Micron Technology (NASDAQ:MU | MU Price Prediction) just delivered one of the most remarkable nine-month runs in mega-cap history, and the memory cycle bulls are convinced this is only the second inning. Our model takes a more cautious view.

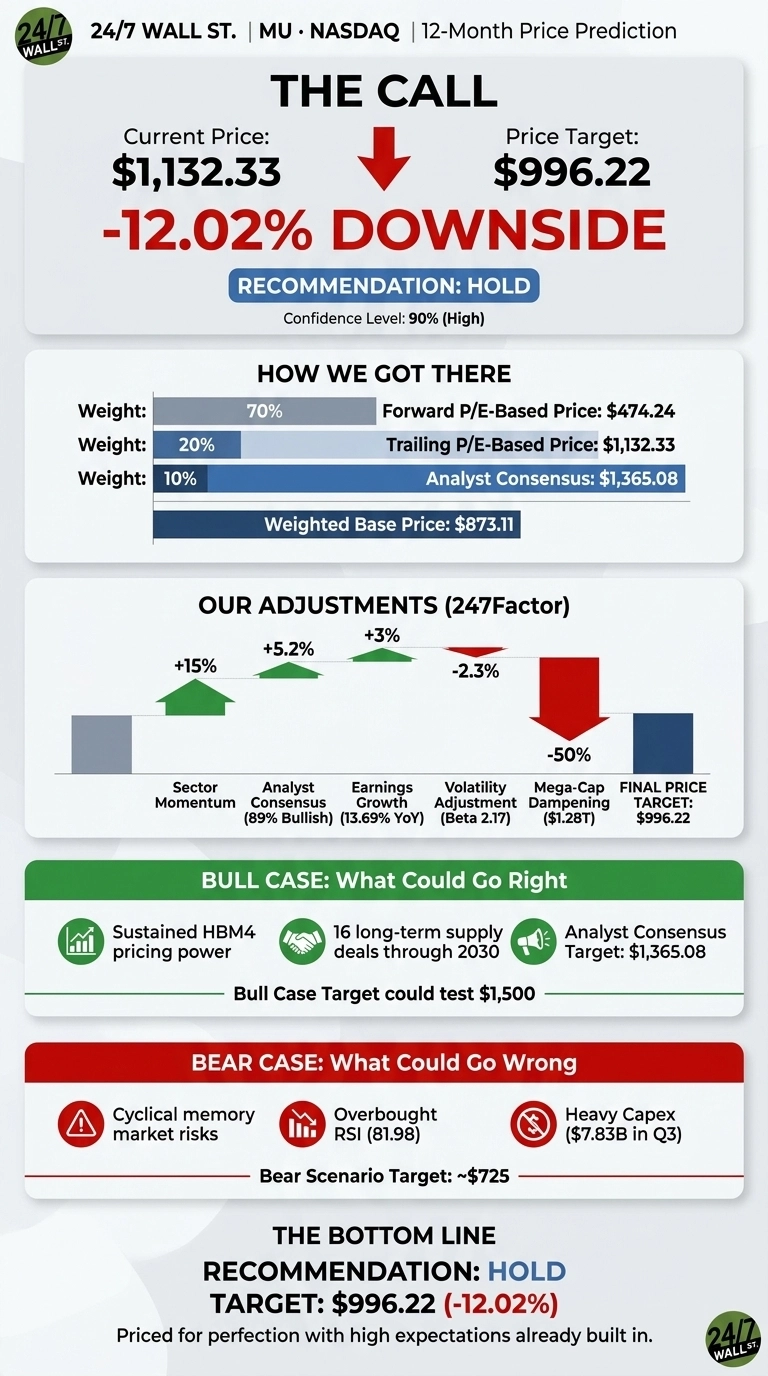

After running the numbers through our proprietary framework, the 24/7 Wall St. price target for Micron is $996.22, which implies a 12.02% downside from the current price.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $1,132.33 |

| 24/7 Wall St. Price Target | $996.22 |

| Upside/Downside | -12.02% |

| Recommendation | HOLD |

| Confidence Level | 90% |

Why We Could Be Wrong

Before going deeper, I want to be fair to the bulls. Micron is one of the most divisive stocks in the market right now, and real upside could come from sustained HBM4 pricing power into calendar 2027 or the activation of the 16 long-term supply deals secured through 2030.

Our 24/7 Wall St. price target is one datapoint among many. A detailed bull case appears below outlining why Micron could outrun our model.

An 11x Run Meets a Blowout Quarter

The setup here is extreme. Micron is up 296.92% year to date and 800.86% over the past year, trading 9% off the $1,255 52-week high.

Q3 FY2026, filed June 24, 2026, was a blowout: revenue of $41.46B beat by 17.6%, non-GAAP EPS of $25.11 beat by 23.79%, and GAAP gross margin reached 84.6%. Management guided Q4 to $50B in revenue with non-GAAP EPS of $31. Yet shares fell 6.69% the day after the report, hinting that expectations had run ahead of the fundamentals.

The Bull Case Above the Target

The bull case rests on AI memory becoming a structurally scarce asset. CEO Sanjay Mehrotra called out “multi-year Strategic Customer Agreements” enhancing predictability, and HBM4 is ramping in high volume with HBM4E targeted for calendar 2027.

Sell-side analysts are loudly bullish: Deutsche Bank lifted its target to $1,550, Morgan Stanley moved to $1,200, and DA Davidson went to $2,000 arguing the memory cycle is “not yet over.” The consensus target is $1,365.08. If HBM4 pricing holds and Q4 guidance proves conservative, shares could realistically test $1,500.

What Could Go Wrong

The risks are mostly cyclical. Weekly RSI sits at 81.98, deeply overbought for the eighth straight week. Historically, Micron has pulled back after earnings beats: the average one-week change post-earnings across eight quarters is -1.13%. Capex of $7.83B in a single quarter plus a $325M loss on debt prepayments show the cost of staying ahead.

Morningstar flagged “yellow flags for memory stocks”, and insider activity skews toward selling. Bulls would counter that the heavy capex funds HBM4E capacity that pays off through 2030. A bear scenario lands near $725.

Hold for Now

My verdict is hold with 90% confidence. The 24/7 Wall St. price target of $996.22 reflects a stock that has priced in a perfect cycle. A more constructive setup would require Q4 revenue above $51B with margins above 86%.

The picture weakens if RSI stays above 80 and hyperscaler capex commentary softens. The factor that tips the scale: the model values forward EPS at a sober multiple, and current pricing demands the cycle keeps accelerating.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $996 |

| 2030 | $972 |

These projections assume Micron continues executing on HBM4 and HBM4E with disciplined capex. A sharper memory downcycle in 2029 or 2030 could pull shares toward the bear path near $624.

Contact [email protected] for any questions or corrections.