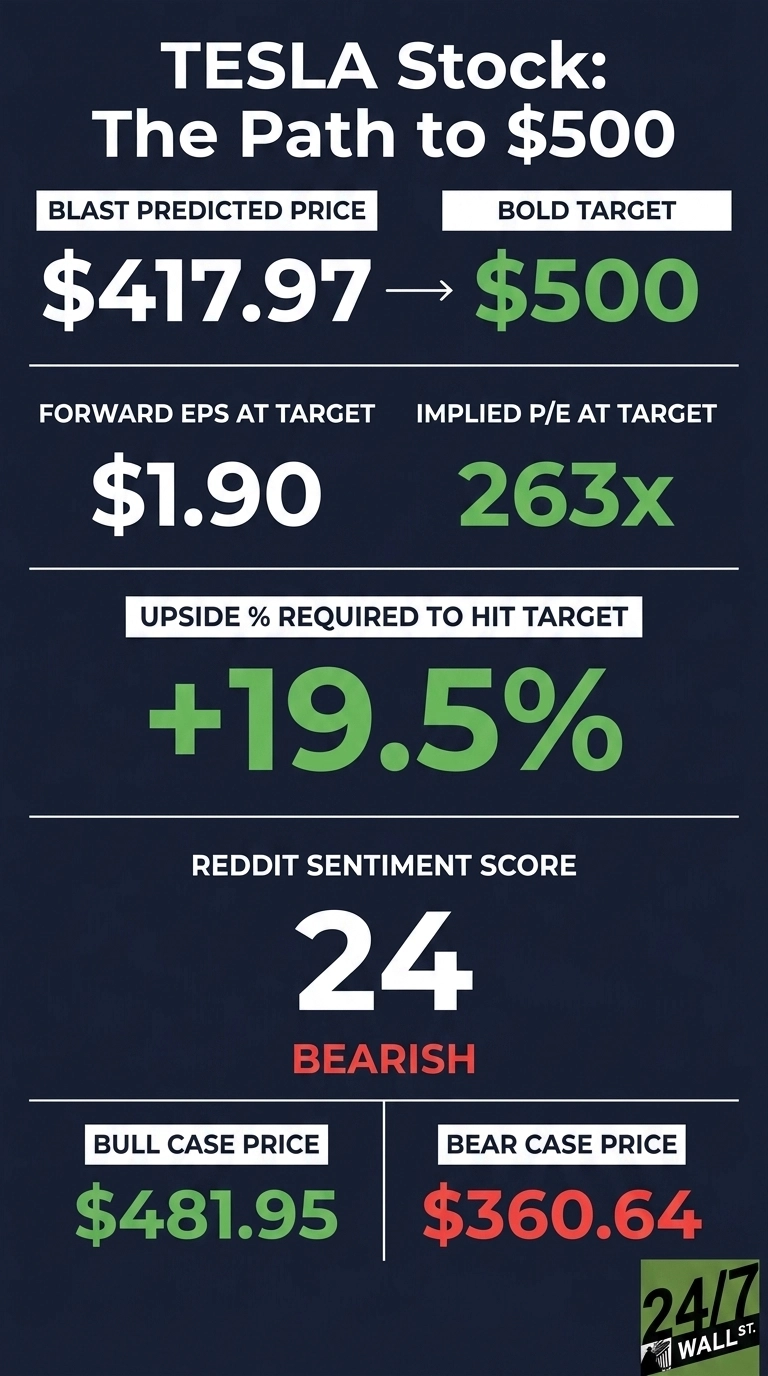

Wall Street Sees Modest Upside

Consensus is lukewarm. The Street’s average price target sits at $411.89, slightly below current price, with 5 Strong Buy, 18 Buy, 17 Hold, 4 Sell, and 3 Strong Sell ratings. My base case lands at $417.97 with 90% confidence, calling fair value. The bull scenario clocks in at $481.95, the bear at $360.64.

Only 49% of analysts are bullish, which undersells the operating leverage here. Q1 operating income jumped 135.84% YoY on modest revenue growth. That signals a business at an inflection point.

The Path to $500

Reaching $500 from today’s $418.45 requires a gain of 19.5%. With a forward EPS of $1.90, a $500 price implies a forward P/E of 263x. My base case at $417.97 already implies 231x, meaning the bold target needs roughly 32x additional multiple expansion.

That is substantial but not impossible if EPS growth accelerates. Catalysts include Cybercab, Tesla Semi, and Megapack 3 entering volume production in 2026, plus Optimus production lines at Fremont.

FSD v14.3 cut inference latency by up to 20%, and unsupervised Robotaxi rides are live in Dallas and Houston. Hit those milestones and forward EPS estimates move higher fast. Main risk: merger drama with SpaceX or xAI that confuses the equity story.

Valuation Today vs Earnings Power

At $418.45, Tesla trades at roughly 220x forward earnings of $1.90. That is rich on any backward-looking lens. Shares sit between a 52-week high of $498.83 and a low of $281.85, currently 17% off the high. Over 10 years, TSLA is up 2,744.28%, so the long-term compounding case is undeniable. The bull thesis to $500 asks whether autonomy and Optimus justify that triple-digit multiple.

Is $500 Realistic?

$500 requires a 19.5% move, and the 52-week high already brushed $498.83, so the level is not fantasy.

Three things need to go right: Q2 deliveries land in the 450,000 to 475,000 range the crowd expects, FSD subscriber growth stays north of 50% YoY, and SpaceX merger noise resolves cleanly.

What derails it: another quarter of regulatory-credit erosion paired with weak Optimus traction. Prediction markets assign 17% probability to $495 in June, so I am not promising it happens fast. Returns at this level shouldn’t be expected every year, but we’ve outlined the blueprint for how Tesla could reach $500 in 2026.

Contact [email protected] for any questions or corrections.