Shares of Adobe (NASDAQ:ADBE | ADBE Price Prediction) are down 5% in Thursday midday trading, slipping to roughly $222.60 and pressing against a 52-week low of $220.17. The latest leg lower extends a brutal stretch for the creative-software giant.

Year to date, Adobe stock is down 37%. The trailing-12-month P/E ratio sits near 13x, an unusually compressed multiple for a name that long commanded premium software valuations.

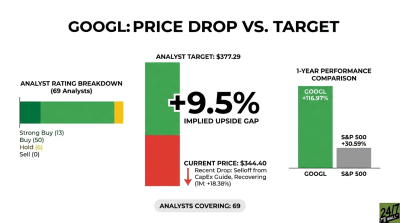

The contrast with Alphabet (NASDAQ:GOOGL) is stark. Alphabet stock is up 11% year to date, and that gap is fueling a debate among Adobe shareholders: should they hold on for a rebound, or rotate into one of the AI players pressuring Adobe?

Value Bargain or Value Trap?

The bull case for Adobe stock rests on heavy free cash flow, a deep enterprise moat across Creative Cloud, Acrobat, and Experience Cloud, aggressive buybacks, and a low valuation that could spring-load a rebound. Adobe’s Q1 FY2026 results backed parts of that thesis, with non-GAAP EPS of $6.06 beating estimates and revenue of $6.40 billion growing 12% year over year.

CEO Shantanu Narayen asserted that “Adobe delivered record Q1 results with AI-first ARR more than tripling year over year and subscription revenue growing 13 percent.” Adobe’s total ARR exited the quarter at $26.06 billion.

The bear case is the value-trap warning. Generative-AI rivals including OpenAI’s DALL-E and Sora, Midjourney, Canva, Figma (NYSE:FIG), and Alphabet’s own Imagen, Veo, and Gemini are encroaching on Adobe’s core creative turf. A cheap P/E ratio means little if AI permanently impairs growth, and Adobe sits inside the broader “SaaSpocalypse” selloff in subscription software.

Moreover, insider activity adds caution. Narayen disposed of roughly 75,000 shares on April 28 at prices between $243.19 and $244.78, with Adobe’s CFO and other executives selling alongside him during the decline.

Alphabet: Results and Risks

The irony is that “switching to Alphabet” means moving capital into one of the companies putting pressure on Adobe. Alphabet’s Q1 FY2026 print was impressive, with EPS of $5.11 versus a $2.63 consensus, and revenue of $109.90 billion, up 22% year over year.

Furthermore, Alphabet’s Google Cloud surged 63% to $20.03 billion, with backlog ballooning to roughly $460 billion. Google CEO Sundar Pichai declared that Gemini models are now processing “more than 16 billion tokens per minute via direct API use by customers, up 60% from last quarter.”

However, Alphabet isn’t risk-free. Antitrust scrutiny, AI competition in search, and a 2026 CapEx guide of $175 billion to $185 billion have compressed free cash flow. The prediction market on Polymarket pegs only a 4% probability that GOOGL stock closes higher today.

What to Watch Now

Adobe reports Q2 FY2026 results after the close Thursday, with guidance for revenue of $6.43 billion to $6.48 billion and non-GAAP EPS of $5.80 to $5.85. Polymarket assigns a 98% probability that Adobe beats EPS again.

The catch is that Adobe has beaten earnings five quarters in a row, yet the average day-of reaction has been -5%. Investors weighing a rotation into Alphabet should size their positions to account for the possibility that AI-driven disruption is rerating Adobe lower, even as the fundamentals hold up.

Tonight’s call from Adobe CFO Daniel Durn and the leadership team could shape the next share-price move. The setup is binary: a beat-and-raise may finally reward the discount, while another sell-the-news reaction would deepen the value-trap case and keep the “switch to Alphabet” debate alive into the back half of the year.

Contact [email protected] for any questions or corrections.