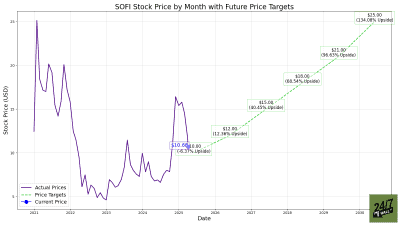

I keep hitting the buy button on SoFi Technologies (NASDAQ:SOFI | SOFI Price Prediction), and the Fed-driven tech sell-off this month has only made my finger heavier. The stock sits at $16.67, down 36.33% year to date, while the QQQ has gained 16.74% over the same window. That gap is the opportunity. The market is pricing SoFi like a bruised fintech. I am buying it like a national bank that happens to be quietly rewiring how 14.7 million people manage money.

My core thesis is simple. SoFi is becoming a financial services operating system, and the cross-sell data proves it. In Q1 2026, 43% of new products were opened by existing members, up from 36% a year earlier. CEO Anthony Noto said it bluntly on the call: “When other companies are stumbling, our revenue growth is accelerating.” I believe him because the numbers back the mouth.

Three reasons the conviction holds

First, the earnings power is real and compounding. Q1 net income hit $166.73 million, up 134.45% year over year, on operating income growth of 150.12%. Adjusted EBITDA was $339.9 million at a 31% margin. Management is guiding 2026 to roughly $4.655 billion in adjusted net revenue and $0.60 in adjusted EPS, with a medium-term adjusted EPS CAGR of 38% to 42% through 2028. A forward P/E of 27x against that growth rate is the “dirt-cheap” part of the title.

Second, the deposit machine is funding everything. SoFi ended the quarter with $40.24 billion in deposits, funding over 90% of total liabilities, and drove cost of funds down 48 basis points year over year. That bank charter is the moat. It is why loan originations of $12.18 billion grew 68% without blowing up the balance sheet, and why tangible book value per share climbed to $7.21, up 57% year over year.

Third, the optionality is free. SoFiUSD is the first stablecoin accessible directly within a traditional, national bank application, now integrated with Mastercard for global settlement. The Loan Platform Business added $3.6 billion of new commitments with three new partners, including a leading global bank. None of that is in the analyst consensus target of $21. The CEO is buying his own stock: Noto picked up 31,423 shares in early May between $15.73 and $16.00.

The honest risk I am underwriting

The Technology Platform segment is the wart. Revenue fell 27% year over year after a large client departed, and enabled accounts dropped 16%. Credit is drifting the wrong way, with the personal loan charge-off rate rising sequentially to 3.03% from 2.80%. I am sizing for it. Management still expects tech platform like-for-like growth of about 12%, and the personal loan book carries a weighted average FICO of 745 and weighted average income of $154,000. The borrower base is prime, the capital ratio sits at 21%, double the 10.5% regulatory minimum, and I would rather own that risk at $16 than at $26.

Why the buy button stays active

Reddit went from a bullish 68 on May 29 to a bearish 22 the next morning. That kind of whiplash is exactly when long-term owners get paid. I will keep buying SoFi as long as members grow north of 30%, deposits keep funding the loan book, and Noto keeps shipping products faster than the market can price them. The Fed sets the weather. SoFi is building the house.

Contact [email protected] for any questions or corrections.