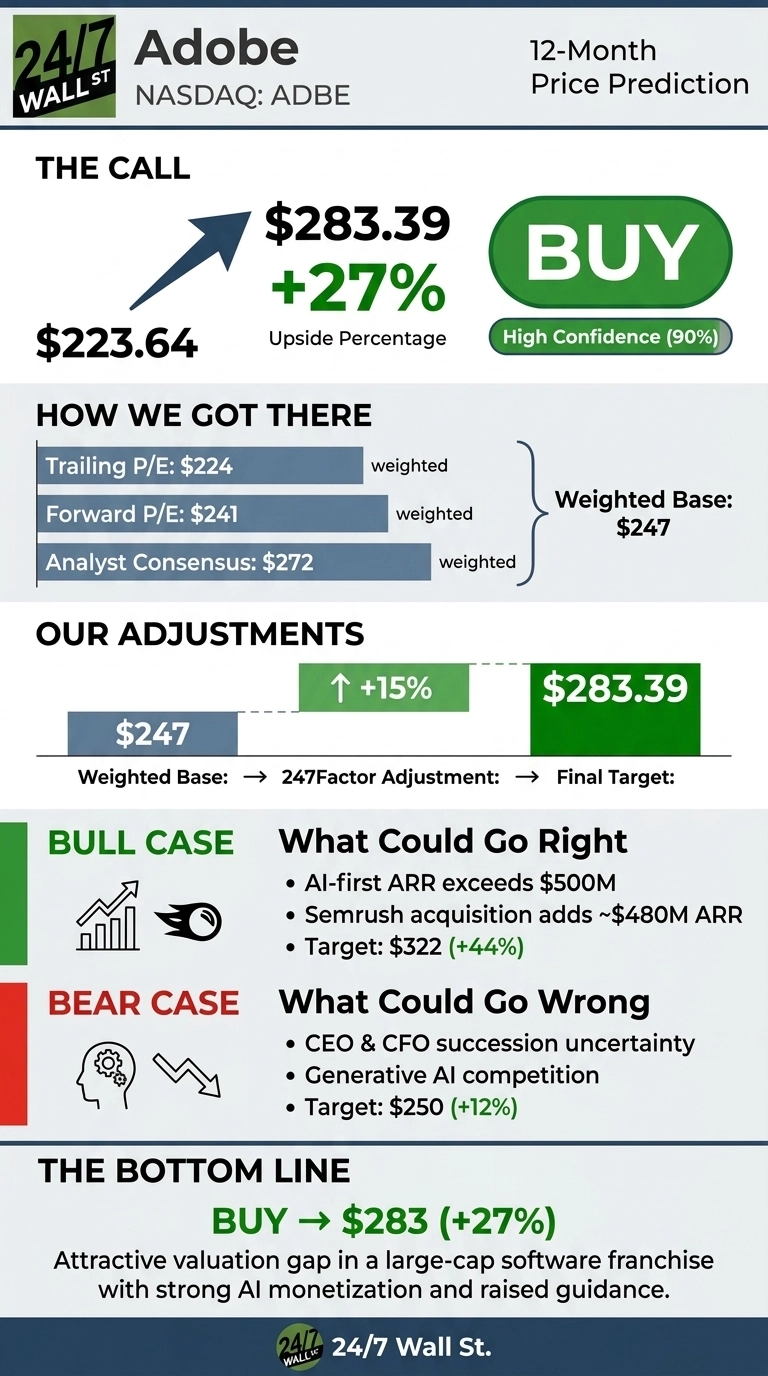

Adobe (NASDAQ: ADBE | ADBE Price Prediction) has been beaten down while fundamentals improved. Our 24/7 Wall St. price target is $283.39, roughly 26.72% above the current price of $223.64. We rate the stock a buy with 90% model confidence. An $88.9 billion software franchise with AI-first ARR north of $500 million, trading at a forward P/E near 9.

| Metric | Value |

|---|---|

| Current Price | $223.64 |

| 24/7 Wall St. Price Target | $283.39 |

| Upside | 26.72% |

| Recommendation | BUY |

| Confidence Level | 90% |

Adobe Was Cut Nearly in Half While Fundamentals Improved

ADBE is down 39.79% over the last year and 36.1% year to date, below the 52-week high of $376.16 and just above the $190.12 low.

Q2 FY26, reported June 11, 2026, was a record. Revenue hit $6.62 billion (up 13% YoY), non-GAAP EPS of $5.96 marked a fifth straight beat, and total ARR closed at $27.10 billion. Management raised FY26 non-GAAP EPS guidance to $24.35 to $24.45.

The Case for $322 and Higher

Our bull scenario takes ADBE to $322.51, a 44.21% return over 12 months. Firefly ARR is approaching $300 million and grew roughly 50% quarter over quarter, Firefly enterprise ARR is up 4x YoY, and Creative freemium MAU jumped from 50 million to 90 million.

Acrobat AI Assistant paid MAU grew 150%+ YoY. Options positioning skews bullish with a full-chain put/call ratio of 0.46. The Semrush deal adds roughly $480 million in ARR, and consensus of $272.48 implies meaningful upside.

What Could Go Wrong

Our bear scenario finishes at $249.71, still an 11.66% return. CEO Shantanu Narayen is transitioning to Board Chair, CFO Dan Durn departed June 15, 2026, and Q2 GAAP EPS of $4.25 was weighed by a $70 million goodwill impairment and a $30 million litigation accrual.

Competition from OpenAI, Canva, Figma, and Microsoft Copilot has crushed the multiple. Recent insider activity skewed to selling. The goodwill charge is a non-cash write-down on a legacy Publishing and Advertising unit. Non-GAAP EPS of $5.96 still grew 18% YoY. The operating engine remains intact.

How Adobe Compares to Salesforce and Autodesk

Adobe’s forward P/E near 9 looks cheap against two AI-forward software peers.

Salesforce (NYSE: CRM)

Salesforce (NYSE: CRM) is the cleanest AI-monetization comparison. Q1 FY27 revenue of $11.13 billion grew 13.3% YoY, with Agentforce plus Data 360 ARR near $3.4 billion, up over 200% YoY. Salesforce trades at a trailing P/E of 18 versus Adobe at 13. On a comparable AI-growth basis, Adobe screens materially cheaper.

Autodesk (NASDAQ: ADSK)

Autodesk (NASDAQ: ADSK) is the closest creative and design software analogue. Q1 FY27 revenue of $1.93 billion grew 18.4% YoY with non-GAAP EPS of $2.99. Management guides FY27 non-GAAP EPS of $12.40 to $12.65.

Adobe’s forward EPS of $26.26 and Q2 revenue growth of 13% suggest the market is pricing ADBE like a decelerating incumbent, while the numbers describe a raised-guidance AI beneficiary.

I Would Buy Here, With Eyes Open

The 24/7 Wall St. price target of $283.39 with 90% confidence and a buy rating reflects a rare valuation gap in mega-cap software. A forward P/E of 9 attached to a business that just raised guidance and tripled AI-first ARR to over $500 million makes this compelling.

The setup looks attractive for investors who can stomach CEO and CFO succession noise. The thesis weakens if AI-first ARR growth breaks or if the freemium payback (management expects it to play out over 2027) fails to materialize.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $251.16 |

| 2027 | $283.39 |

| 2028 | $335 |

| 2029 | $390 |

| 2030 | $446.28 |

These projections assume Adobe converts freemium traffic into paid seats and defends its creative moat. Meaningful upside or downside could come from the CEO succession outcome, the pace of AI monetization, or a broad re-rating of the software sector.

Contact [email protected] for any questions or corrections.