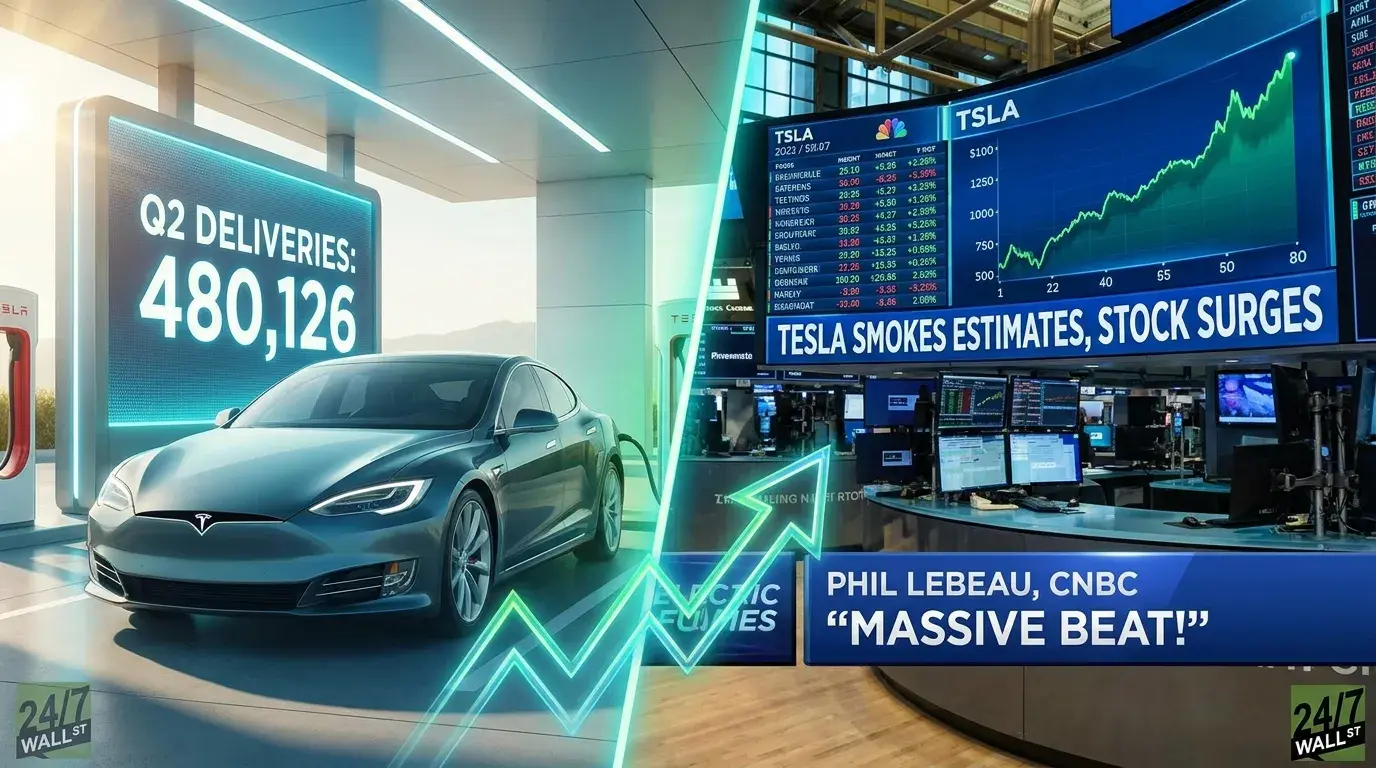

Phil LeBeau went on CNBC Thursday morning and delivered the kind of number that reorders a Tesla (NASDAQ:TSLA | TSLA Price Prediction) week. “These are far better than the street was expecting for the second quarter. Tesla delivering almost 481,000 vehicles,” he said. For a company that spent the first half of 2026 fighting a narrative about EV demand cratering, this was the reversal.

Tesla reported Q2 deliveries of 480,126 vehicles against a consensus estimate of 406,600. That is the beat everyone is talking about, and it is a big one. The stock, worth about $1.6 trillion going into the release, had been coasting on a 13.25% one-week run before today’s release landed.

The number that shocked wall street

LeBeau summed the math up bluntly. “The consensus estimate going into today was 406.6 thousand vehicles. They beat it by 74,000 vehicles. So just a massive beat from Tesla for the second quarter.”

Context matters here. Q1 2026 deliveries came in at 358,023 units, which Jim Cramer had characterized as up about 6% year over year but well below expectations. Then Goldman Sachs walked its Q2 forecast up to 420,000 vehicles from 405,000, and Polymarket traders sniffed something bigger, pricing the 475,000-plus bracket at 0.993 probability heading into today. The prediction market called it. Sell-side analysts stayed lower.

Q2 production was 451,758 vehicles, meaning Tesla shipped more cars than it built. That drew down the inventory that had ballooned to 27 days of supply at the end of Q1. That is the inverse of the problem Cramer flagged in April, when production was rising almost 13% year over year while deliveries lagged. Demand showed up.

It wasn’t just cars

The other line in LeBeau’s report that deserves attention concerns the energy business. “They also deployed 13.5 GWh of energy storage. That business continues to accelerate,” he said. That figure sits comfortably above the 12.5 GWh record set in Q3 2025 and near the 14.2 GWh Q4 2025 record. Megapack is quietly becoming the part of Tesla that behaves most like a real growth business, with Services and Other already growing 42% year over year in Q1.

The regional picture underneath the top-line number is uneven. China-made EV sales rose 24.4% year over year in June, the eighth straight month of growth. Spain sales climbed 5.6% in June and 29.8% for the first half. Norway registrations fell 43% year over year. Tesla can absorb Norway. It cannot absorb losing China, which is why the 24.4% number probably matters most inside Palo Alto.

Meanwhile, BYD reported Q2 2026 battery-electric deliveries of 557,090 units and is on track to reclaim the global EV crown.

Tesla winning the estimate game while still trailing BYD in absolute volume is the shape of this market now.

What to watch next

Deliveries are a volume metric. Margins are a profit metric. Those are different things, and the second one gets answered on July 22, after the close, when Tesla reports full Q2 financial results. That is when the market finds out whether the extra 74,000 cars came with pricing discipline or with incentives that compress automotive gross margin. See Tesla’s prior Q1 2026 exhibit on SEC.gov for the baseline.

Q1 was encouraging on that front. Automotive gross margin expanded to 21.1% from 16.2% year over year, and free cash flow ran $1.44 billion. If Tesla held that line while delivering 480,000 cars, the story writes itself. If margins slipped to move the metal, the beat gets recharacterized quickly.

One more thing to keep an eye on. Michael Burry disclosed a fresh short against Tesla at $416.22. The stock opened this morning down 2.89% despite the beat, which tells you the tape was already pricing in something close to this outcome. The analyst consensus target of $421.16 now looks stale. Watch the revisions. That is where the real repricing happens over the next two weeks.

For a regular investor, the takeaway is simple. Tesla just proved the demand skeptics wrong on volume. Whether it proved them wrong on profitability shows up July 22. Both answers are worth waiting for before writing the epitaph on either side of the trade.

Contact [email protected] for any questions or corrections.