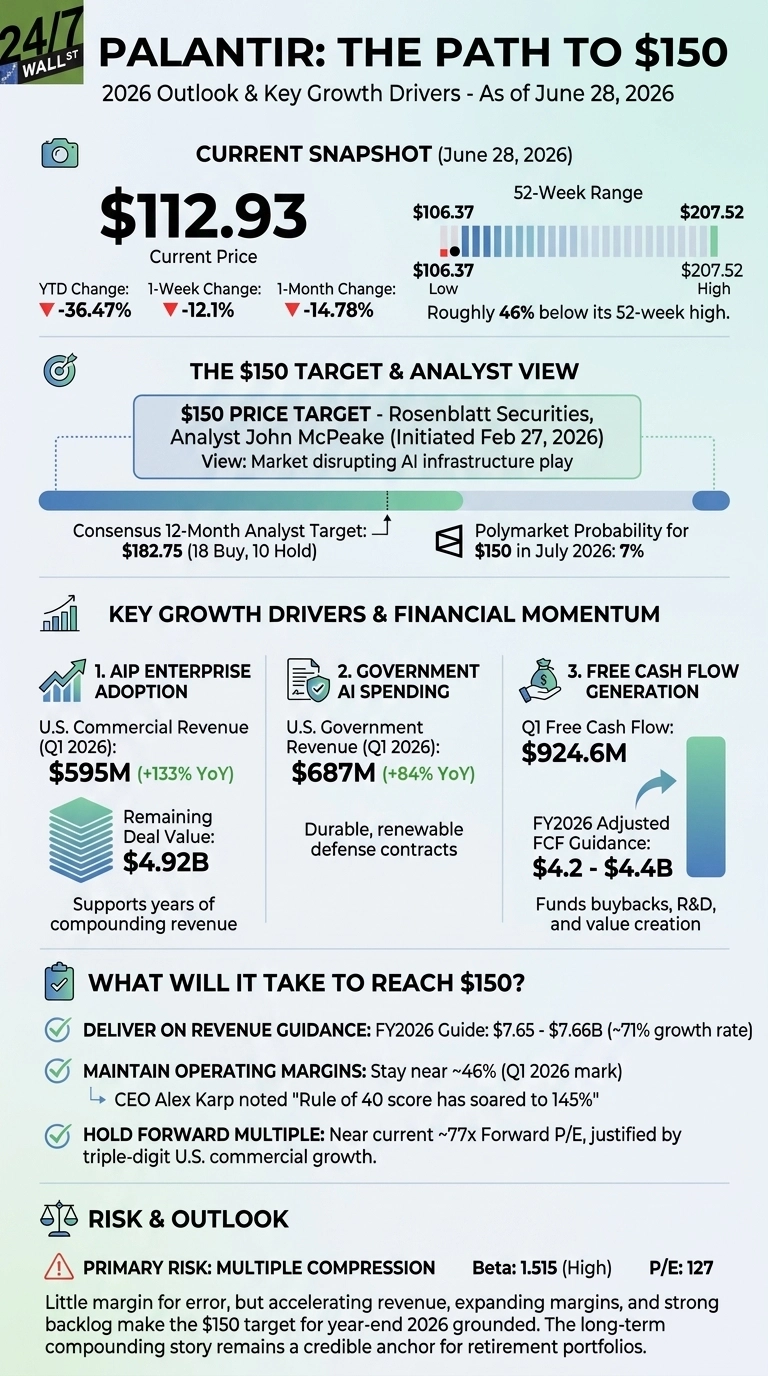

Palantir Technologies (NASDAQ:PLTR | PLTR Price Prediction) has handed retirement investors a wild ride in 2026. Shares of Palantir closed Friday at $112.93, down 12.1% over the past week, 14.78% over the past month, and 36.47% year to date from a starting price of $177.75. The one year change sits at negative 21.71%, and the stock is roughly 46% below its 52 week high of $207.52.

Despite the pullback, most of the Street still holds moderate forecasts. The consensus 12 month analyst target sits at $182.75, with 18 Buy ratings, 10 Holds, and a couple of bears.

But veteran Rosenblatt Securities analyst John McPeake made waves earlier this year when he initiated coverage on February 27, 2026 with a Buy rating and a $150 price target, calling Palantir a market disrupting AI infrastructure play. From today’s price, that target implies meaningful upside by year end 2026.

That is well above the Polymarket crowd, which currently assigns just a 7% probability to PLTR hitting $150 in July, and below the broader sell side consensus. But can PLTR realistically reach $150 by the end of 2026?

McPeake’s thesis rests on operating leverage that is showing up in the numbers right now. Palantir’s Q1 2026 revenue grew 84.7% year over year to $1.632 billion, the highest growth rate in company history, and GAAP operating income reached $754 million at a 46% margin. CEO Alex Karp noted the “Rule of 40 score has soared to 145%”, a level matched only by NVIDIA, Micron, and SK hynix.

Key Drivers of PLTR Stock Performance

- AIP enterprise adoption. U.S. commercial revenue jumped 133% year over year to $595 million in Q1, with remaining deal value of $4.92 billion. For long term retirement accounts, that backlog supports years of compounding revenue over multiple quarters.

- Government AI spending. U.S. government revenue grew 84% year over year to $687 million. Defense and intelligence contracts are durable and renewable, the kind of recurring base retirement portfolios prize.

- Free cash flow generation. Q1 free cash flow hit $924.6 million, and management guides FY2026 adjusted free cash flow of $4.2 to $4.4 billion. Compounding cash flow at this scale is what funds buybacks, R&D, and the next leg of value creation.

What Will It Take for PLTR to Reach $150?

The math is clean. With 2,296,071,000 shares outstanding, $150 implies a materially larger market cap than today’s $270.7 billion. Three conditions need to hold:

- Palantir delivers on its raised FY2026 revenue guide of $7.65 to $7.66 billion, a 71% growth rate.

- Operating margins stay near the 46% Q1 mark, validating the Rule of 40 narrative.

- The forward multiple holds near its current 77x, justified by triple digit U.S. commercial growth.

The primary risk is multiple compression: a high beta of 1.515 and a P/E of 127 leave little margin for any guidance miss. Even so, with revenue growth accelerating, margins expanding, and a $4.92 billion U.S. commercial backlog already in hand, McPeake’s $150 target for year end 2026 looks well grounded, and the long term compounding story remains a credible anchor for retirement portfolios.

Contact [email protected] for any questions or corrections.