Investors in the semiconductor capital equipment sector often face a structural question about where value is created in the supply chain. The largest equipment manufacturers—companies such as Applied Materials (NASDAQ:AMAT | AMAT Price Prediction) and Lam Research (NYSE:LRCX)—design and sell complete semiconductor manufacturing systems. Surrounding these firms is a large ecosystem of suppliers that provide subsystems, fluid delivery systems, precision components, robotics, and process control technologies that are integrated into those systems.

Because these suppliers participate directly in the manufacturing tools sold by the equipment companies, their revenue growth is closely tied to wafer fabrication equipment (WFE) spending cycles. This relationship has drawn renewed attention following recent earnings reports and analyst upgrades across several supply chain companies.

For example, following its fiscal fourth-quarter earnings beat, Needham raised its price target on Ultra Clean Holdings (NASDAQ:UCTT) to $70 from $50 on February 24 while maintaining a Buy rating. The firm cited improving customer forecasts and expectations for 15%–20% growth in wafer fabrication equipment spending, with a step-function increase anticipated later in the year. TD Cowen also raised its price target on UCTT to $70 from $35 while maintaining a Buy rating and highlighting strengthening demand expectations for leading-edge logic and DRAM, particularly high-bandwidth memory (HBM), which benefits deposition, etch, and CMP equipment suppliers. On the same day, Oppenheimer reiterated its Outperform rating on UCTT and raised its price target, citing strong guidance and a 2026 revenue growth outlook of roughly 15%–20%.

Such upgrades reinforce the view that subsystem suppliers tied to leading-edge semiconductor manufacturing are positioned to benefit from the next capital spending cycle in wafer fabrication equipment.

Yet the critical investment question remains unresolved. While suppliers participate in the growth of semiconductor capital spending, the equipment manufacturers themselves control the system architecture, the customer relationship with semiconductor fabs, and the majority of system-level revenue. Historically, this structural position has allowed equipment companies to capture a larger share of the value created during semiconductor capital spending cycles.

This article therefore examines a fundamental investment question within the semiconductor equipment ecosystem: is it better to invest in the equipment manufacturers themselves—Applied Materials and Lam Research—or in key suppliers within their supply chains such as MKS Instruments (NASDAQ:MKSI), Ultra Clean Holdings (UCTT), and Ichor Holdings (NASDAQ:ICHR)?

Pros and Cons of Investing in Smaller Supply Chain Companies

Supply chain companies are typically smaller than their major customers and can therefore offer potentially higher growth rates. Their products are often highly specialized and tightly integrated into the design of semiconductor manufacturing equipment. These relationships can create long-term customer partnerships and recurring revenue streams.

Subsystem suppliers also frequently possess niche technological expertise that makes them difficult to replace once their components are designed into a semiconductor tool platform. This dynamic can provide stable revenue opportunities during industry upcycles.

MKS Instruments differs somewhat from Ichor and Ultra Clean in that it serves multiple end markets including industrial, photonics, and life sciences applications. This diversification reduces reliance on semiconductor capital spending and can partially offset cyclicality in the semiconductor equipment sector.

However, investing in smaller supply chain companies carries significant risks. These firms are often heavily dependent on a small number of customers. If those customers experience order declines or adjust production schedules, the impact on supplier revenue can be immediate and severe.

Smaller companies also tend to have fewer financial resources and less pricing power than their larger customers. During semiconductor industry downturns, subsystem suppliers often experience sharper revenue contractions and more volatile earnings than the equipment manufacturers themselves.

Analysis of Applied Materials and Lam Research

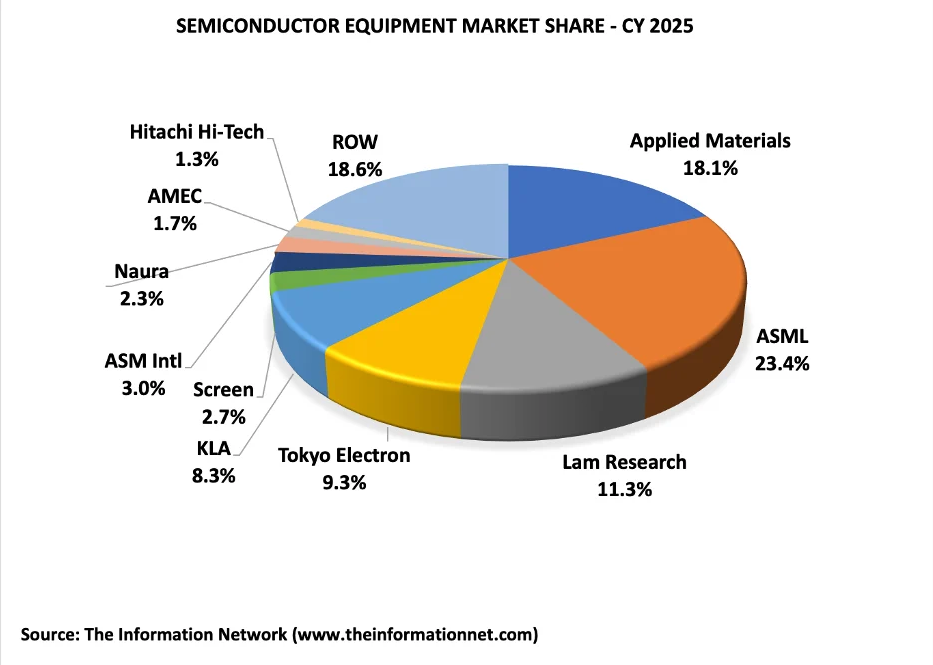

Applied Materials and Lam Research are among the largest semiconductor equipment manufacturers in the world. According to Chart 1, which shows 2025 semiconductor equipment market share and is derived from my report entitled “Global Semiconductor Equipment: Markets, Market Share, Market Forecasts“, Applied Materials ranked second globally with approximately 18% market share while Lam Research ranked third with roughly 11% share.

Chart 1. Global Semiconductor Equipment Suppliers Top 10 2025

The scale of these market shares reflects not only the strength of the equipment companies themselves but also the extensive network of suppliers that provide the subsystems and components integrated into each tool platform.

These companies assemble complex semiconductor manufacturing systems using thousands of parts sourced from suppliers around the world. Subsystem providers supply critical technologies ranging from gas delivery systems and vacuum components to robotics, motion control systems, and precision machined parts.

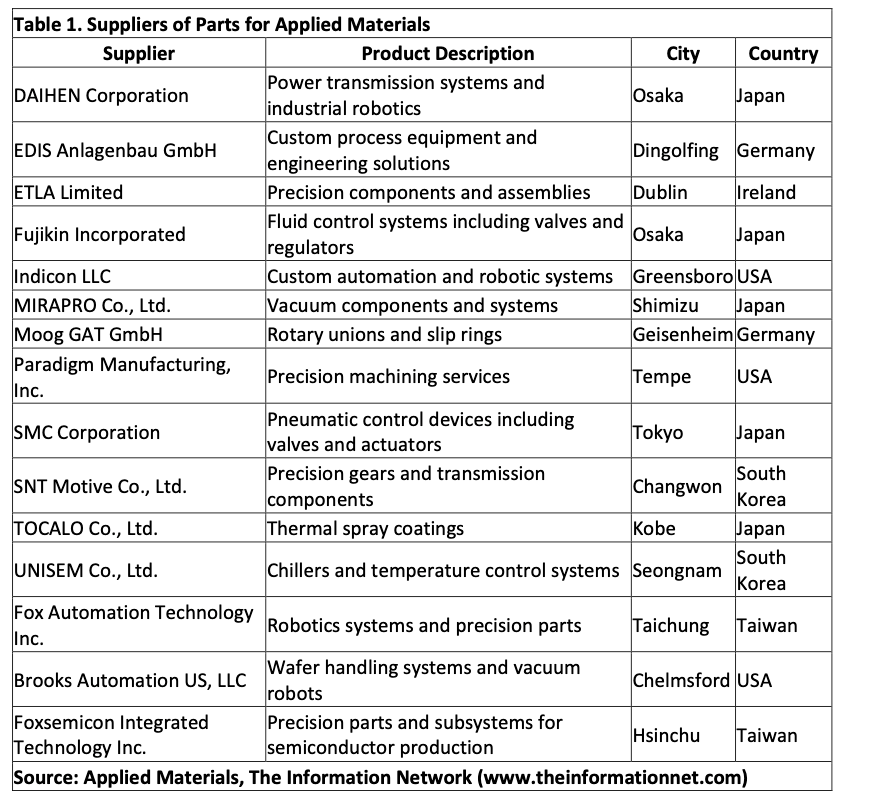

According to Table 1, the diversity of suppliers supporting Applied Materials reflects the global nature of the semiconductor equipment supply chain.

Sales Analysis of Suppliers to Applied Materials and Lam Research

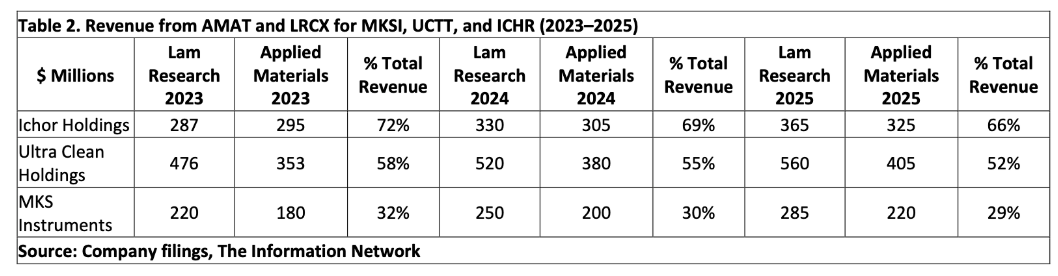

Subsystem suppliers generate significant revenue from their largest customers, reflecting the highly integrated nature of semiconductor equipment manufacturing. Companies such as Ichor Holdings, Ultra Clean Holdings, and MKS Instruments provide subsystems that are designed directly into the equipment platforms of Applied Materials and Lam Research.

According to Table 2, revenue derived from these two equipment manufacturers represents a substantial portion of total sales for these suppliers. The table illustrates how dependent subsystem suppliers can be on a small number of equipment companies, which exposes them to fluctuations in tool demand but also allows them to benefit directly when equipment build rates increase during semiconductor capital spending upcycles.

The data illustrate the concentration risk inherent in the semiconductor equipment supply chain. While subsystem suppliers participate directly in equipment growth cycles, their revenues remain closely tied to the order patterns of a limited number of customers. When tool shipments rise, suppliers benefit from higher subsystem demand, but when capital spending slows, revenue declines can occur rapidly because of the limited diversification of their customer base.

Structural Value Capture in the Semiconductor Equipment Supply Chain

The structural position of semiconductor equipment manufacturers within the value chain helps explain why they have historically delivered stronger financial performance than many of their subsystem suppliers. Equipment companies such as Applied Materials and Lam Research sell complete manufacturing systems directly to semiconductor fabs, often with average selling prices ranging from several million dollars to well over $100 million for advanced process tools.

Subsystem suppliers, by contrast, typically provide specialized components that represent only a fraction of the total system value. Fluid delivery systems, vacuum components, robotics, gas panels, and other subsystems are essential to tool performance, but they account for a relatively small portion of the final system price. As a result, suppliers generally operate with lower margins and have limited pricing leverage compared with the equipment manufacturers that control the overall system design.

Another important structural difference is the ownership of the customer relationship. Semiconductor manufacturers purchase equipment systems directly from companies such as Applied Materials and Lam Research, which maintain long-term service contracts and process integration partnerships with their customers. Subsystem suppliers, however, typically sell to the equipment companies rather than directly to the semiconductor fabs.

These structural dynamics help explain why the largest semiconductor equipment manufacturers often capture a disproportionate share of the financial returns generated during semiconductor industry upcycles.

According to Chart 2, share price performance over the past year reflects the strong recovery in semiconductor capital spending following the 2023 downturn. Lam Research and Applied Materials both benefited from accelerating demand for deposition and etch equipment tied to advanced logic, memory, and AI-related infrastructure. Suppliers such as MKS Instruments and Ultra Clean Holdings also participated in this recovery as tool build rates increased across major equipment manufacturers. However, the magnitude of performance across the group varies significantly, illustrating the differing levels of operating leverage and market exposure among the equipment companies and their subsystem suppliers.

Chart 2. Share Price Performance – 6 Months

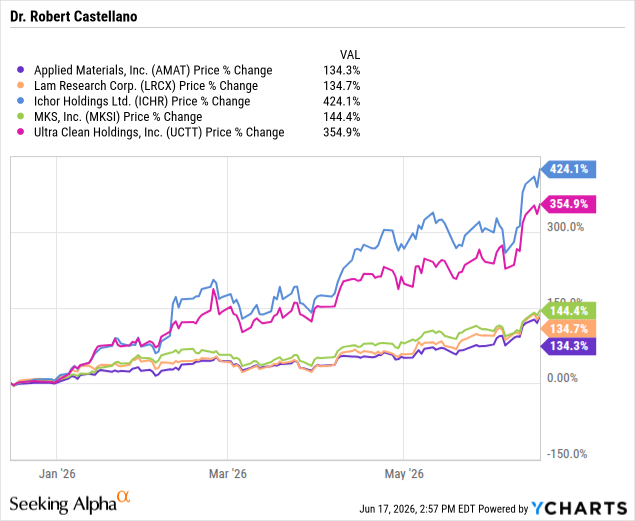

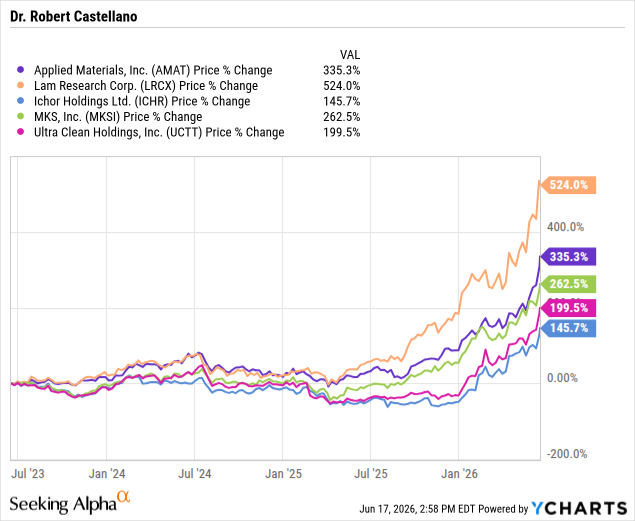

According to Chart 3, the longer three-year performance horizon provides a clearer view of how value has been captured across the semiconductor equipment supply chain. Over this period, the largest equipment manufacturers have generally outperformed their suppliers, reflecting their control of the system architecture, customer relationships with semiconductor manufacturers, and a larger share of the total system revenue. Subsystem suppliers such as Ichor Holdings and Ultra Clean Holdings remain highly leveraged to equipment demand, but their financial performance is more sensitive to cyclical fluctuations in tool shipments and customer concentration.

Chart 3. Share Price Performance – 3 Years

Over a longer three-year period the performance divergence becomes more apparent, with the largest equipment manufacturers generally outperforming their suppliers.

Investor Takeaway

The semiconductor equipment ecosystem illustrates a classic supply-chain investment dilemma. Suppliers participate in the growth of semiconductor capital spending and can experience significant revenue expansion during industry upcycles. However, the equipment manufacturers themselves control system architecture, customer relationships, and the majority of system-level revenue.

The historical share-price performance presented in this article suggests that the equipment manufacturers have captured a larger portion of the value created during semiconductor capital spending cycles.

While companies such as MKS Instruments, Ultra Clean Holdings, and Ichor Holdings remain important participants in the semiconductor manufacturing ecosystem, investors seeking exposure to long-term growth in wafer fabrication equipment spending may find that the system manufacturers—Applied Materials and Lam Research—have historically provided more consistent returns.

Contact [email protected] for any questions or corrections.