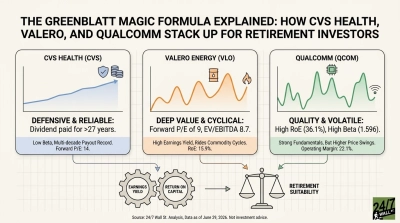

John Rogers Jr., founder of Ariel Investments, has built a four-decade track record buying quality but unloved mid- and small-cap consumer names, then holding them through years of doubt. His playbook prizes recognizable brands, durable cash flow, and disciplined capital return, purchased when Wall Street has given up. Ariel’s logo is a tortoise for a reason: slow and steady wins.

For retirement-focused investors, the Rogers philosophy is appealing, but the wrapper matters more than the sticker. Three current Rogers-style candidates are all out of favor for very different reasons. The real question is which kind of out-of-favor a retiree can actually live with. We rank them from least to most appropriate for a long-horizon income portfolio.

3. Mohawk Industries

Mohawk Industries (NYSE:MHK | MHK Price Prediction) is the world’s largest flooring company, home to Daltile, Karastan, Pergo, and Quick-Step. It is also the textbook Rogers pick: shares trade near $120, down almost 39% over five years, on a trailing P/E of 18x and a price-to-book ratio of 0.88.

Q1 FY26 revenue rose to $2.73 billion with adjusted EPS of $1.90, beating the $1.81 estimate. CEO Jeff Lorberbaum flagged that “the global flooring industry has been in a recession for almost four years, and historically we have multiple years of higher growth as markets recover.” Housing starts in May 2026 came in at 1,177 thousand units, still in the healthy range but well off the March 2026 peak of 1,522 thousand.

The problem for retirees: Mohawk pays no dividend, has a beta of 1.21, and the thesis rests entirely on a housing cycle turn that could take years. Big upside if it works, but no income while you wait.

2. Mattel

Mattel (NASDAQ:MAT) owns Barbie, Hot Wheels, Fisher-Price, and UNO. The stock has been punished, trading near $13.50, down about 32% year to date and over 57% over the past decade, near the 52-week low of $13.37.

Q1 FY26 revenue of $862.2 million topped estimates by 6.58%, with Hot Wheels billings up 17%. Management repurchased $200 million of stock in Q1 and is targeting $400 million in buybacks for 2026 under a new $1.5 billion authorization through 2028. Full-year adjusted EPS guidance is $1.27 to $1.39, and the shares trade at a forward P/E near 10x. Analysts have an $18.50 consensus target.

CEO Ynon Kreiz had a Masters of the Universe film hit theaters on June 5, 2026, plus a gaming push. For a retiree, though, Mattel pays no dividend, and toys are discretionary. It ranks ahead of Mohawk because iconic IP and heavy buybacks provide harder downside support than a housing cycle bet.

1. General Mills

General Mills (NYSE:GIS) owns Cheerios, Blue Buffalo, Häagen-Dazs, and Pillsbury. The stock is itself unloved, trading near $37.50, about 31% lower over the past year, on a trailing P/E of 9x with a beta of negative 0.04.

The Q4 FY26 report on July 1, 2026, delivered adjusted EPS of $0.95, crushing the $0.80 estimate, on revenue of $4.61 billion. Management reaffirmed a $3 billion cumulative cost-savings target by FY2030 and guided free cash flow conversion near 85%.

The dividend is the anchor. General Mills declared a $0.61 quarterly payout on July 1, 2026, payable August 3, 2026, with an uninterrupted history stretching back through the 2008 crisis and a current yield of 6.5%. Food spending hit $1,566.8 billion in May 2026, up from $1,518.3 billion a year earlier, even as consumer sentiment slid to 44.8, near recessionary levels. Risks include a $1.8 billion goodwill impairment on the North America Pet segment and a softer FY27 profit outlook.

The Rogers Verdict for Retirees

Rogers’s philosophy is about buying quality brands during maximum pessimism and waiting. All three names qualify. But retirement portfolios weigh income reliability and volatility more heavily than upside optionality. Mohawk offers the biggest recovery torque and no cash return. Mattel adds iconic IP and aggressive buybacks, still without a dividend. General Mills pairs a beaten-down valuation with a 27-year dividend record, a defensive beta near zero, and cash flows tied to grocery aisles that shoppers fill regardless of the sentiment index. For a long-horizon retiree looking for the Rogers tortoise pace with a paycheck attached, General Mills is the fit.

Contact [email protected] for any questions or corrections.