Starbucks (NASDAQ: SBUX | SBUX Price Prediction) and McDonald’s (NYSE: MCD) both delivered upbeat quarters this spring, but the stories underneath could not be more different.

Starbucks is mid-turnaround under CEO Brian Niccol, while McDonald’s is a steady franchised cash machine led by Chris Kempczinski. If you are deciding where to park $10,000, the choice comes down to turnaround upside versus durable scale.

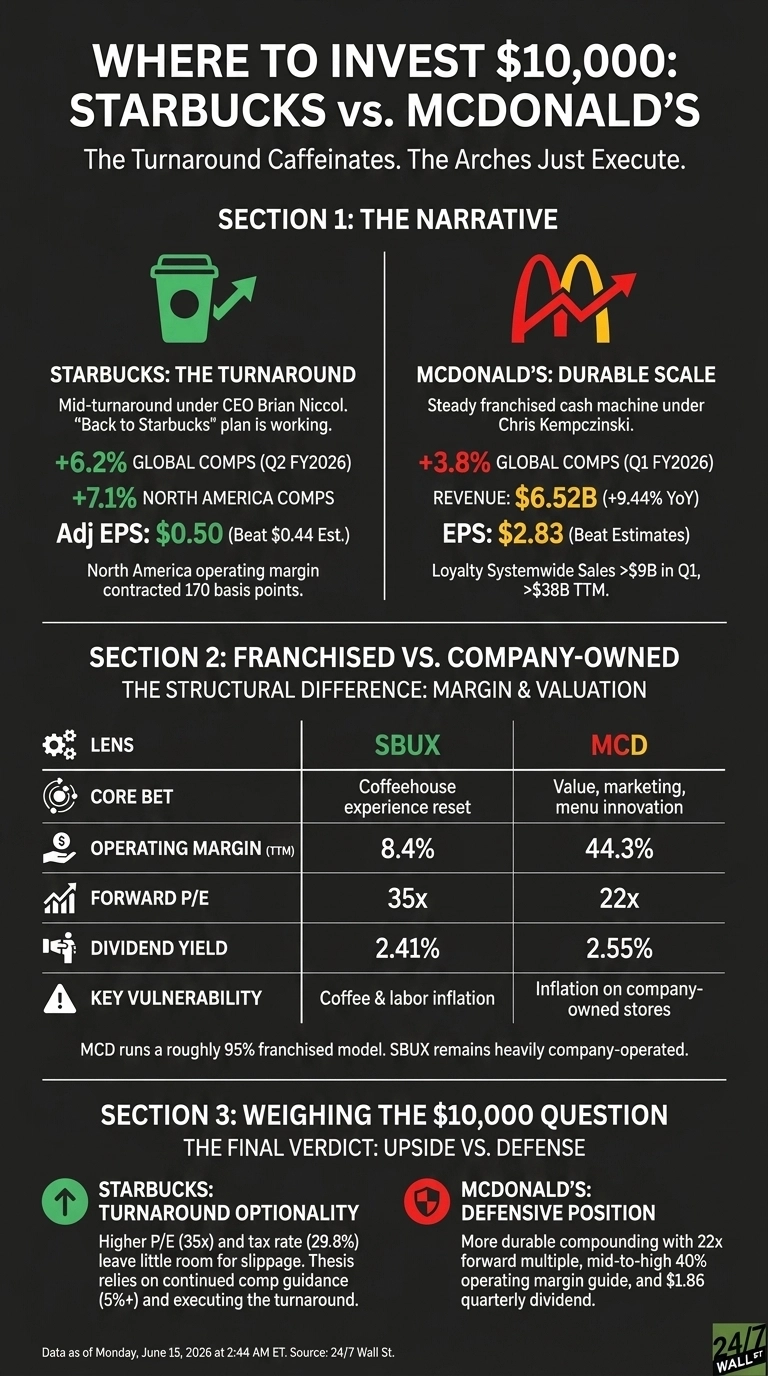

The Turnaround Caffeinates. The Arches Just Execute.

Starbucks’ Q2 FY2026 was the clearest sign yet that the “Back to Starbucks” plan is working. Global comps rose 6.2%, with North America jumping 7.1% on 4.4% transaction growth. Real customers are walking back through the doors.

Adjusted EPS of $0.50 beat the $0.44 estimate, and revenue hit $9.53 billion. Niccol called it “the turn in our turnaround.” The catch: North America operating margin contracted 170 basis points on labor investments, tariffs, and coffee inflation. China comps barely moved at 0.5%, prompting the Boyu Capital JV that hands operating control to a local partner.

McDonald’s Q1 FY2026 was less dramatic and arguably more reassuring. Revenue grew 9.44% to $6.52 billion, EPS of $2.83 beat estimates, and global comps rebounded to +3.8% after a negative reading a year earlier.

International Operated Markets revenue jumped 14%, helped by the UK, Germany, and Australia. Loyalty is the quiet weapon: systemwide sales to members topped $9 billion in the quarter and $38 billion on a trailing basis.

Franchised Cash Flow vs. Company-Owned Risk

| Lens | SBUX | MCD |

| Core bet | Coffeehouse experience reset | Value, marketing, menu innovation |

| Operating margin (TTM) | 8.4% | 44.3% |

| Forward P/E | 35x | 22x |

| Dividend yield | 2.41% | 2.55% |

| Key vulnerability | Coffee and labor inflation | Inflation on company-owned stores |

McDonald’s runs a roughly 95% franchised model, which is why franchised restaurants generated $4.01 billion of the quarter’s revenue with much higher pass-through economics.

Starbucks remains heavily company-operated, meaning every wage hike and bean cost lands directly on its P&L. That structural difference shows up in margin and in valuation.

The Next Test Is Pricing Power and Loyalty

I will be watching whether Starbucks can hold the 5% or greater comp guidance into fiscal H2 as the China JV reshapes reported revenue. For McDonald’s, the question is whether loyalty across 70 markets can keep lifting check size while value menus protect traffic.

Shares since earnings tell a story: SBUX is up 6.54% since April 28, while MCD has nudged just 1.07% higher since May 7. Year to date, SBUX has run 23.88%, MCD is down 5.66%. Reddit retail sentiment on MCD has skewed bearish in early June, which is worth noting but not investing on.

Weighing the $10,000 Question

On the numbers, McDonald’s looks like the more defensive position. The combination of a 22x forward multiple, mid-to-high 40% operating margin guide, and $1.86 quarterly dividend supports durable compounding while the stock sits below its 200-day average.

Starbucks offers more turnaround optionality, though the 35x forward P/E and 29.8% tax rate leave little room for slippage. If coffee inflation worsens or U.S. comps stall, the Starbucks thesis is the first to reassess.

Contact [email protected] for any questions or corrections.