SoFi Technologies (NASDAQ: SOFI | SOFI Price Prediction) has dominated retail trading feeds all year on the strength of a 30% revenue growth guide, a stablecoin launch, and a CEO who keeps buying his own stock. But here’s what you should actually be watching.

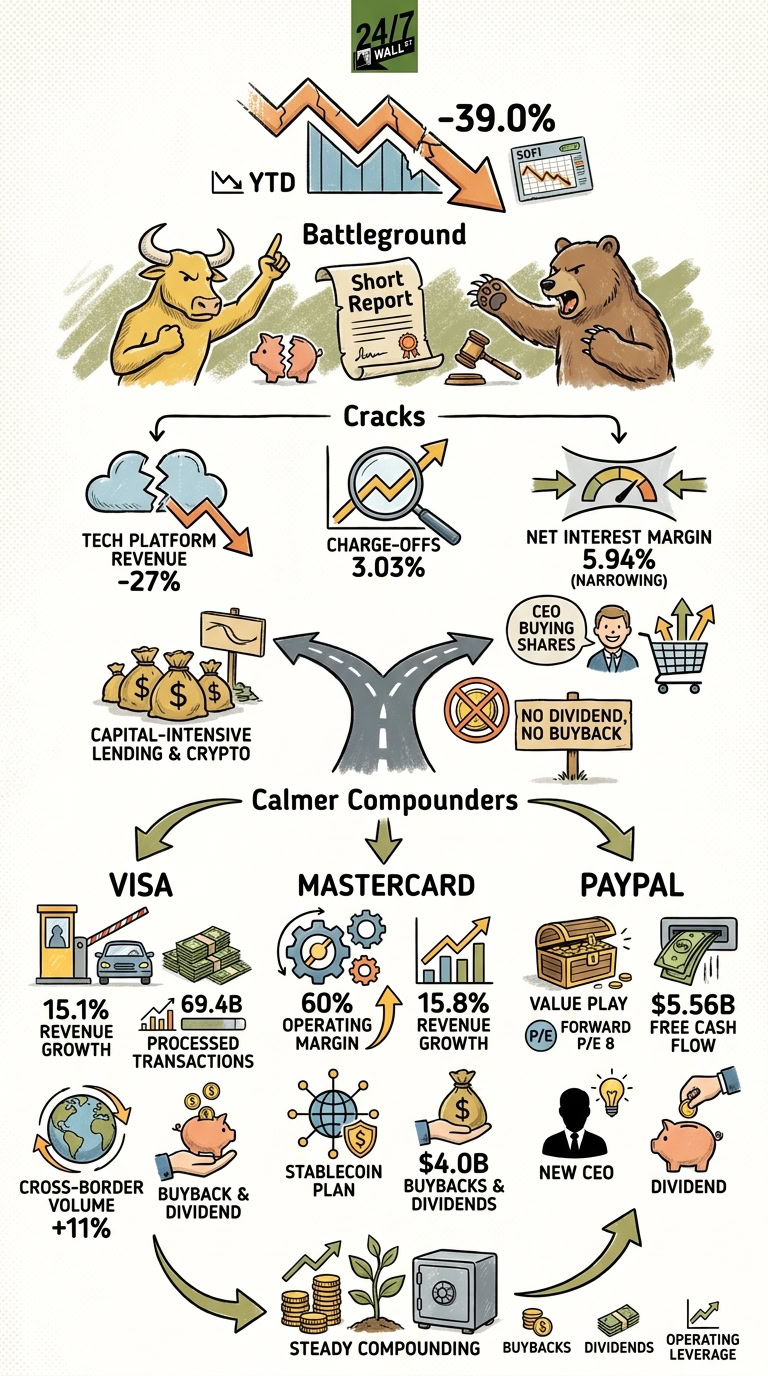

SoFi trades as a battleground ticker right now. The stock is down 39.0% year to date through May 26, trading at $15.98 against an analyst mean target of $21.00 that has been steadily cut. Goldman Sachs, Morgan Stanley, Bank of America, and Keefe Bruyette & Woods all trimmed targets, while Muddy Waters issued a short report alleging improper financial reporting and Block & Leviton opened a securities fraud investigation.

The Q1 headline numbers were fine, but the cracks are real: Technology Platform revenue fell 27% year over year on a large client departure, personal loan charge-offs rose to 3.03% from 2.80% sequentially, and net interest margin narrowed year over year to 5.94% compared to the prior-year period. CEO Anthony Noto bought 116,323 shares since March, which is admirable conviction. SoFi also pays no dividend, runs no buyback, and is pivoting deeper into capital-intensive lending and crypto. Retirement investors deserve calmer compounders. Here are three.

1. Visa: The Toll Booth Still Works

Visa (NYSE: V) is the boring duopoly half of global payments and that is the entire point. Q1 FY26 revenue rose 15.1% year over year, with processed transactions of 69.4 billion (+9%) and cross-border volume ex-intra-Europe up 11%. Operating margin sits at 67.3%, the company carries a 0.784 beta, and management is returning capital aggressively: $21.1 billion remaining buyback authorization and a $2.68 annual dividend. Analysts are nearly unanimous in recommending buying shares. The stock is down 6.9% year to date, providing a relative entry discount versus the five-year average multiple.

2. Mastercard: 60% Operating Margins and a Stablecoin Plan

Mastercard (NYSE: MA) is the answer to the “but what about crypto disruption?” question SoFi bulls keep raising. Q1 FY26 revenue grew 15.8% year over year to $8.40 billion, adjusted operating margin expanded to 60.8%, and cross-border volume was up 13%. The company returned $4.0 billion via buybacks and $777 million in dividends in a single quarter, with $11.7 billion left on the authorization. Mastercard Agent Pay and the planned BVNK acquisition put the network at the center of stablecoin settlement, which is the same trend SoFi is chasing from a far weaker competitive position. Shares are down 13.6% year to date to $493.01.

3. PayPal: The Unloved Cash Machine

PayPal (NASDAQ: PYPL) is the value play hiding in plain sight. The stock trades at a forward P/E of 8, and it generated $5.56 billion in free cash flow in FY25. Management retired $6.0 billion in stock over the trailing 12 months and just initiated the company’s first dividend at $0.14 per quarter. A new CEO, Enrique Lores, is the catalyst, and Michael Burry recently increased his stake. On a $39 billion market cap returning roughly $6 billion annually to shareholders, the math takes care of itself.

The Takeaway

For investors weighing the headline drama, the three names above offer steadier compounding profiles backed by buybacks, dividends, and operating leverage.

Contact [email protected] for any questions or corrections.