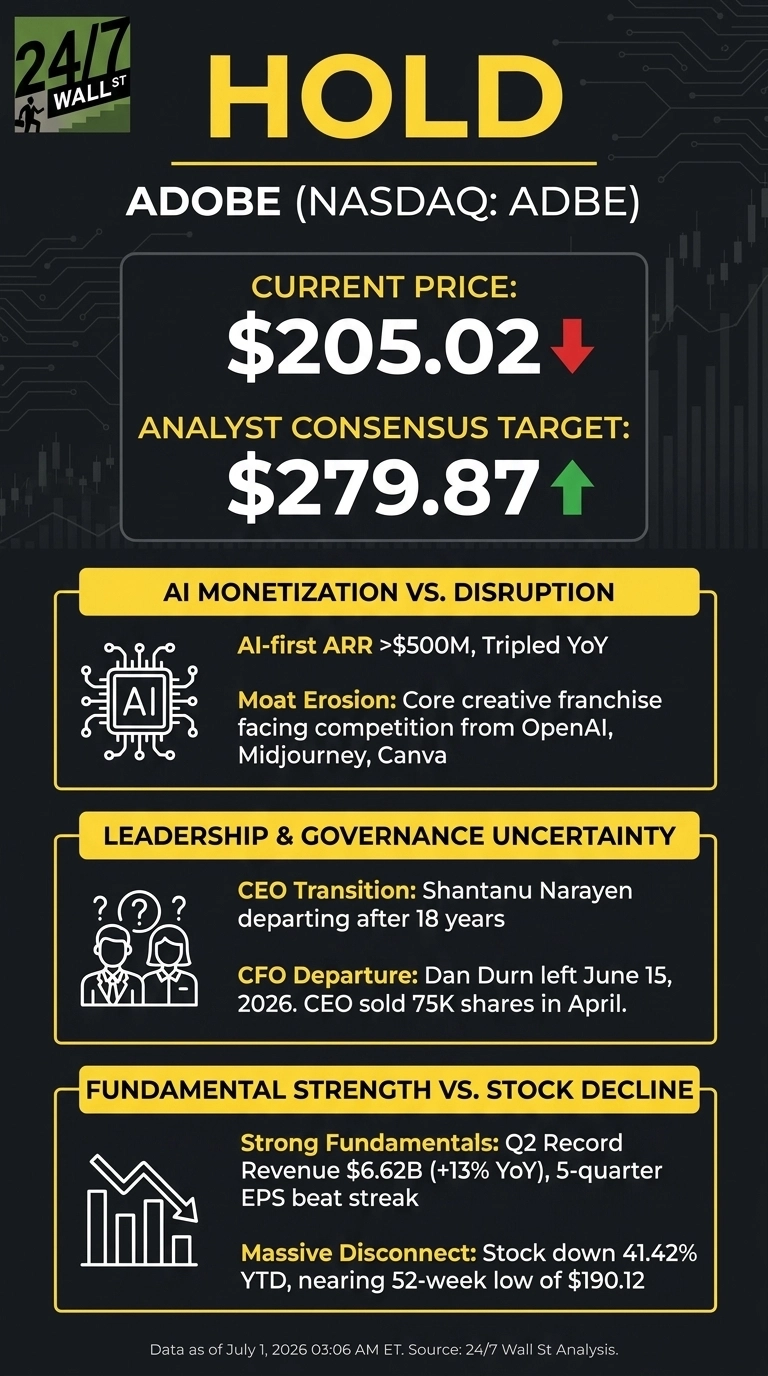

At $205.02, Adobe (NASDAQ:ADBE | ADBE Price Prediction) is a Hold. The stock sits within striking distance of its 52-week low of $190.12, yet the underlying business is putting up record numbers, creating an interesting disconnect in large-cap software.

Adobe owns the creative software stack professionals default to (Photoshop, Illustrator, Premiere, Acrobat), and has repositioned around generative AI through Firefly, Express, GenStudio, and AEP. The market has stopped paying software-multiple prices for that franchise.

Shares have slid from a 52-week high of $386.88 as investors weigh AI disruption from OpenAI, Midjourney, and Canva against Adobe’s own AI monetization ramp.

A CEO transition after 18 years under Shantanu Narayen and the June 15, 2026 departure of CFO Dan Durn compound the issue: a fundamentally strong business trading like a broken one.

Why the Selloff Looks Like an Opportunity

Adobe trades at a forward P/E of 8 and a PEG ratio of 0.554, extraordinary for a business generating a 28.7% profit margin and 62.9% return on equity. Free cash flow is prolific: $10.03 billion in operating cash flow in FY2025.

Fundamentals are accelerating. Q2 FY2026 delivered record revenue of $6.62 billion, up 13% YoY, with non-GAAP EPS of $5.96 extending a five-quarter beat streak. AI-first ARR tripled year over year to exceed $500 million, and management raised FY2026 guidance to $26.50 billion to $26.60 billion in revenue.

Capital return underscores conviction. Adobe repurchased $2.11 billion in stock in Q2 alone, and Director David Ricks bought 10,000 shares at $194.513 on June 25, a rare open-market accumulation near the low.

Why the Market Is Losing Patience

Adobe’s moat is eroding in real time. Generative AI tools from OpenAI, Midjourney, and Canva now handle image, video, and layout tasks that once required a Creative Cloud subscription. Adobe’s own $450 million stock business is declining faster than management modeled.

ARR growth has decelerated to roughly 10.2%, a reset for a stock that once traded on 15%-plus growth expectations. The Q2 $70 million goodwill impairment on the Publishing & Advertising unit and a $30 million litigation accrual pressured GAAP results.

Governance is another overhang. Narayen is leaving, CFO Dan Durn is gone, and the CEO sold 75,000 shares in late April at $243 to $245. Reddit sentiment has turned bearish, with scores between 35 and 38 heading into July.

Why Patience Beats Conviction

Adobe’s numbers are unambiguously good, but the stock’s action tells a different story. Multiple compression this severe usually resolves only when a catalyst forces the market to re-underwrite the business.

Two catalysts stand out. First, naming a new CEO will reset the leadership discount; the search is expected to take a few months. Second, the Semrush integration and continued AI-first ARR compounding must show Adobe is capturing AI value rather than defending against it.

Until then, buying feels early and selling feels late. The forward multiple already reflects deep skepticism, and fundamentals do not justify capitulation.

What the Numbers Say

Adobe trades at $205.02 against an analyst consensus target of $279.87, implying roughly 36.5% upside. Coverage runs 39 analysts deep, with 3 Strong Buy, 12 Buy, 20 Hold, and 4 Sell ratings, mirroring the Hold verdict.

Valuation is compelling: a trailing P/E of 12, forward P/E of 8, and EV/EBITDA of 8.1. Performance tells the other side. ADBE is down 41.42% year to date and 47.01% over one year, while the S&P 500 is up 9.51% YTD and 20.87% over one year.

The Case for Standing Still

At $205.02, Adobe is a hold.

Two things must resolve before the risk/reward tilts decisively: a new CEO with credible AI product credentials, and AI-first ARR continuing its current trajectory past $1 billion to prove the franchise is expanding faster than it is being cannibalized. Both are plausible over the next two to four quarters, but neither is in hand today.

If Adobe re-rates on a positive CEO announcement or a Q3 beat extending the AI-first ARR curve, missing the first 10% to 15% of the move is acceptable given leadership overhangs. A further leg down toward the $190.12 52-week low remains possible if AI disruption headlines intensify.

Watch three items: AI-first ARR growth relative to the current $500 million run rate, Creative & Marketing subscription growth holding at or above the 13% pace, and the pace of the CEO search.

Adobe is too cheap to sell and too uncertain to buy. That is exactly what a Hold looks like.

Contact [email protected] for any questions or corrections.