With the rate environment stabilizing in mid-2026, income investors are circling back to a familiar playbook: own the businesses that have raised payouts through every cycle in living memory. Dividend Kings and Aristocrats with 25-plus years of consecutive hikes offer a growing cash payment backed by durable franchises that the bond market still struggles to match consistently. Three names stand out this June for combining proven dividend track records with reasonable forward multiples and recent earnings momentum.

Here are the three dividend growth stocks worth a close look this month.

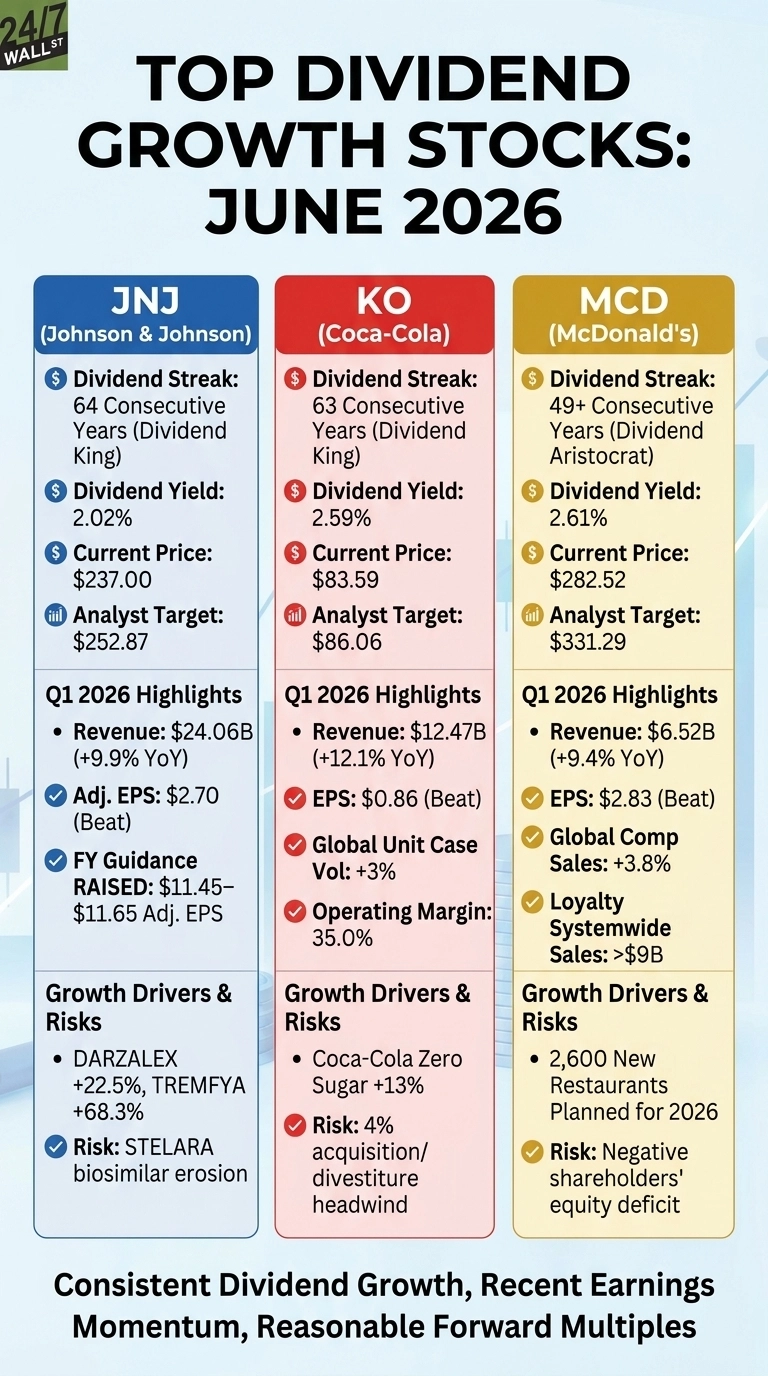

Johnson & Johnson (NYSE: JNJ)

Johnson & Johnson (NYSE:JNJ | JNJ Price Prediction) is the gold standard of dividend longevity. The healthcare giant just declared its 64th consecutive annual increase, raising the quarterly payout 3% to $1.34 per share, paid on June 9, 2026. That puts JNJ in a club almost no public company can claim membership in.

The fundamentals back the streak. Q1 2026 revenue came in at $24.06 billion, up 10% year over year, beating the $23.61 billion estimate. Management raised full-year guidance to $100.3 billion to $101.3 billion in revenue with adjusted EPS of $11.45 to $11.65. Oncology is doing the heavy lifting: DARZALEX grew 23% to $3.96 billion and TREMFYA jumped 68% to $1.61 billion. CEO Joaquin Duato said the company is “delivering on its promise for a year of accelerated growth and impact.”

Shares are up 16% year to date through June 9, yet the forward multiple sits at just 20x earnings with a 2% yield and an analyst target of $252.87. The caveat: STELARA biosimilar erosion drove sales down 60% to $656 million, and a planned Orthopaedics separation introduces execution risk. The pipeline is broad enough to absorb the hit, but it is a real near-term headwind to monitor.

Coca-Cola (NYSE: KO)

Coca-Cola (NYSE:KO) is the other beverage Dividend King in this group, with 63 consecutive years of dividend increases and $8.8 billion paid out to shareholders in 2025. The current quarterly dividend stands at $0.53 per share, with the next ex-dividend date on June 15, 2026.

Q1 2026 was a standout. Revenue hit $12.47 billion, up 12% year over year, with EPS of $0.86 versus $0.81 expected, the fourth straight beat. Global unit case volume rose 3%, led by China, the US, and India, while Coca-Cola Zero Sugar volume grew 13% across all segments. Operating margin expanded to 35% from 33%. Management lifted full-year guidance to 4% to 5% organic revenue growth and 8% to 9% comparable EPS growth, with free cash flow targeted at roughly $12.2 billion.

KO trades at a forward P/E of 24x with a 3% yield, and the stock has run 20% year to date against an analyst target of $86.06. The risk worth flagging: acquisitions and divestitures are a ~4% headwind, and Asia Pacific comparable operating income fell 17%. CEO Henrique Braun framed the quarter as reflecting “our unwavering focus on staying close to the consumer, executing locally and managing complexity.”

McDonald’s (NYSE: MCD)

McDonald’s (NYSE:MCD) rounds out the list as the relative value play. The stock is down 6% year to date, trading well below its 200-day moving average of $306.47, even as the burger giant continues a streak of 49-plus consecutive years of dividend increases as a Dividend Aristocrat. The current quarterly dividend of $1.86 reflects a 5% raise from October 2025.

Q1 2026 showed the operating engine reaccelerating. Revenue rose 9% to $6.52 billion, EPS landed at $2.83 versus $2.74 expected, and global comparable sales jumped 4% after going negative a year ago. US comps grew 4%, and loyalty systemwide sales topped $9 billion in the quarter across 70 markets. CEO Chris Kempczinski put it directly: “McDonald’s delivered this quarter. Our 6% global Systemwide sales growth shows how we executed with discipline, proving that we can drive results even in a challenging environment.”

The numbers behind the thesis: a 3% yield, forward P/E of 22x, operating margin in the mid-to-high 40% range, and an analyst price target of $331.29. Roughly 2,600 new restaurants are planned for 2026. The caveat investors should weigh: a negative shareholders’ equity deficit of $1.79 billion, ongoing restructuring charges from Accelerating the Organization continuing through 2027, and tariff/trade exposure on the input side.

Why These Three, Why Now

Each of these names cleared the same screen: a multi-decade history of dividend increases, recent earnings momentum confirmed by the most recent quarter, and a forward multiple that does not require heroic assumptions to justify. JNJ and KO offer the dividend longevity premium with current-year tailwinds, while MCD offers the discount entry on a Dividend Aristocrat trading below its 200-day average. For investors seeking proven income compounders as rates stabilize, the bar these three clear is hard to replicate elsewhere in the large-cap universe.

Contact [email protected] for any questions or corrections.