One line from Microsoft (NASDAQ:MSFT | MSFT Price Prediction) CEO Satya Nadella on the April earnings call reframed the entire debate over how quickly generative AI can turn into a real profit-and-loss line. The company’s AI business now operates at scale, and the growth rate suggests the ramp is still in its early innings.

The Number

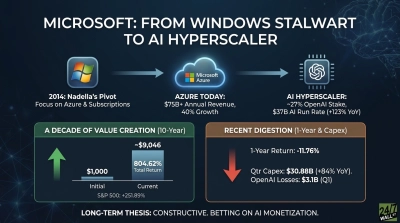

$37 billion. That is Microsoft’s AI annual revenue run rate as of the fiscal third quarter of 2026, reported in the company’s 8-K filed April 29, 2026. On Microsoft’s recent earnings call, Nadella stated it plainly: “Our AI business surpassed an annual revenue run rate of $37 billion, up 123% year over year.”

This is a company disclosure of a run-rate metric, distinct from reported GAAP revenue and from forward guidance. It also reflects annualized current-quarter run rate as defined by management.

What It Means

A 123% year-over-year jump on a base this large is the operational headline. It sits inside a broader cloud engine that is accelerating with it. Intelligent Cloud revenue reached $34.681 billion, up 30%, and Azure grew 40% in constant currency. Microsoft Cloud clocked $54.5 billion in the quarter, up 29%.

The demand behind the run rate is visible in Microsoft’s reported backlog. Commercial remaining performance obligations hit $627 billion, nearly doubling year over year at 99% growth. That is contracted revenue queued up for future delivery. On top of this key figure, capital expenditures came in at $30.876 billion, up 84.39% year over year. That’s the amount Microsoft has set aside to fund its AI data centers which support that backlog. Copilot adoption is the other tell. Paid seats crossed 20 million, up 250% year over year, with Accenture alone taking 740,000 seats.

Market Reaction

Shares of Microsoft traded at $428.00 at the April 29 filing, closed at $414.44 one day later, and reached $450.24 thirty days after the report. As of July 2, 2026, the stock closed at $390.49, with a one-week gain of 10.67% off a lower base and a one-year decline of 19.85%. The stock’s 10-year return of 763.3% puts the recent pullback in context for long-term holders.

Bull Case

Microsoft’s bull case rests on scale, mix, and durability.

In terms of scale, a $37 billion AI run rate compounding at triple digits is generating cash flow now, with operating cash flow of $46.679 billion in the quarter, up 26.01%. The company’s mix has also improved, with consolidated operating margin sits at 46%, and CFO Amy Hood told investors AI margins are “better and have remained better in our AI business versus where we saw them in the cloud transition looking back.” And on durability, there’s plenty for Microsoft investors to like. Capacity is sold out, with management saying it expects to remain capacity-constrained “at least through 2026.”

The ROI question that hangs over hyperscaler capex was answered directly. Nadella responded recently that, “When the TAM is so expansive and when shortages are generally growing between supply and demand, it gives you a lot of confidence in the ROI.” The chip supplier picture reinforces the demand signal. NVIDIA (NASDAQ:NVDA) is up 24.06% over the past year, closing at $194.83 on July 2, 2026, on continued AI infrastructure orders.

Analyst View

Analyst sentiment aligns with the operational picture. Microsoft carries 12 strong buys, 40 buys, 3 holds, and zero sell ratings, with an analyst target price of $561.11 against a share price near $390. Forward P/E stands at 20.

Bottom Line

For long-term holders, the $37 billion AI run rate is the pivot point in the Microsoft story. It converts the capex debate from theoretical to arithmetic. The $627 billion commercial backlog and 20 million paid Copilot seats provide the revenue lines that the roughly $190 billion in calendar 2026 planned capex is meant to serve.

Microsoft’s 12-month drawdown coexists with an AI franchise scaling at a rate few software businesses ever have. That gap between price action and operating trajectory is where patient investors tend to find their edge.

Contact [email protected] for any questions or corrections.