Micron Technology (NASDAQ:MU | MU Price Prediction) has become the memory story of the AI cycle. Cloud Memory revenue hit $13.769 billion in fiscal Q3 2026 alone, and non-GAAP gross margin ballooned to 84.9%. CEO Sanjay Mehrotra called it plainly: “Micron’s record fiscal Q3 financial results and even stronger outlook for Q4 reflect the strategic value of memory in the AI era.”

Shares are up 241.97% year to date, yet the stock just pulled back sharply. So can MU push through to $1,500 in 2027? Let’s do the math.

Why Micron Shares Just Got Hit Despite Blowout Numbers

The pullback is real. MU fell 19.61% in the past week and 8.32% over the past month, even as YTD gains sit near 242%.

Two headlines drove the reversal. Michael Burry disclosed a short at $1,051.87, arguing the rally reflects “AI hype and FOMO rather than fundamentals”. Wall Street veteran Jordi Visser flagged the sell-off as a warning of a “mid-cycle slowdown” in the AI trade.

Add a beta of 2.142 and an ongoing class-action lawsuit alleging price fixing, and volatility becomes the price of admission. This is a stock that moves twice as hard as the tape in both directions.

Wall Street Sees Big Upside. Our Model Sees Fair Value.

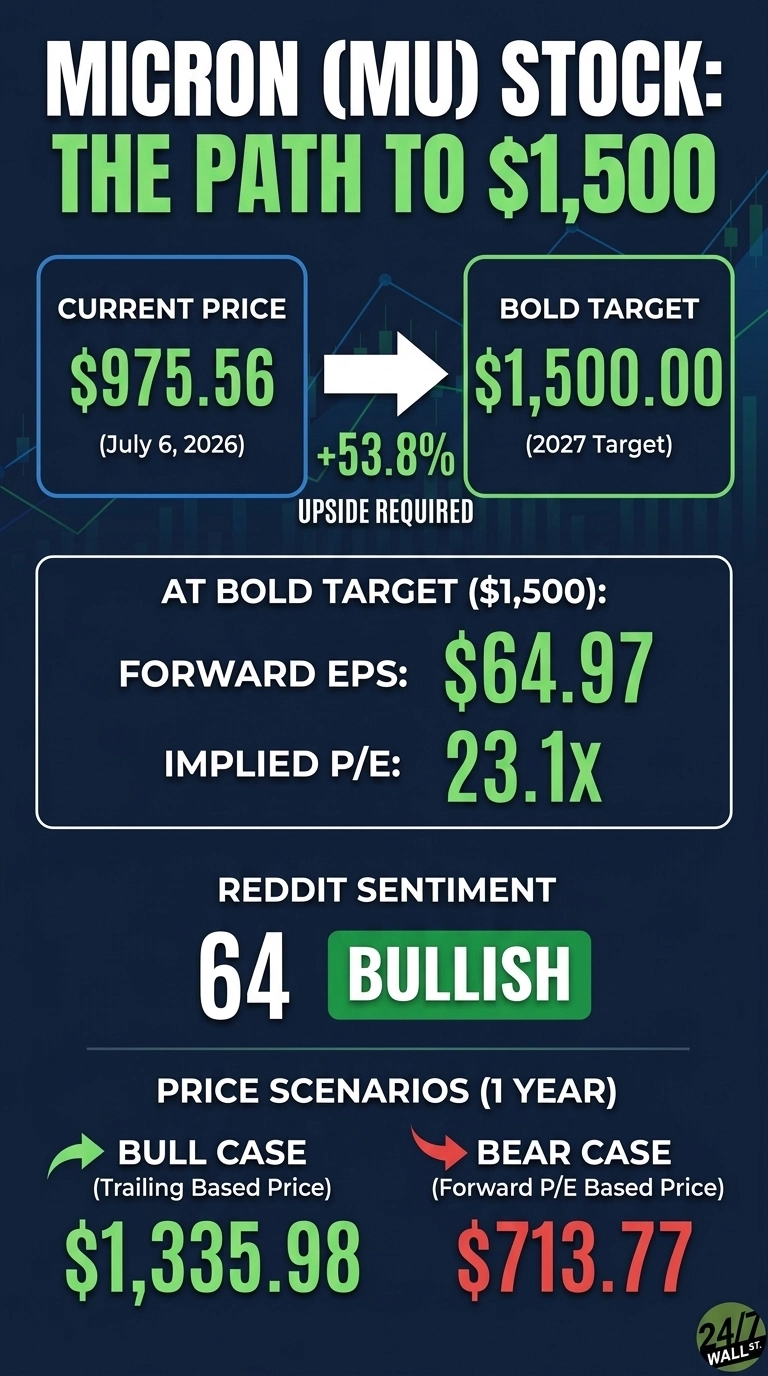

Analysts are unusually aligned. The consensus target is $1,486, with 9 Strong Buys, 31 Buys, 4 Holds, and just 1 Strong Sell. Bullish sentiment sits at 89%. Our own base case lands at $979.86, essentially flat, with a bull case of $1,335.98 and bear case of $713.77. Confidence is 90%.

My take: analysts are closer to right than our conservative base. When earnings acceleration is this violent (345.72% revenue growth), a P/E model built on trailing numbers understates the earnings trajectory.

The Path to $1,500 Per Share

Reaching $1,500 from today’s price of $975.56 would require a gain of 53.8%. With forward EPS of $64.97, a price of $1,500 implies a forward P/E of 23x. Our base case of $979.86 already implies 22x, meaning the bold target requires roughly 1.5x of additional multiple expansion.

That target is achievable if the AI capex build holds. Q4 26 guidance already calls for $50 billion in revenue and non-GAAP EPS of $31. Cloud Memory quadrupled from $5.284 billion in Q1 to $13.769 billion in Q3. Mehrotra says “multi-year Strategic Customer Agreements will significantly enhance the durability and predictability” of results.

HBM4 is in high-volume shipments, HBM4E is targeting calendar 2027 volume, and a $9 billion Japan expansion adds supply. Cramer captured the shift: “Micron’s Become a Secular Growth Story, Not a Cyclical Story.” The risk: memory has always been cyclical, and Burry is betting that history rhymes.

Where Micron Trades Today vs Its Earnings Power

At $975.56, MU trades at roughly 15x forward EPS of $64.97. Alpha Vantage pegs the forward P/E even lower at 7x on updated estimates. Either way, that is cheap relative to peers in the AI supply chain.

Shares sit between a 52-week high of $1,255 and a low of $103.23. The 10-year return of 7,903.59% shows the payoff when memory cycles turn. This is a compounding story if pricing power holds.

Is $1,500 Realistic? My Verdict

$1,500 by 2027 means a 53.8% gain and a 23.1x forward multiple. That is a stretch, but a reasonable one.

Three things need to go right: HBM4 pricing must hold through the ramp, Strategic Customer Agreements need to convert into visible FY27 revenue, and the AI capex cycle cannot roll over. A demand air pocket from hyperscalers would derail it fast. Returns at this level shouldn’t be expected every year, but we’ve outlined the blueprint for how Micron could reach $1,500 in 2027.

Contact [email protected] for any questions or corrections.