Wall Street’s verdict on Broadcom (NASDAQ:AVGO | AVGO Price Prediction) is unambiguously bullish, with the analyst consensus price target now sitting above the stock’s own 52-week high after a brutal post-earnings selloff. The smart money signal is clear: sell-side desks have leaned harder into the name precisely as retail capitulated, and institutional positioning hasn’t blinked.

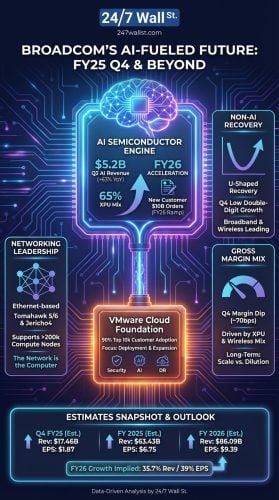

Broadcom stock currently trades near $376, after a sharp post-earnings drawdown from $495 at the time of its Q2 FY2026 earnings filing. The pullback came despite a record quarter and a guidance bar that implies 84% year-over-year revenue growth for Q3 FY2026.

That dislocation is the headline story. Analysts haven’t followed retail out the door, and the consensus number now looks like a monster target rather than a modest one.

The Analyst Signal Is Loud

The Wall Street consensus price target on Broadcom stock stands at $522.06, a level that sits above the stock’s 52-week high of $495. The coverage book is heavily skewed bullish: 7 Strong Buy, 37 Buy, 4 Hold, zero Sell, and zero Strong Sell ratings, or roughly 92% bullish.

Institutional positioning corroborates that conviction. 80% of Broadcom’s float sits in institutional hands, and there’s no visible exit by the funds that actually move the tape. Mizuho’s recent ASIC channel-check note flagged a large TPU shipment ramp and a sizable revenue opportunity tied to the Google relationship and the Apollo and Blackstone AI partnership, an example of the bullish framework on the sell side.

Crowd sentiment tells the opposite story. Reddit chatter on AVGO stock has been neutral with low activity, and a Polymarket contract on Broadcom becoming the second-largest company by market cap on June 30 sits at just less than 1% implied probability. In other words, the professional bid and the retail bid have decoupled.

The Gap Between Wall Street and the Tape

The arithmetic gap between the $522.06 consensus and Broadcom’s current handle widened sharply this month after AVGO stock fell 12% over the past month, even as fiscal year results came in ahead of estimates on every line. Broadcom’s Q2 FY2026 non-GAAP EPS landed at $2.44, AI semiconductor revenue hit $10.8 billion, and management guided Q3 AI revenue to $16 billion, up over 200% year over year.

The bear case is real and worth weighing, though. Broadcom trades at a P/E ratio of 66x trailing and a forward earnings multiple of 34x, gross margin is set to compress to 74% in Q3 as TPU mix scales, and the customer base is concentrated among a handful of hyperscalers. Broadcom CFO Kirsten Spears acknowledged on the call that “as the TPUs continue to accelerate, there will be pressure overall on gross margin.”

The bull case rests on visibility. Broadcom CEO Hock Tan reiterated guidance for fiscal 2027 AI semiconductor revenue in excess of $100 billion, with Q2 AI bookings of over $30 billion against $10.8 billion shipped. That kind of book-to-bill is what the consensus target is leaning on.

Is the Smart Money Right?

The honest read is that Wall Street’s $522 price target for Broadcom stock is probably still too cheap. Broadcom’s record AI revenue, 200%-plus guided growth, and a $30 billion bookings number are hard to dismiss. The risks (valuation, margin mix, customer concentration) shouldn’t be overlooked, however.

Investors weighing AVGO stock today have a clean setup to evaluate against their own time horizon and risk tolerance. Moderate position sizing and a willingness to add on further weakness is the framework most consistent with what the consensus target, the institutional book, and Broadcom’s own guidance are saying together.

Contact [email protected] for any questions or corrections.